Nadia Gharbi, Senior Economist Pictet Wealth Management.

We expect that the ECB’s Governing Council (GC) to maintain the current policy rates at this week’s monetary policy meeting (on 26 October). We also foresee the GC remaining open to further hikes if the inflation outlook worsens while stressing that it sees the present level of rates to be appropriate.

The press conference will likely centre on three primary topics:

- Risks associated with the economic outlook.

- The efficiency of monetary policy transmission.

- Normalisation of the ECB’s balance sheet.

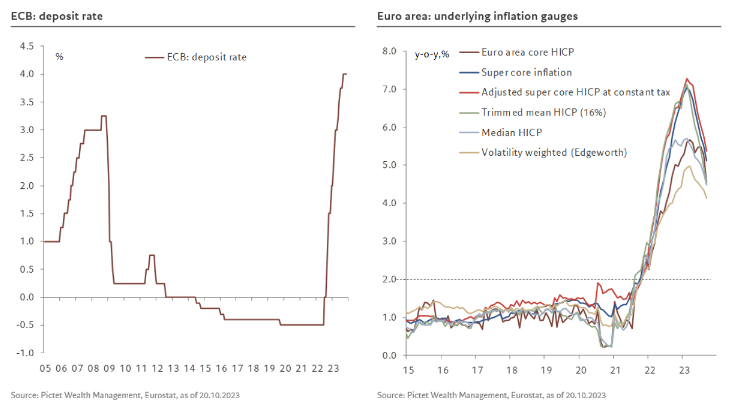

Economic Outlook: Recent data on economic activity have been muted, consistent with the September staff projections. While inflation data have displayed clear disinflationary trends, fluctuations in energy prices have raised concerns about potential ‘second-round’ effects on headline inflation. ECB president Christine Lagarde will probably underscore the heightened uncertainty surrounding the economic outlook due to the conflict in the Middle Eastern, hinting both at a potential downturn in growth and inflationary pressures from rising energy prices.

Monetary Policy Transmission: The GC has substantially upgraded its evaluation of the robustness of monetary policy transmission. From our perspective, recent developments should solidify the view that policy transmission is indeed progressively influencing broader financial conditions and the actual economy. Notably, long-term (real) sovereign bond yields have surged in parallel with developments in the US bond market, while monetary and credit statistics suggest credit is contracting.

Balance Sheet: Given recent market fluctuations, especially increased yields and spreads, we don't anticipate any news regarding reinvestments of the ECB’s Pandemic Emergency Purchase Programme (PEPP). If questioned, Lagarde might hint at ongoing discussions but emphasise the GC's reluctance to hasten balance sheet normalisation given current market developments. Considering the recent widening of spreads on Italian government bonds, Lagarde may face questions about the ECB’s Transmission Protection Instrument (TPI). She is likely to say that PEPP reinvestments remain the primary strategy, while the TPI remains a further viable option to deploy if necessary. Before the Thursday meeting, it is worth mentioning that some important data will be published. In particular, flash purchasing manager index (PMIs) figures for October (on 24 October) will likely provide more clarity on the pace of Europe’s growth in Q4, while the publication of the Bank Lending Survey on the same day will give more insight into the impact of monetary tightening.

Overall, we expect no policy changes this week and no new announcement about quantitative tightening. Nor do we expect the ECB to review the remuneration of banks’ required reserves before the conclusion of its review of its operational framework in spring 2024. We continue to believe that the ECB has concluded its cycle of rate hikes and that it will hold rates at the current level for the foreseeable future.