FOMC preview (November 1) – proceeding carefully with a tightening bias We expect the FOMC to keep rates unchanged at 5.25-5.50% at its meeting next week, as is widely priced by the markets. We don’t expect changes to QT or tweaks in other administered rates. There will be no new dot plot or economic projections.

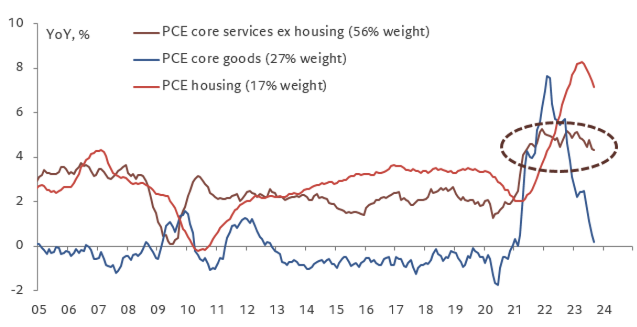

Economic data since the last FOMC meeting suggest growth strengthened further, the labor market remains tight, and trend inflation declined. Meanwhile, financial conditions have tightened meaningfully and the conflict in the Middle East introduced renewed uncertainty and upside risks to energy prices. Recent Fedspeak suggests the FOMC’s base case is likely that growth will slow in coming months. But officials remain concerned about a re-acceleration in inflation and deems it premature to conclude the hiking cycle. The latest PCE report shows supercore inflation, the Fed’s preferred gauge of underlying price pressures, remains elevated.

We expect the policy statement to acknowledge robust growth in the third quarter, but keep in place the forward guidance that “In determining the extent of additional policy firming that may be appropriate”. A dovish move would be to remove the word “additional”, suggesting more strongly that rates may already be at a sufficiently restrictive level.

Chair Powell is likely to repeat his stance from his October 19 speech, suggesting that the Fed is proceeding carefully. He noted that the rise in long-end rates had done some of the Fed's financial tightening work for it, and the increase did not reflect repricing of Fed expectations, so the tightening can be viewed as a substitute for additional rate hikes.

Officials are mindful of robust growth and a strong labor market, and is likely to repeat the reaction function that "additional evidence of persistently above-trend growth, or that tightness in the labor market is no longer easing, could put further progress on inflation at risk and could warrant further tightening of monetary policy".

Core PCE inflation breakdown - supercore inflation, the Fed’s preferred gauge of underlying price pressures, remains elevated.

US GDP: Consumers went nuts in Q3, but a hard act to follow

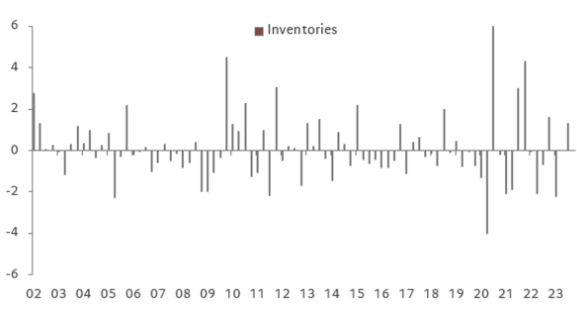

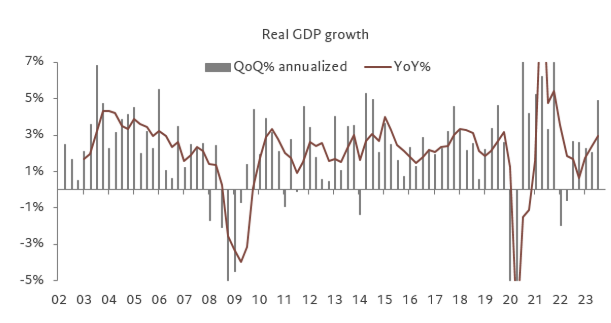

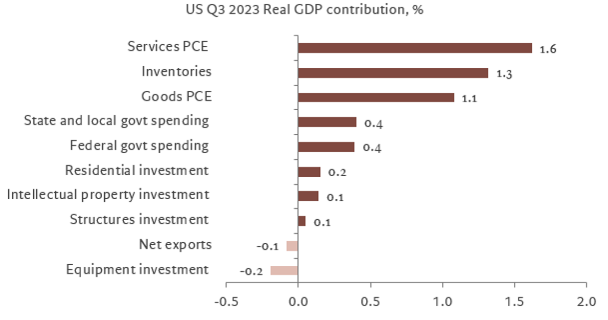

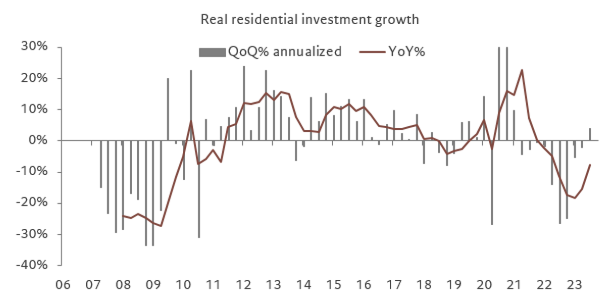

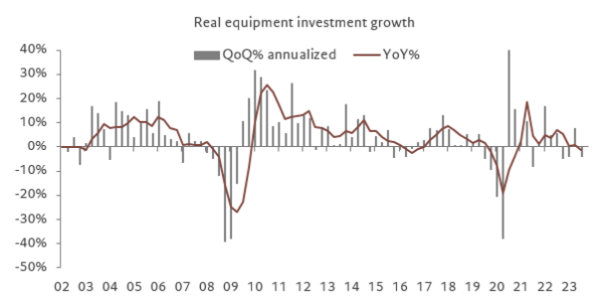

Real GDP accelerated sharply in Q3, rising 4.9% QoQ annualized, up from 2.1% in Q2 and better than consensus expectation of 4.5%. In fact, consensus expectation started the quarter at zero! (and shout out to the Atlanta Fed GDP Now). The acceleration was driven by strong consumption and government spending, and an outsized 1.3pp boost from inventories. Business investment contracted slightly as equipment investment fell after a sharp rise last quarter. Stripping out the volatile trade and inventories, domestic final sales, a better gauge of final demand, grew at a still impressive rate of 3.5%. The GDP deflator surprised on the upside, coming in at 3.5% QoQ annualized, up from 1.7% in Q2. However, importantly, quarterly core PCE inflation came slightly below expectations, raising downside risks to tomorrow’s monthly print, where consensus is looking for a print of 3.7% YoY. Looking into the details, there is no denial that the economy was on strong footing in Q3. But the factors that contributed to the strength are turning negative and we expect growth to slow below potential in Q4. Strength in consumer durable goods and discretionary services spending turbocharged the economy in Q3, but student debt payment, gas prices, tighter borrowing costs, and less pent up demand should lead to a slowdown. In fact, real disposable personal income was negative in Q3. Residential investment grew in Q3 after nine quarters of contraction, but the renewed rise in mortgage rates should dampen housing demand. Business investment lost momentum at the end of the quarter, and business surveys are consistent with anemic growth. Inventories contributed heavily to growth in Q3 after two quarters of destocking. This sector is volatile and tend to be mean revering, and such heavy inventory accumulation is unlikely to be repeated.

On the other hand, government spending, fueled by defense spending and infrastructure bills, is likely to continue adding to growth. Overall, the US economy has been outperforming expectations despite monetary constraint and credit tightening. But GDP is backward looking and do not change our expectation for the Fed to be on hold at the meeting next week. Financial conditions tightening and geopolitical uncertainty should make the Fed proceed carefully, while above-target inflation and red hot growth should keep the hawkish policy bias alive.

Chart 1. Real GDP growth contribution by spending categories

Chart 2. Q3 Real GDP growth contribution by detailed spending categories

Chart 3. Real residential investment – still negative but pace of decline slowed

Chart 4. Real equipment investment – strengthened due to transportation

Chart 5. Inventories contribution to real GDP