Enrique Díaz-Alvarez, Matthew Ryan, CFA, Roman Ziruk, Itsaso Apezteguia, Eduardo Moutinho & Michał Jóźwiak

We’ve witnessed a rather mixed performance from the currencies in Central and Eastern Europe since our last update.

All four of the currencies covered in this report have lost ground against the euro in the past four months, to varying extents. This can be partly attributed to the shift towards an easing bias among the central banks in the CEE, at a time when rates of inflation in the region continue to print well above target, and indeed above most other European countries. The broad ‘risk off’ mode prevalent in financial markets in recent months has also contributed to the move, as investors brace for a slowdown in growth globally, notably in the Euro Area, which appears on the brink of a technical recession.

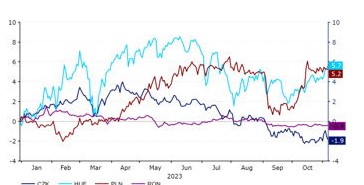

The recent mild underperformance in the CEE currencies ensures that the Czech koruna (-1.9% vs. EUR) and the Romania leu (-0.4%) are now trading lower for the year against the euro. We view the weakness in the former as partly an effect of high valuation and an underwhelming performance in the Czech economy, while the leu continues to be unfavoured due to the twin deficits in Romania’s current and fiscal accounts. The Hungarian forint (+5.7%) and the Polish zloty (+5.2%), however, remain two of the better performing emerging market currencies so far in 2023. In the case of HUF, we see this as partly due to valuation and an improvement in real rates, while sentiment towards PLN has also improved since the election victory for the opposition coalition in Poland in October.

CEE FX Performance [vs. EUR] [2023] Source: LSEG Datastream Date: 08/11/2023

Since our last update, rates of inflation in the CEE have begun to normalise, albeit from extraordinary high levels. Indeed, Citigroup ’s Inflation Surprise Index for the CEEMEA region is now roughly flat, indicating that inflation data is currently more-or-less matching economists’ estimates. In response to the easing in price pressures, most central banks in the CEE (with the exception of the National Bank of Romania) have either already begun their easing cycles, or appear to be on the brink of delivering their first cuts. The Hungarian National Bank was the first to begin easing policy in May, with the National Bank of Poland shocking investors with a massive 75 basis point rate cut in September. Meanwhile, the Czech National Bank unexpectedly held rates steady in early-November, although the first cut there doesn’t appear to be too far off.