By Ole Hansen, Head of Commodity Strategy at Saxo

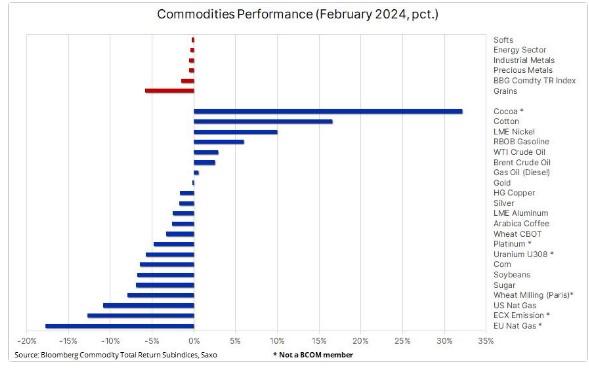

Commodities suffered a broad albeit moderate setback last month with all sectors trading lower, primarily led by a third monthly decline in grains after the sector hit a three-year low amid ample supply, in the process driving the speculative short position to a record high. Overall, the Bloomberg Commodity Total Return index (BCOM), which tracks a basket of 24 major commodity futures almost evenly split between energy, metals, and agriculture, traded 1.5% lower, a fourth monthly decline.

Ole Hansen |

The table below shows the performance across several commodity futures, some of which are not members of the BCOM index. Examples include cocoa which surged higher by one-third, recording its biggest monthly gain in 22 years, as the supply crisis in West Africa continued to cause havoc across the chocolate industry. At the bottom of the table, we find EU natural gas suffering further losses amid ample supply and mild end-of-winter weather, and partly linked to that, the ECX emission contract which slumped near to a three-year low – and more than halving from last year’s peak. Staying with the energy theme, it’s worth noting that without the notoriously volatile US natural gas contract, which slumped to a near four-year low, the BCOM index loss would have been less than one percent with crude oil and fuel products all trading higher amid emerging signs of underlying strength

Elsewhere, it was a relatively quiet month across the metals space with industrial and precious metals both suffering small declines, a relatively decent performance during a month where China economic data continued to disappoint while US Treasury yields shot higher after US data strength further delayed the expected timing of the first and depth of subsequent US rate cuts.

EU emissions and green transformation industry continue to suffer

Wall Street reached new record highs last month and, not surprisingly given the current AI hype and focus on defence, Saxo’s equity theme baskets show strong year-to-date gains for defence and semiconductors, followed by mega caps and cybersecurity. At the bottom of the table, we find four baskets that include companies involved with commodities and the green transformation.

During the past year, with surging funding costs and the recent prospect of rates not being reduced at the same pace as previously thought, the capital-intensive industries involved with developing solutions within the green transformation, renewable energy, and energy storage have all suffered steep declines. Besides high funding costs, these industries have also suffered from a steep decline in natural gas prices which have raised the relative cost of developing alternative solutions.

Related to this, another market that has suffered steep declines in recent months has been the cost of buying carbon offsets in Europe with the ECX emission contract at one point slumping to near EUR 50 per tons, down from EUR 105 this time last year. The collapse in the cost for paying to pollute has partly been driven by the fact that the European power network is cleaning up so fast it's destroying demand for carbon permits. The massive rollout of solar and wind farms across the EU during the past couple of years, and the recovery in nuclear power generation in France combined with lower industrial activity topped up with a mild winter all driving natural gas prices sharply lower have reduced demand for higher polluting coal.

The energy transformation and focus on combating harmful emissions had, up until last year, supported sharply higher emission prices and with that driven a speculative long bubble with traders/speculators believing it could only go up. Having almost halved in value during the past year, that speculative bubble has burst, thereby reducing the selling pressure. Overall, however, the prospect for a recovery depends on economic activity and whether we see a revival among the heavy energy-consuming industries that were hurt during last year’s gas price surge. With the market for emission allowances set to tighten significantly later this decade – as more industry groups will have to buy permissions – a floor will eventually be found, but whether that floor is above EUR 50 remains to be seen and will, among other factors, depend on whether Europe can avoid a prolonged economic slowdown.

Cocoa : speculators no longer to blame for ongoing surge

Cocoa futures extended their parabolic surge last month, rising more than one-third to record the biggest monthly jump in 22 years. The rally which gathered momentum late last year has seen the futures price in New York surge to a record high above USD 6000 per ton, around 2.5 times higher than the five-year average seen prior to 2023. This was driven by a worse-than-expected deficit in 2023-24 – the third in a row – due to adverse developments in West Africa, the world’s top producing region, accounting for around 75% of global production. Heavy rains earlier in the season hurt crops and spread disease before ageing trees had to contend with heat and dryness. All these developments contributed to lowering output and with small-lot farmers not reaping the economic award, they will continue to struggle affording much needed but expensive pesticides and fertilizers to combat diseases while maintaining production from ageing trees.

Arrivals of bags from cocoa farmers to ports in Ivory Coast, the number one shipper, are currently down around one-third on last year, and with the mid-season crop after March now also looking challenged, it has raised concerns about the availability of cocoa to meet already agreed sales obligations, potentially leaving some of the major chocolate producers short changed, forcing them to enter the futures market to secure supplies, inadvertently turning into buyers of futures instead of normal selling (hedging) activity. Looking at the weekly Commitment of Traders data, we find that producers are increasingly the main buyers as they cut short positions while hedge funds have been net sellers for several weeks, in the process cutting their net long to an 11-month low.

Gold’s coiled spring behaviour

We maintain a bullish outlook for gold and silver, but as we have highlighted on several occasions in recent months, both metals are likely to push significantly higher until we get a better understanding about the delivery of future US rate cuts. Until the first cut is delivered, the market may at times run ahead of itself, in the process building up rate cut expectations to levels that leave prices vulnerable to a correction. With that in mind, the short-term direction of gold and silver will continue to be dictated by incoming economic data and their impact on the dollar, yields and not least rate cut expectations.

One key focus remains the short-term rates market which has gone from pricing in more than six 25 basis points US rate cuts this year to less than four, while bets on the timing of the first cut have moved out to June, potentially leaving a very narrow window available for the remainder of these cuts. This assumes that the FOMC is unlikely to cut rates near the November US Presidential election in order to avoid being accused of showing favouritism towards the incumbent president.

That said, gold managed to put up a very strong defence last month against a stronger dollar and surging Treasury yields, especially the 2-year yield which surged higher by more than 40 basis points to 4.62%, thereby once again lifting the opportunity cost of holding a non-coupon paying position in gold. Overall, the metal ended the month with a small loss and ahead of Thursday’s long-awaited US PCE core deflator print, the Fed’s preferred inflation gauge, gold had behaved like a coiled spring, wanting to trade higher despite yield headwinds, but held back by worries about an inflation surprise. However, with the number in line with expectations, the yellow metal moved higher thereby moving closer to the February high at USD 2065 per ounce.

Crude oil stuck in neutral despite underlying strength

The WTI and Brent crude futures contracts continue to trade within relatively narrow ranges, with WTI between USD 76 and 80, and Brent between USD 81 and 84, with the technical-driven trade the focus at a time when the fundamental drivers have struggled to dictate the direction of prices.

Overall, we maintain the view that Brent and WTI will likely remain rangebound, respectively around USD 80 and USD 75 per barrel during the first quarter and next, but with disruption risks in the Middle East and OPEC+ production restraint potentially leaving the risk/reward skewed to the upside. In the short term, the market will be focusing on WTI and whether traders will be successful in pushing the price through resistance just below USD 80, a level that was unsuccessfully challenged last week. Brent, meanwhile, has got more work to do before potentially attempting a breakout, with the level to watch for that to happen being somewhat higher at USD 85.

Some underlying fundamental strength has emerged this past month with widening price differences between monthly contracts indicating a more robust outlook across parts of the physical market. In the short term, the focus remains on the Red Sea where Houthi attacks continue and next week’s OPEC+ meeting which is expected to yield an extension beyond March of the current agreement to keep production curtailed.