By Ole Hansen, Head of Commodity Strategy at Saxo

- Broad gains drive the Bloomberg Commodity Index to a three-month high

- Strength in energy and industrial metals point to end of year-long consolidation

- Copper at an 11-month high supporting strong week for copper miners

- Crude oil pops on IEA flip, but is it enough to break the long-held range?

- Silver and copper strength supporting gold despite yield and dollar headwinds

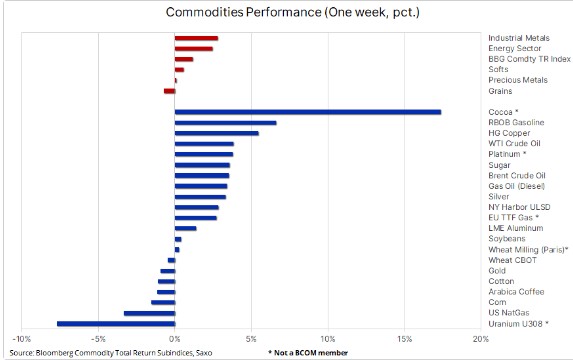

The commodity sector recorded a third consecutive weekly gain, and while it was precious metals and softs attracting most of the attention at the beginning of March, we have during the past couple of weeks seen strength across all sectors with wheat and uranium being two of the notable exceptions. The Bloomberg Commodity Total Return Index, which tracks a basket of 24 major commodity futures spread evenly between energy, metals, and agriculture, reached a three-month high, and it has raised the question whether the year-long consolidation phase is ending?

WTI and Brent crude oil reached four-month highs after the IEA flipped their 2024 supply and demand forecast to a deficit amid an expected prolonged period of production cuts from OPEC+. Supported by silver, gold meanwhile remains resilient, holding onto most of its recent strong gains despite dollar and yield strength following stronger-than-expected CPI and PPI prints this week. Data which led the market to conclude the US Federal Reserve will adopt a cautious stance and would like to see more evidence of inflation falling towards the 2% target. As a result bets on a 25 bp rate cut in June fell to 75% from 95% at the start of the week.

Copper and copper miners meanwhile attracted a great deal of attention after the King of Green metals reached an 11-month high following a 6% jump supported by already tight market conditions potentially made worse by the prospect for Chinese smelters cutting production. Iron ore (down 30% YTD) slumped below USD 100 per tonnes as China’s property crisis will continue to keep a lid on steel demand. Uranium’s long-term upside potential remains intact despite recent stop-loss selling from investors who got caught up in the January buying frenzy.

The agriculture sector saw cocoa reach a fresh record at USD 7700 per tonnes, more than three times the five-year average price. The New York futures contract trades up 87% on the year as a production shortfall in West Africa shows no signs of improving. Hedge funds, meanwhile, continue to hold onto a near-record grains sector short, led by corn and soybeans, a risky bet ahead of the Northern Hemisphere planting and growing season, where weather developments will become the key focus.

Copper and copper miners break higher on China smelter curbs

Copper and copper mining stocks pushed higher this past week with HG copper breaking above USD 4 per pound and LME above USD 8700 per tons to reach 11-month peaks, while ETFs tracking copper mining stocks surged by more than 6%. Over the past month, the metal has steadily climbed, buoyed by a weakening dollar, optimism in post-Lunar holiday demand in China, and material downgrades to 2024 mine supply increasingly tightening market conditions. Several mining companies have announced production downgrades due to factors like increased input costs, declining ore grades, rising regulatory expenses, and weather-related disruptions.

The latest rally pushing prices higher, was fueled by Chinese smelters reaching a rare agreement to jointly cut production of refined metals to cope with shortages of raw material. China, the world’s largest copper production hub, has witnessed smelters vie for scarce supply by slashing their processing fees, resulting in a downward trend in treatment and refining charges to near zero.

Furthermore, the ongoing green transformation is augmenting demand from traditional sectors like housing and construction. An anticipated initiation of a US rate-cutting cycle later this year may prompt companies, which depleted inventories last year to mitigate funding costs, to restock. We maintain our long-standing bullish stance on copper, and with copper miners also exhibiting signs of resurgence, the possibility of a fresh record high in the second half of the year appears achievable.

Lithium sector stabilising amid production cutbacks

Lithium, a key component in rechargeable lithium-ion batteries, shows signs of stabilising after producers, responding to an 80% price collapse last year, have started to trim production, potentially by as much as one-third according to analysts. During the past month, we have seen similar initiatives by US natural gas producers who have made temporary cutbacks to support prices and to bring down an overhang of stocks, currently more than 37% above the five-year average. Developments that for both commodities support the old saying that the best cure for low prices is low prices as it lowers production while for some commodities stimulates demand.

While spot Lithium has stabilized it is interesting to note that the China Lithium Carbonate 99.5% benchmark has rallied by 21% so far this year, potentially signaling improved fundamentals. Meanwhile, the Solactive Global Lithium Index, which tracks the performance of 40 of the largest and most liquid lithium-related companies, trades down around 11% during the same period. The index includes well-known names like Albemarle Corp, TDK Corp, and Pilbara Minerals, some of which have been weighed down by heavy short selling from hedge funds, but with sentiment showing signs of improvement, these shorts are now at risk, leaving the sector exposed to further gains should the recent recovery continue.

Crude oil at four-month high on IEA flip

In our mid-week crude update, we highlighted how the recent lack of a price catalyst had pushed the four-week rolling average trading range in WTI and Brent to a ten-year low. Crude has nevertheless been seeing a steady but calm ascent since December, when Houthi attacks on ships in the Red Sea raised the geopolitical temperature while supporting tighter market conditions with millions of barrels of crude and fuel products being stuck at sea for longer.

However, since then the combination of Ukrainian drone strikes on Russian refineries, which according to estimates may reduce Russia’s refinery runs by 300k barrels per day in 2024, and not least the IEA flipping their 2024 forecast to a deficit, both help drive WTI and Brent higher. In their latest Oil Market Report (OMR) for March, the International Energy Agency (IEA) raised their global oil demand forecast to 1.3 million barrels per day, while shifting their balance for the year from a surplus to a deficit based on the assumption OPEC+ will maintain current production curbs through 2024.

Ahead of the IEA news, crude prices had slipped after the Energy Information Administration (EIA) raised their US crude production forecast to a record 13.65m barrels/day in 2025 from 13.19m barrels/day this year, while OPEC in their latest monthly update wrote supply cuts had stalled as Iraq for a second month produced around 200k barrels/day above its quota.

Brent crude broke above former resistance in the USD 85 per barrel area, but lack of follow-through buying ahead of the weekend potentially highlighting a market that remains range-bound, but with a small upward bias. Using Fibonacci retracement levels, the next key resistance is located at USD 88 per barrel.

Gold enjoys the tailwind from copper and silver strength

Gold continues to show a great deal of resilience, having so far given back less than 40 dollars of the 170 dollars it gained during the previous two weeks. This during a week that saw stronger-than-expected US inflation data from CPI to PPI potentially delaying the beginning of the US rate cut cycle. The data prints helped send US treasury yields higher while the dollar recorded its first weekly gain in four. However, countering these developments was the mentioned rally in copper which drove a gold-supportive run higher in silver.

Underlying support has for months been provided by central banks, some of which are buying gold to reduce their exposure to the dollar, and continued strong demand from retail investors in Asia, most notably in China where stock market weakness and falling property prices are forcing the middle class to look elsewhere. In the short-term, some of that demand may slow while investors adopt to the new and higher price level, but with heightened geopolitical tensions reducing short-selling appetite, we feel that gold’s current buy-on-dips credentials has only been strengthened.

Without participation from ETF investors who remain net sellers, the recent rally has primarily been driven by under-invested hedge funds who rushed back onto the long side after several key resistance levels were broken. In the week to 5 March when gold rallied 4.8%, money managers such as hedge funds and CTAs bought 63k futures contracts (195 tonnes), the biggest one-week increase since June 2019, and with buying extending into the following period, this group of traders now hold an elevated position, that needs to be protected, potentially another reason why gold has not been allowed to fall in response to this week’s yield and dollar rally.

While perplexed about the timing of the latest surge to a record, occurring despite the prospect for a delayed start to the US rate cutting cycle, we maintain our USD 2300 target with the technical picture potentially pointing to an even higher level around USD 2500. In the short-term the risk of a deeper correction to USD 2135, the December 4 high, cannot be ruled out. Silver meanwhile needs to build a base in the USD 24 to 24.50 area from where it may attempt to mount a fresh attempt at the April 2023 highs around USD 26.