US corporate bonds today have an attractive risk-return profile and offer an excellent diversification for a diversified portfolio, says Georgios Costa Georgiou, Managing Director Global Head Fixed Income Product Specialists of Allianz Global Investors. He is referring both to short-term high yield paper and to investment grade commercial paper that combines longer durations with lower risk. Additional advantages of the US credit market include the enormous supply and liquidity as well as the generally negative correlation with longer-term government bonds and equities.

First pillar: high yield

For five years now, Georgiou has focused on fixed-income investments and US bonds, but for years, when interest rates were extremely low, he was a voice with only a few listeners. ‘Today and actually since the second half of 2023, I am being heard again because at the moment these are attractive times for bonds, which have clearly made a comeback. We see interest from parties who, unlike pension funds and insurance companies, are not obliged to buy bonds.’ Firstly, the product specialist is seeing an opportunity in the US with regard to short-term high yield. High yield bonds generally offer a higher yield than investment grade bonds in order to compensate investors for the higher risk associated with investing in issuers with a lower rating.

And why are US high yield corporate bonds attractive today, also for non-Americans? ‘Because this is one of the largest markets for commercial paper in the world. In five years, it has doubled in size to about 1,000 billion US dollars. In other words, there is a great deal of choice while at the same time the market is very liquid. This expansion has been driven by an influx of companies with lower credit ratings that gained access to the capital markets, as a result of which the liquidity and diversity of the market have increased.’ All these elements also make this market attractive for European investors. ‘Furthermore, the US economy is growing at an annual rate of 3%, which is faster than in the rest of the world. There is hardly any growth in Europe and that weighs on European companies, especially those that depend on the European market or must export to China.’

Attractive characteristics

In contrast to their counterparts with a higher rating, high yield bonds often have shorter maturities, averaging about four to five years, while issuers with a higher credit rating, such as JP Morgan or Bank of America , can issue bonds of 20 to 30 years. ‘These high yield bonds therefore offer a high interest rate, an average annual return of 7.89% since 2009, combined with a short duration, 2.4 on the American high yield market for the moment. Duration is not exactly the same as maturity; it measures the sensitivity of a bond to a change in the interest rate. This shorter maturity also provides investors with additional benefits such as a better visibility of the company and less exposure to long-term interest rate fluctuations. After all, you have no idea where the interest rates will be in 10 years’ time. It is these two elements that make the risk/return profile so attractive.’

He also points out that shorter duration high yield bonds make them less sensitive for interest rate risks and, as remarkable as it may seem, they offer investors a defensive buffer during periods of market volatility. ‘They provide protection against downward risks, but carry most of the upward return during market upswings. This defensive characteristic was particularly evident during periods of interest rate volatility, such as in 2022 and 2023. Furthermore, short-term high yield bonds have historically exhibited lower rates of default than their longer-term counterparts, further enhancing their appeal to investors seeking income stability and capital preservation.’

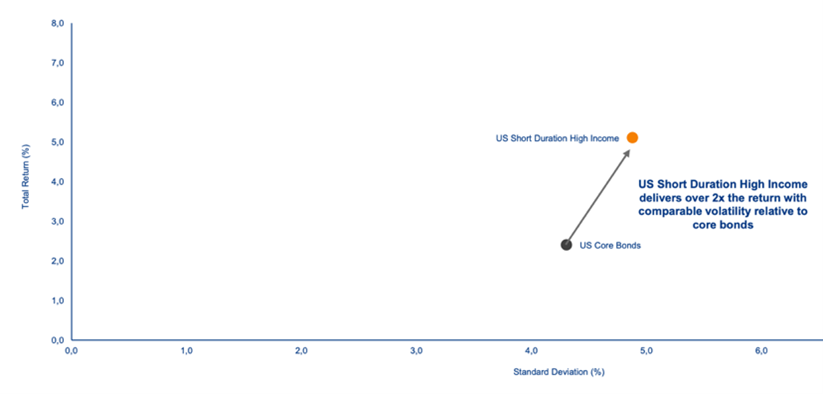

Lower volatility

To top it all off, he adds that the volatility (expressed in standard deviation) of US short-term high yield paper is only slightly higher than that of US Core Bonds (a portfolio consisting of IG corporate bonds and government paper) but that the return is higher. ‘It is a striking finding of which many investors are not aware. They immediately assume that high yield means high risk, but that is not the case at all.’

And what can we expect for the market segment if the interest rate starts to fall, as is generally expected? ‘In a scenario of falling interest rates, it is above all these bonds that will benefit due to their lower duration. Indeed, the widely prevailing expectation is that the curve will become steeper. So, the rates in the shorter term will fall more than those in the longer term. We make the assumption that longer interest rates, such as the 10-year rate, will probably not fall so much because more and more market participants are starting to worry about the growing budget deficit.’

Finally, Georgiou mentions one of the group’s funds, Allianz US Short Duration High Income Bond, as one to benefit from this market segment. As an individual investor, it is virtually impossible to compose a portfolio of this type of paper yourself. ‘The managers of this fund focus on credit quality; given that the economic circumstances and fundamentals of companies play an important role in bond performance. By conducting rigorous credit analyses and selecting bonds issued by financially sound companies, investors can reduce the risk of default and increase the resilience of their portfolios in fluctuating interest rate environments,’ he concludes.

Second pillar: investment grade

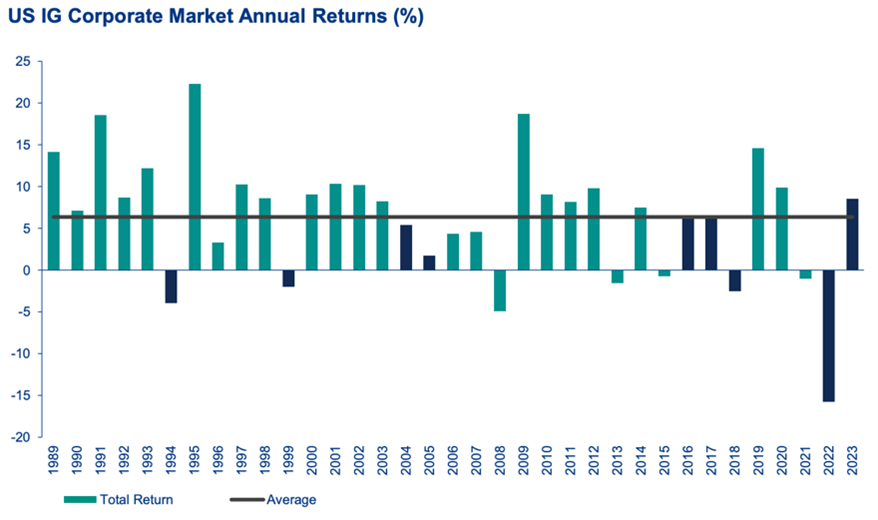

Georgios Costa Georgiou then switches the focus to another aspect of the US credit market, namely investment grade paper. He also finds this market segment, characterised by issuers with a higher credit quality, one that is attractive to include in a diversified portfolio because it has a different risk-return profile that perfectly complements the short-term high yield segment. ‘Investment grade bonds generally have a longer maturity and a lower yield compared to high yield bonds. However, they offer more stability and a lower risk of default, making them suitable for risk-averse investors looking for stable income flows. Investment grade bonds are issued by companies with a strong credit rating, generally BBB or higher, as judged by major credit rating agencies such as Moody’s, Standard & Poor’s, and Fitch Ratings.’ The US IG market is one of the most liquid markets that exists. Moreover, the rate of default is historically very low, at less than 0.5%, because the universe is made up of large and high-quality blue chip companies. Since 1989, this market segment has produced an annual return of approximately 6% (see below).

On the other hand, investment grade bonds also offer stability and diversification advantages, above all in periods of economic uncertainty. Historically, there are hardly any defaults. ‘This investment category has historically shown little correlation with equities and riskier segments of the fixed-income market, such as emerging markets and high yield, which were discussed above. Compared with government bonds, the segment offers an extra annual return of 1 to 2%.’

Allianz fund

The Managing Director of Allianz Global Investors mentions the fund AllianzUS Investment Grade Credit as one to benefit from this market segment . ‘The investment philosophy with the fund is simple: we perform a bottom-up selection to identify attractive issuers. We limit ourselves to USD-denominated investment grade commercial paper and avoid other types of bonds and credit positions. Moreover, we do not take a position on duration. Our strategy is predominantly focused on active management, whereby 80 to 90% of the added value to our funds is supplied by the careful selection of securities.’