We expect the BOJ to hike again this year and beyond

Zhennan Li, Senior Asia Economist, Pictet Wealth Management.

- We expect the Bank of Japan (BoJ) to tighten its monetary policy again this year, with the overnight call rate rising to 0-0.25% from 0-0.1%. Our baseline case is that the BoJ will hike in July, but this is a very close call, especially given the bank’s cautious and opportunistic approach to normalising its monetary policy, meaning the next rate hike could be delayed until October.

- We also expect the BoJ to hike beyond this year, with the policy rate gradually approaching the bank’s nominal neutral rate.

- The main unknown is whether inflation can be sustained at around 2%. If inflation overshoots, we could see a more aggressive rate-hiking cycle, but if inflation undershoots the cycle could be shallower.

BOJ TO HIKE AGAIN THIS YEAR

We expect the BoJ to hike further this year, with the uncollateralised overnight call rate moving up to 0-0.25% from 0-0.1%. There are three major reasons for this expectation:

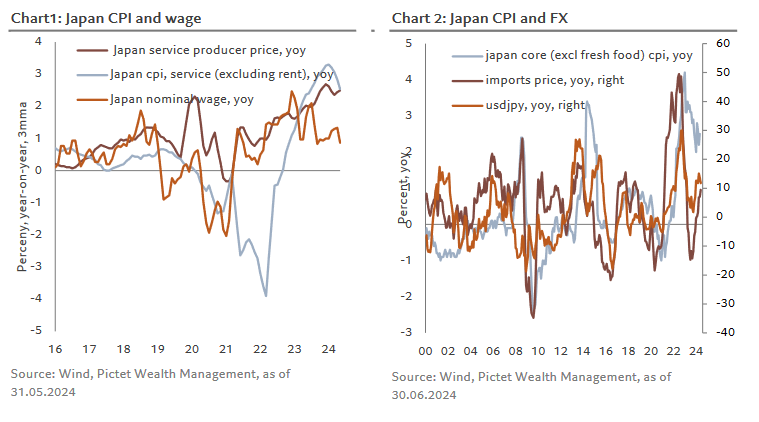

First, the BoJ has grown increasingly confident that a virtuous cycle is forming be- tween wages and inflation. While monthly CPI inflation data has been fluctuating, the BoJ is more focused on underlying inflation and inflation expectations to gauge whether its 2% inflation target can be achieved sustainably. Several measures of un- derlying inflation monitored closely by the BoJ have been rising. One major factor for this is BoJ research showing that services inflation is increasingly sensitive to wage growth (Chart 1).

Second, comments made at its June meeting suggest the BoJ is more and more con- cerned about the yen’s ongoing decline and the first-round impact of this on inflation (empirically, a 10% change in the exchange rate leads to a change of around 20bps in consumer inflation, with a six-month lag, Chart 2). The depreciation of the yen could also have a second-round effect on inflation through wage growth (for in- stance, upward pressure on inflation in coming months could have an impact on next year’s Shunto wage negotiations).

Third, after contraction in Q1 due to one-off factors, economic growth should re- cover in the coming quarters, perhaps to a level beyond Japan’s long-term potential. This could lead to an improvement in the output gap and put upward pressure on inflation. Household consumption has been weak, but summer tax cuts and higher wage growth could help it recover in the coming quarters.

WE EXPECT THE BOJ TO HIKE IN JULY, BUT IT IS A VERY CLOSE CALL

The BoJ could hike either in July or October (when it will update its economic out- look). Our baseline case is that the BoJ will hike in July, but it is a very close call. Market expectations for a hike this month have dropped since the BoJ announced that details of its plans for reducing its JGB purchases will be unveiled at the end of this month. Yet at its June meeting, the BoJ’s governor argued that it was possible to hike rates and reduce JGB purchases at the same time (depending on data). A bunch of important data will be released before the BoJ’s July meeting, including the Q2 Tankan business survey as well as labour market and inflation data, the final result of the Shunto wage negotiations, the BoJ’s regional economic reports, etc. Most data released so far support a hike in July, as does the yen’s continued weakness. But there is an argument for waiting until October, when the BoJ will have more information on the passthrough from wages to services inflation and household spending. Delaying the next rate increase to October would be in keeping with the BoJ’s cautious and opportunistic approach to normalising monetary policy.

WE EXPECT THE BOJ TO HIKE BEYOND THIS YEAR

At its April meeting, the BoJ mentioned that its policy rate would approach the nominal neutral rate in the second half of its forecast period (FY 2024-2026) as it ex- pects to reach its target of a sustainable 2% rate of inflation by then.

There is much uncertainty around what the neutral rate level is in Japan. The BOJ has mentioned a wide range of between -1% and 0.5% for the real neutral rate. Gov- ernor Kazuo Ueda said in March that the current real interest rate of around -1% (as- suming inflation expectations of around 1%) is likely to be significantly below the real neutral rate, suggesting he thinks it is probably above -0.5%. Based on the index constructed by the BoJ, medium- to long-term inflation expectations are currently around 1.5% . This figure could rise to 2% if the inflation target is achieved sustaina- bly.

After decades of low growth and inflation, the BoJ does not want to jeopardize Ja- pan’s recovery, which is why we expect it to tighten policy only gradually in the coming years, until its policy rate approaches the neutral rate.

RISK

Achieving its sustainable 2% inflation rate is the main rationale for the BoJ to keep normalising monetary policy. Reaching this target hinges to a large extent on a vir- tuous cycle between wages and inflation. If the passthrough from wages to prices is not as strong as expected (since Japanese economy had been in deflation/low infla- tion for such a prolonged period), leading to inflation undershooting, then the hik- ing cycle could be shallower. By contrast, we could see deeper rate hikes if inflation overshoots or if concerns about yen depreciation grow.