The US equity market rejoiced last week in the de-escalation of the trade war with China. As of last Friday, the S&P500 was 5.8% above the level hit on the eve of “Liberation Day”, albeit still 3% below its recent peak on 19 February. Yet, a 30% tariff hike on China would still be a hard pill to swallow for the US economy, especially as the agreement with the UK the previous week suggested that it would be difficult to expect a rate below 10% on any country hit by reciprocal tariffs. The weighted average tariff – assuming the 30% rate on Chinese products becomes permanent and the specific add-ons for other countries are suspended beyond the end of the 90 days negotiation phase, due to expire in July, but still taking on board the 25% specific hit on steel, aluminium and cars – would still rise by some 15 percentage points, reaching its highest level since the Hawley-Smoot days of 1934, and still enough to lift US inflation by roughly 1.5%. This is of course better than the 30% hit after Liberation Day and the further escalation with China, but still a very large shock. We suspect the equity market is also responding to a potential shift of the White House’s focus away from trade to more business-friendly matters, such as de-regulation and tax cuts. On 14 May, the House Ways and Means Committee approved a tax legislation titled “The One, Big, Beautiful Bill” (it’s the official name, OBBB in this note). The bulk of the bill is about prolonging the TCJA provisions due to expire, but there are “enhancements” which would lift business profitability in the US. The cut in the headline corporate tax rate from 21% to 14% - a campaign proposition – has gone out, but accelerated amortisation schemes, for instance for R&D efforts conducted in the US, and tax breaks for opening new factories, would still reduce the overall corporate tax bill. There would also be gains for households. While the OBBB does not go as far as to exempt social security pensions from income tax – another campaign pledge – senior citizens would still benefit from a specific exemption of USD4,000 dollars a year. Interests on car loans would also become deductible (for cars made in the US). In line with the campaign promises, tips and overtime would become tax exempt.

There is however less positive news for foreign investors in the US. Indeed, the OBBB contains elements which could raise the taxation of dividends and interests remitted to non-residents. Section 899 of the bill would levy an incremental tax of 5% every year (up to a maximum of 20%) on financial income generated in the US accruing to residents of foreign countries imposing “unfair” taxation on US companies. The definition of such “unfair” practices is wide: on top of the OECD sponsored Under-Taxed Profits Rule – basically the minimum global 15% corporate tax – this would also cover Digital Services Taxes, implemented in several EU countries and in the UK, which the US considers as weighing disproportionately on US Tech companies. In other words, the bill is being “weaponised” as part of the trade war expanded to services which we discussed last week. The House is handing the President a key bargaining chip in the current negotiations, although one which, should it be exercised, would probably be counter-productive for the US interests down the line (more on this later).

The vote in the Ways and Means Committee on 14 May was still only a first step in what could be a complex process. The bill has failed to get through the House Budget Committee last Friday, with a 16 to 21 votes, as some fiscally conservative Republican Representatives rejected it on grounds of fiscal sustainability, calling for more offsetting action on the spending side.

They have a point. The Yale Budget Lab has estimated the impact of the OBBB (see link here). Their conclusion is that the Bill in its current form would cost USD 3.4 trillion over 2025-2024 and USD 5trn over the same period should the temporary measures of the OBBB made permanent. It is probably easier to read this in terms of deficit to GDP ratio: according to the Yale Budget Lab estimates, the OBBB would bring the US deficit to 8% of GDP by 2034 (if made permanent) and 7.2% (if only temporary), bringing public debt in a 120/130% of GDP range. This is despite the abolition of most IRA tax incentives, which goes beyond electric vehicles but will also affect projects in renewable energy.

There are two natural “offsets”. One would be to follow the Republican fiscal conservatives call for more spending cuts on healthcare via Medicaid. Under current plans, most Medicaid recipients would need to complete 80 hours per month of work, education or volunteer activities, and co-payments (in clear financial participation from patients) would become mandatory for certain individuals above the poverty line. Financial transfers to states using their own funds to provide healthcare to undocumented migrants would be curtailed. Yet, according to the House Republicans’ communication, those plans would reduce the deficit by c. USD625bn over 2025-2034, i.e. offsetting only one fifth of the impact of the tax cuts in the most favourable scenario (taking on board only temporary measures). This is encouraging the fiscal hawks in the Republican party to demand more cuts, but according to the CBO’s estimates, several millions of Medicaid recipients would already be cut off from the system in the current version of the plan, and on the other side of the spectrum within the Republican caucus, more “populists” members are already voicing their discomfort with altering what has been a key plank of the US welfare state since the 1960s. Trade tariff income is the other natural offset, and habitual readers of Macrocast will know that this is a key reason why we think there is a high floor to additional concessions on this front.

As we write on Sunday night, House Republicans are still trying to find a compromise, but they have little capacity to absorb dissent – they have only a 4-seat majority margin. Getting a House vote would not be the end of story. Since the Republicans are using the reconciliation process to avoid filibustering, the same legislation needs to be agreed by the Senate and the House. Some Republican Senators have already voiced their intention to modify the House’s draft. If a modified version is voted by the Senate, a conference would need to be set jointly with the House, and any compromise legislation resulting from such conference would still need to be voted in the same terms by both the House and the Senate.

If a compromise is found at the House’s Budget Committee to overcome the hawks’ opposition, a full House floor vote is targeted for 26 May. If successful, this would then go to the Senate. The aspirational deadline for the finalisation of the process is 4 July, but there could be numerous obstacles on that timeline. We note that the Treasury has been warning about the exhaustion of the “extraordinary measures” by August. Irrespective of the agreement on the full bill, in any case the debt ceiling will have to be pushed again by then.

Section 899 could be one of the issues at stake in the negotiations, given its potentially counter-productive aspects. Indeed, what it could ultimately amount to is a reduction in the real rate of return on US assets held by non-residents. This would be close to the ideas put forward by Stephen Miran which we discussed a few weeks ago, intended to trigger a depreciation of the US dollar with the risk – explicitly recognized by Miran himself – that US funding costs rise further. A bit like with tariffs, the US would ultimately penalise its own economy when trying to punish overseas stakeholders. Such tax on overseas holdings of US assets would also run counter one of the stated objectives of the tariffs, i.e. attracting investment on the US territory.

Moody’s decision on Friday to remove the US sovereign of its AAA rating may be symbolic – it was the last agency which had not yet done so - but it should draw attention to the daunting fiscal challenge facing the United States. Beyond the lack of clarity on the budget choices, section 899 could add to the pressure on long-term interest rates. When forecasting the deficit’s trajectory, the Congressional Budget Office is assuming a return of 10-year yields to 4.0% by the end of the year, down from 4.5%. This is still possible, assuming a swift transmission of Fed cuts to the whole curve when – as we think – the tangible effects of the current policy stance on the labour market materialises in the second half of the year. Still, a concern over a persistent “risk premium” attached to US bonds could very easily jeopardize such transmission.

European – and French - complications

Europe’s policy set-up has received less attention recently. Yet, Europe is also facing its own internal difficulties. Negotiating with the US on trade is the first urgency. We discussed last week how we thought that the UK-US deal suggested Brussels should brace itself for tough talks with Washington DC. We note however that at least a formal process has started: the EU and the US have exchanged documents last week for the first time, according to the Financial Times. A particular issue for the EU – which is specific to its institutional setup – is that on top of finding an agreement with the “other side”, maintaining consensus across member states could be a challenge. Still, given the volatility triggered by the new policy stance in the US, by contrast, Europe appears as a source of stability, while Friedrich Merz’ shift to a significant catch-up in public spending offered a source of optimism on the medium-term macroeconomic prospects for the Euro area, even if the impact is not likely to materialise quickly.

Europe’s political life remains fractious, with potential adverse effects on the quality of the policy response, but for now the central tenets of the region’s policy choices remain intact. In Germany itself, F. Merz’ difficulties in controlling his parliamentary majority, illustrated by the failure of the Bundestag to elect the new Chancellor in the first round, may signal that the delivery of the new fiscal course could be less swift than expected. Still, it may not be surprising that the new coalition faces internal stress given the magnitude of the proposed policy shift. To some extent, this tension is proof of the cultural revolution on fiscal issues now in motion in Berlin. In Portugal, the push by Chega in the snap parliamentary elections on Sunday, coming neck and neck with the Centre-left for the second-biggest party position, illustrates the persistence of the far-right attractiveness across Europe, including in parts of the region which were seemingly immunised so far from that temptation. Yet, the centre-right strengthened its position, winning 32% of the votes against 28% last year. It will still be a minority government, but broad coalitions – or supply and confidence agreements – are common in Portugal. The overall policy stance will not change. Outside the Euro area, In Romania, higher turnout allowed the centrist candidate to defeat his far-right opponent who had won the first round. It is likely that the campaign will leave scars – and Mr Simion initially indicated he would not necessarily accept the result - but again, the pro-European stance prevailed. Where the outcome is more uncertain is in Poland, where the centrist candidate to the presidency only barely did better than his main opponent from PIS, and where the high overall score of the various nationalist candidates leaves the second round quite open. Still, while failing to dislodge PIS from the Presidency would make Prime Minister Donald Tusk’s full reform project more difficult, his overall policy stance would change very little.

Still, while the institutional levers in Europe may remain for now remain reasonably firmly in mainstream hands, outside Germany some policy limitations remain dauting given the lack of fiscal space. France is a good example. Political life has become less volatile there lately despite the lack of a majority in parliament. Yet, the fiscal equation remains extremely difficult to solve, and this matters for the entirety of the Euro area. Indeed, while Germany should be able to contribute positively to euro-wide economic activity in the years ahead, France will likely “pull in the other direction”, since a significant fiscal adjustment is unavoidable.

France’s public deficit stood at 5.8% of GDP in 2024, the highest in the Eurozone. While the average deficit in the EU decreased in 2024, France’s deficit increased by 0.4 percentage points compared to 2023. Public spending reached 57.1% of GDP, slightly below the average observed since the 2008–2009 crisis (57.8%). However, this average was mechanically elevated due to COVID-19 costs, and France’s spending remains 8 percentage points above the Eurozone average—a gap that has remained stable.

Public debt was 113.0% of GDP at the end of 2024, up from 109.8% in 2023. France’s debt is notably higher than the Eurozone average of 89% of GDP, with only Greece and Italy exhibiting higher debt ratios. The gap between France’s debt and the Eurozone average has been widening (see Exhibit 1). French debt was below the area’s average at the beginning of monetary union. It converged to the average in the years following the Great Financial Crisis of 2008 and the subsequent European sovereign crisis. Then, while debt has stabilised since the middle of the previous decade in the Euro area beyond the one-off shock of the pandemic, it has continued to rise in France. This deterioration in France’s relative position cannot be explained by weaker economic growth, as French GDP has been growing at a similar pace to the Eurozone average—slightly above 1% annually.

What correction is planned? Given the complex political situation, France’s budgetary planning beyond the current year is quite imperfect. The latest Medium-Term Budgetary and Structural Plan (PSMT), detailing necessary adjustments through 2029, was prepared by the Barnier government and submitted to the European Commission (EC) in October 2024. By construction, it could not account for the failure of the finance bill and the arrival of a new government team. In April 2025, the Treasury submitted a “recalibrated” version for 2025 to the EC, reflecting final 2024 results and early-year budget decisions, but it does not provide much detail for the 2026–2029 phase beyond generic targets. For 2025, the government aims to reduce the budget deficit by 0.4 percentage points of GDP, to 5.4%, compared to 5.0% projected in the October PSMT. This is despite the 2024 deficit turning out lower than previously estimated (6.1%). Thus, the planned fiscal consolidation for this year has been downgraded from 1.1% of GDP to just 0.4%. This underperformance is only marginally due to a downward revision of expected growth (–0.4 points, to 0.7%), which mechanically worsens the deficit by 0.2 percentage points of GDP. The main reason is an upward revision of the forecast for net expenditure growth in volume terms—from 0% in the October 2024 PSMT to 0.9% in the April 2025 update. The reduced ambition for 2025 mechanically shifts the bulk of the adjustment effort to 2026 and 2027—an election year—in the April PSMT update. It anticipates adjustments of 0.9% of GDP in 2026 and 0.7% in 2027 (without indications on the type of measures which could be implemented). Even under these conditions, and assuming growth returns to trend in 2026 and 2027, the deficit would still be 4.1% of GDP in 2027, only falling below 3% in 2029, as projected in the October version. Public debt would reach 118% of GDP in 2027, beginning to decline only from 2028.

What will happen if no action is taken? Given the macroeconomic headwinds, in a “normal” configuration for fiscal policy, the government could or even should opt for postponing the adjustment further, but such approach would be quite risky given the magnitude of the current fiscal imbalances. To illustrate this, one possible approach is to simulate a path for the deficit and debt assuming that the primary structural deficit, i.e. the share of the deficit which cannot be ascribed to the cycle or to the interplay of interest rates and debt, stays at its current level. This is what the French Treasury presented in one of the illustrative scenarios provided in the October version of the PSMT. In this case, and assuming GDP grows in line with trend, public debt would rise from 113% of GDP in 2024 to 122.2% in 2027 and 136.6% in 2031. Debt would then maintain an unsustainable trajectory, potentially reaching 180% of GDP by 2041 (see table 44 in the document linked here).

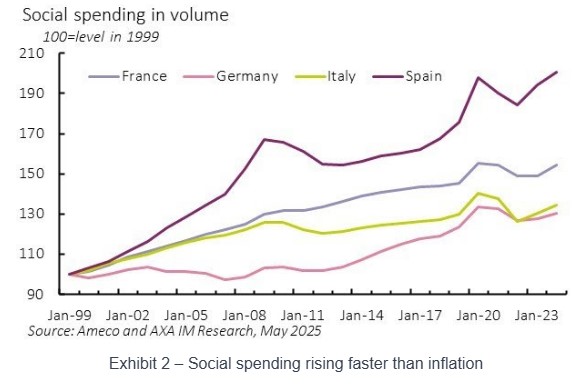

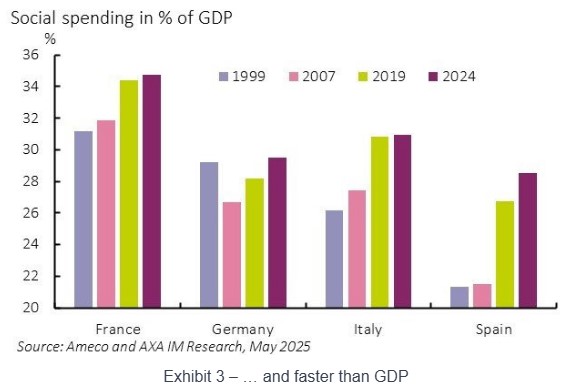

This may even be a too benign simulation, since merely keeping the structural deficit stable would probably require some corrective measures. Indeed, social spending in France has been growing faster than inflation in an almost linear fashion when correcting for the shock of the pandemic (see Exhibit 2, which shows social spending in volume, i.e. adjusted for inflation). Among the four biggest economies, only Spain has seen a bigger gap with inflation. Yet, in the latter case, this appears more as a “catching up process” and social spending in Spain as a percentage of GDP remains lower than in France, Germany and Italy (see Exhibit 3). France has been ranking first on social spending consistently over the last 25 years. This is not attributable to a systemic extension of the French welfare state during the period, but rather to the effect of demographic change combined with the institutional features of social protection. The French pay-go pension system alone explains c.3 GDP points of the spending gap with the Euro area average.

Illustratively, instead of keeping the structural deficit unchanged, in a different simulation, we allow social spending to rise in line with its 25-year trend, i.e. twice as fast as inflation (3.5% per annum against 1.7%), assuming GDP grows in line with potential, total public spending would rise by 3 % of GDP over the next 10 years if the rest of government expenditure merely rises in line with GDP. In a configuration in which tax would also rise in line with GDP – no discretionary tax hike – the deficit would also rise by three percentage points.

Of course, in such a “business as usual” scenario, with the deficit steadily growing, interest rates would likely rise. The Treasury’s central scenario in the PSMT assumed a plausible interest rate of 3.7% for 10-year bonds in 2027, which is 40 basis points higher than current rates. In the “unchanged structural deficit scenario”, even if the 10-year rate remains at 3.7%, the “snowball effects” would be significant: interest payments would increase from 2.1% of GDP in 2024 to 2.8% in 2027 and 3.8% in 2031. If market developments are more adverse than planned, as a simple benchmark, each 100-basis point increase in interest rates results, after 10 years, in an annual debt servicing cost increase of another 1 percentage point of GDP.

In a nutshell, significant and lasting discretionary restrictive action will be needed in the years ahead to keep the French debt trajectory under control. This would offset some of the new German fiscal effort. Assuming no Euro-wide fiscal initiative materialises, this would likely put even more pressure on the ECB to maintain accommodative conditions for the Euro area as a whole. Of course, the central bank would probably want to be certain that such fiscal policy shift is effectively implemented to take it on board in its own reaction function, and this may necessitate a political clarification in Paris.