By Virginie Wallut, Director of Real Estate Research and Sustainable Investment, La Française Real Estate Managers While in 2024, there was a rebound in investment volumes, the first quarter of 2025 reveals a certain stability in European commercial property markets. However, this stability masks contrasting dynamics across regions, highlighting a still fragmented recovery.

Even though the European Central Bank (ECB) has continued to cut interest rates, several tension factors continue to hinder a genuine easing, thereby preventing a lasting decline in long-term rates, a key condition for a significant compression of real estate yields. The ECB’s more accommodative monetary stance contributes to the steepening of the yield curve, strengthening the relative appeal of real estate products.

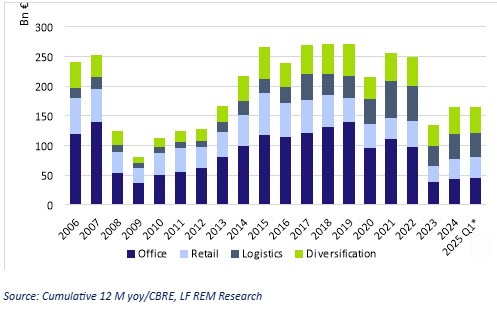

Investments: contrasting regional dynamics

In the first quarter of 2025, €36.6 billion were invested in commercial real estate property, bringing the total for the past 12 months to €165 billion. The market seems to have entered a consolidation phase following the adjustments observed in 2023 and 2024. Relatively speaking, European investors are increasing their presence, accounting for up to 40% of volumes invested, while North American flows are declining amid latent geopolitical uncertainty. Investment dynamics across Europe were mixed in the first quarter of 2025. In France, investment volumes increased by 41% year-on-year, while Germany and the UK saw respective declines of -7% and -31%.

In the first quarter, the retail and office sectors saw significant growth in their investment volumes, with increases of 17% and 25% respectively, after a phase of value adjustments.

Investment volume in commercial real estate in Europe (€ bn)

Moderate yield compression

In the first quarter of 2025, prime office yields in Europe showed slight declines, reflecting a renewed investor interest in this asset class following a period of significant value correction and improved financing conditions.

At the end of March 2025, prime office yields in European capitals ranged from between 4% and 5% (Paris 4.2%; London 4%; Milan 4.5%; Amsterdam 5%; Berlin 4.8%; Madrid 4.85%) while in major regional cities prime yields varied from 5.5% to 6.5% (Lille 5.85%; Lyon 5.5%)[1].

Investors remain highly selective, favoring well-located assets that comply with the latest technical and environmental standards, while secondary assets remain under pressure with higher yields and lower demand.

Contrasting recovery in take-up

Take-up in Europe is increasing slightly, although companies remain cautious. This recovery remains contrasted across markets. Berlin recorded a 25% year-on-year drop in take-up, reaching its lowest level since 2013, while Frankfurt and Dublin saw take-up more than double over the same period. Demand remains focused on modern assets. In order to stay competitive, investors are encouraged to spend capex to renovate assets. Supported by a focus of demand on high quality assets, prime rents continued to rise in the first quarter of 2025 but at a slower pace than in 2024.

Supply in Europe continues to grow, fueled by new developments initiated before the crisis and slowing demand, as well as vacancies motivated by real estate rationalization strategies. Only three cities - Hamburg, The Hague and Madrid - saw their vacancy rates fall in the first quarter of 2025[2].