Xiao Cui, Senior Economist, at Pictet Wealth Management, ahead of this week’s Fed meeting.

The Fed is widely expected to remain on hold this week, and we expect the Fed will maintain this stance through at least the summer. Since the last FOMC meeting, inflation has slowed, growth has softened marginally, and trade tensions have eased. Chair Powell is likely to reiterate that monetary policy is well positioned, and emphasize the importance of ensuring that inflation expectations remain anchored. With elevated policy uncertainty and risks to both sides of the Fed’s dual mandate potentially pulling monetary policy in opposite directions, the FOMC likely prefers staying on hold until it gains further clarity on the economic outlook.

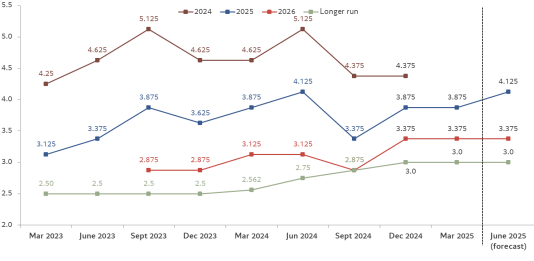

We expect the updated dot plot to show some hawkish adjustments, with the 2025 median rate projection showing one rate cut to 4.125%, down from two cuts in the March projections. Risk is likely tilted towards the dot still showing two cuts. We suspect participants’ tariff assumptions have risen since March, and when combined with still resilient economic data, this could lead to higher interest rate projections. For 2026, we expect the dot plot to show three rate cuts, maintaining the same rate projection of 3.375% as previously indicated. We don’t expect major changes to the longer-run dot (3.0%), but there is a risk of a modest upward adjustment. The Summary of Economic Projections is likely to show higher inflation and lower growth in 2025, but no recession or stagflation in the forecasts.

So far there is limited evidence of broad tariff-induced price pressures in goods prices. However, it may still be too early for the Fed to fully assess the impact of tariffs. Pre-tariff inventory accumulation may have temporarily delayed inflationary effects, and businesses may be finding alternative ways to minimize cost pass-throughs. We expect economic growth to slow noticeably in the second half of the year and continue to forecast that the Fed will cut rates twice in 2025, starting in October.