Key points:

Increased social restrictions as Covid-19 cases surge weighing on growth in near-term, especially in Europe, but progress on vaccinations provides grounds for optimism further ahead.

Solid fourth-quarter GDP growth means China is the first major economy to reach its pre-pandemic trend.

Accommodative monetary policy set to continue for the foreseeable future.

Inflation picking up but unlikely to breach central bank targets.

Economic growth

With recent daily vaccinations approaching 1 million in the United States, we reaffirm our outlook for US GDP growth above 5% in 2021. Additional fiscal stimulus could potentially increase this further. Vanguard foresees fourthquarter 2020 growth in the mid to high single digits, with high-frequency data supporting our view that the number could come in at the higher end.

In the euro area, a surge in Covid-19 cases and the resulting restrictions on economic activity have led us to temper our GDP growth forecast to around 4.5% in 2021 from our previous 5% forecast. Germany is likely to experience the strongest hit to near-term growth owing to its tighter national lockdown measures. Nonetheless, we see economic activity accelerating at a faster pace in the second half of the year than we previously anticipated as the roll-out of vaccines should enable current restrictions to be gradually lifted. Our view that the euro area economy will reach its prepandemic level of growth towards the end of the year is also unchanged.

We have also cut our forecast for 2021 GDP growth in the United Kingdom to around 5% from around 7% last month. We expect the impact of slower growth to be most keenly felt in the first quarter, with a slide back into recession likely owing to the tightened restrictions on activity and the large portion of the UK economy dedicated to vulnerable face-to-face sectors such as leisure, hospitality and tourism. As the vaccination programme here too gathers momentum, we expect the pressure on the healthcare system to gradually ease. This should pave the way for a material easing of restrictions from the spring, which will enable a recovery in output. That said, we expect Brexit to exert a greater negative effect on GDP in the United Kingdom than in the euro area.

The economy in China grew by 2.3% in 2020, according to China’s National Bureau of Statistics, the only full-year growth that any major economy is likely to register for the year. China, whose fourth-quarter GDP growth came in at 6.5% compared with the year-earlier quarter, also becomes the first major economy to reach its pre-pandemic trend. A closer look at quarter-on-quarter numbers, however, confirms our view of a slowing in momentum, with quarterly GDP growth having fallen to 2.6% in the fourth quarter from 3.0% in the third.

Vanguard maintains its forecast for China’s economy to grow by around 9% in 2021 thanks to continued strong developed-market demand for its export goods in the first half, particularly with additional fiscal stimulus likely in the United States, and as China’s domestic service sectors continue to recover.

Vanguard foresees 2021 economic growth of around 6% for emerging markets as the effects of the pandemic and the vaccine rollout—sure to lag behind that of developed makrets—play out. Emerging Asia, with its more effective pandemic management, should lead with growth of around 8%. We expect Central Europe and the Middle East to make the next-best progress, with Latin America, which has taken a harder hit from the pandemic, registering growth of only around 4%.

Monetary policy

Vanguard’s outlook for US monetary policy remains dovish even amid discussions around additional fiscal stimulus to counter the effects of the Covid-19 pandemic. Policymakers at the US Federal Reserve voted on 16 December to leave the target range for its federal funds rate unchanged at 0%–0.25%. It also kept its bondbuying programme unchanged. The Fed said its accommodative stance would continue “until substantial further progress has been made toward the Committee’s maximum employment and price stability goals”. Tapering of such purchases is a long way off, the Fed chairman said, and when it eventually does occur it would come with plenty of advance notice.

The European Central Bank (ECB) kept its main deposit rate unchanged at minus 0.50% at its policy meeting on 21 January. At its previous meeting, as Vanguard expected, the ECB expanded its Pandemic Emergency Purchase Programme (PEPP) by €500 billion to a total of €1.85 trillion and extended the PEPP’s window of asset purchases until at least the end of March 2022. Additionally, the ECB extended by 12 months, until June 2022, the period in which favourable terms will apply under targeted longer-term refinancing operations. Vanguard believes the measures underline the ECB’s commitment to support economic recovery well beyond the end of the Covid-19 health emergency. We expect the ECB to keep monetary conditions highly accommodative, with the deposit rate below zero for at least the next 12 months and with acceleration possible in the pace of asset purchases.

The Bank of England (BoE) maintained its bank rate at 0.1% in December and also left its asset-purchase programme unchanged. Given the worsening outlooks for short-term growth and inflation, we believe the likelihood has increased that the central bank will accelerate the pace of purchases in its quantitative easing programme and that it will leave the programme in place until at least the end of 2021. We don’t expect the central bank to implement a negative-rate policy as such a move would bring operational challenges that banks may not be in position to take on, and we believe the BoE has more potent tools available should conditions warrant further support.

Inflation

The consumer price index in the United States rose 0.4% in December compared with November on a seasonally adjusted basis, having risen 0.2% in November. Compared with a year earlier, the CPI rose by 1.4% compared with a year earlier. Core CPI, which excludes volatile food and energy prices, rose by 1.6%. We expect some volatility in the near-to-medium-term as economic activity resumes and price comparisons with weak prior-year numbers temporarily push inflation above the Federal Reserve’s 2% target. But we don’t expect these cyclical effects to result in a sustained inflationary trend given structural forces including technology. We expect inflation will trend lower in the second half of the year, bringing our outlook for full-year inflation to a range of 1.6% to 1.8%.

In the euro area, inflation declined for a fifth straight month in December, coming in at –0.3% on an annual basis. We expect both core and headline consumer price inflation to rise in the months ahead as the effects of sharply lower energy prices and short-term tax cuts unwind, and as the gap between output and potential output narrows. We nonetheless expect inflation to remain well below the ECB’s 2% target throughout 2021 due to the weak bargaining power of labour and subdued inflation expectations. Even in our upside scenario, we do not expect inflation to surge sustainably above 2%.

Headline inflation in the United Kingdom rose to 0.6% in December compared with a year earlier, up from 0.3% in November. The rate of consumer price inflation slowed materially in 2020, driven by lower energy prices, a valueadded-tax cut, and weakening demand relative to supply, but we expect aggregate prices to rise gradually as these factors unwind in 2021. We foresee inflation rising toward the Bank of England’s 2% target in 2021 given monetary and fiscal stimulus and the imposition of non-tariff trade barriers post-Brexit.

Employment

The unemployment rate in the United States remained unchanged at 6.7% in December, while the economy lost jobs for the first time since April 2020. Job losses were most prominent in the leisure and hospitality sectors amid renewed lockdown measures as virus cases surge. Vanguard doesn’t foresee a prolonged period of job losses, however, with a return to job growth perhaps as early as January and average monthly job creation around 250,000 for all of 2021.

Unemployment in the euro area fell to a seasonally adjusted rate of 8.3% in November, down from 8.4% in October and up from 7.4% in November 2019. Government efforts including furlough and wage-support schemes have held unemployment below levels following the 2008 global financial crisis. Our labour market outlook varies from country to country, with Spain and Italy particularly at risk as a relatively large share of their economies is related to sectors most affected by the pandemic.

Similar to the euro area, support packages in the United Kingdom, including furlough schemes, have limited unemployment. Still, the unemployment rate under the official International Labor Organization measure has risen for the last four months. In the quarter ended in October, the unemployment rate rose to 4.9%, up by 1.2 percentage points from a year earlier.

Brexit

The United Kingdom and European Union agreed a deal on 24 December 2020 that guarantees that trade between them will continue free from tariffs and quotas. We continue to watch for developments in the future UK-EU relationship with respect to financial services.

Asset class return outlooks

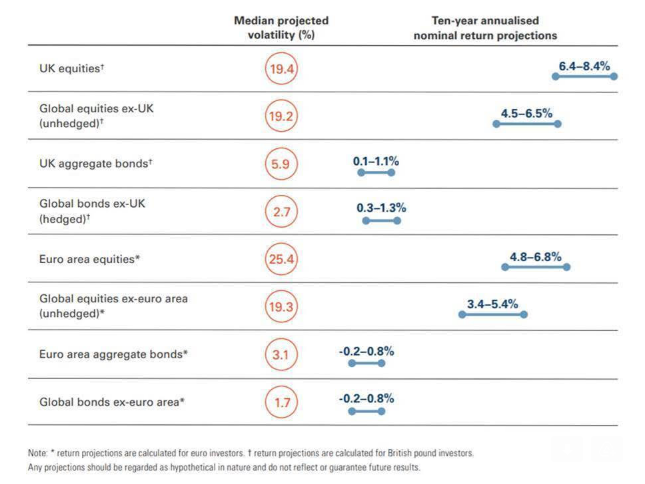

Vanguard’s 10-year annualised outlooks for equity and fixed income returns are unchanged from our last economic and market update in December and are consistent with those presented in the Vanguard Economic and Market Outlook for 2021. The probabilistic return assumptions depend on market conditions at the time of the running of the Vanguard Capital Markets Model® (VCMM) and, as such, can change with each running over time.

ISG updates these numbers quarterly. The projections below are based on the running of the VCMM on 30 September 2020. Projections based on the 31 December 2020 running of the VCMM will be communicated through the February 2021 economic and market update.

Our 10-year annualised nominal return projections are as follows. Please note that the figures are based on a 1-point range around the 50th percentile of the distribution of return outcomes for equities and a 0.5-point range around the 50th percentile for fixed income. Numbers in parentheses reflect median volatility.