Long after the world economy escapes Covid-19, interest rates are likely to remain at or around zero.

Keith Wade |

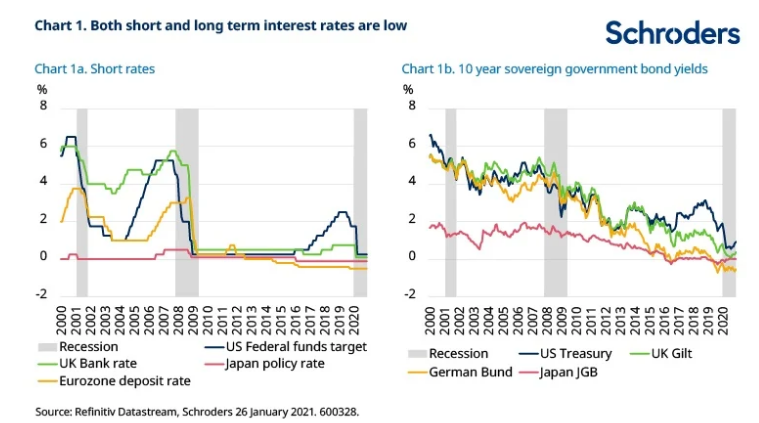

Low interest rates are not new. Short term interest rates have been low since the global financial crisis more than a decade ago. However, the Covid-19 pandemic has led them even lower as central banks have gone “all in” to support economic activity.

Official policy rates are now at unprecedented levels, the lowest since records began in the UK and remain below zero in the eurozone (chart 1a).

What makes the current environment unique though is the low level of government bond yields. Policymakers have stepped up their asset purchase programmes to help drive down long term bond yields to record low levels (chart 1b). It is not just short rates which are at “The Zero” in many markets, so are bond yields.

Surely higher activity means higher rates? Not in our view. We think this low rate environment can persist for some time. Although we expect economic activity to rebound significantly in the second half of 2021, interest rates are unlikely to follow.

Inflation holds the key

One of the key reasons is the outlook for inflation.

As the economy begins to re-open there will be upward pressure on prices and we are already seeing some bottlenecks emerge in the more buoyant goods sector, with shipping costs rising significantly for example.

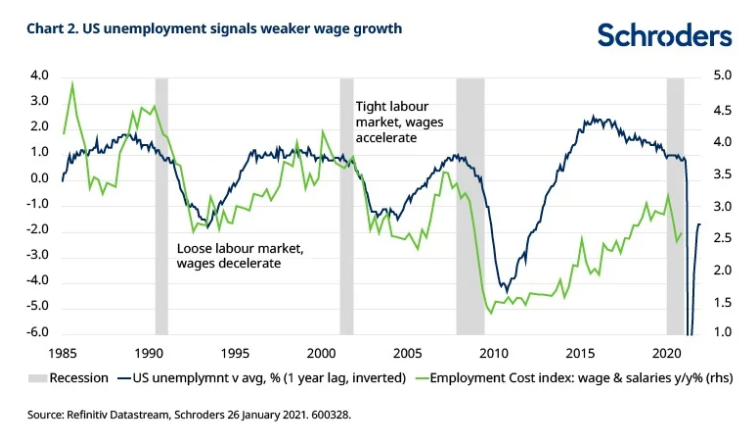

However, this is likely to be a transitory effect as economies will go into the recovery with significant spare capacity, particularly in the labour market. For a transitory increase in prices to turn into a persistent acceleration in inflation we would need to see wages picking up and adding a further round of cost pressure to prices. This seems unlikely with unemployment well above estimates of equilibrium around the world. In the US, the jobless rate is running at 6.7%, well above equilibrium estimates of 4% or lower.

While the relationship between unemployment and wages has weakened somewhat in recent years, the signal is still one of deflationary pressure on wages for a considerable period as workers compete for jobs (chart 2).

In our forecasts the US output gap does not close until the middle of 2022 and later in the UK and eurozone. Consequently, after a brief pick-up once economies re-open later this year, inflationary pressure is likely to ebb until later in 2022.

This is not an outlook which will trouble policymakers as it comes against a backdrop where inflation is already low and central banks recognise that past policies have been too tight and deflationary to hit their inflation targets.

The latter has been most clearly highlighted by the decision by the Federal Reserve to shift its inflation target to one where inflation averages 2% over the cycle. Previously, the aim was to keep inflation at 2%. Now, periods of undershooting should be followed by a spell of overshooting to bring the average back up to target.

As a result, in the current environment, as the economy emerges from recession we would expect the Fed to keep rates low and policy loose for a period to achieve its new target. Such a move would also give the Fed a greater chance of reaching its maximum employment goal where a broader group of families and communities share in the benefits of economic growth.

Of course, we would not rule out a period of higher inflation. There is uncertainty over how the increase in liquidity created during the crisis will be spent and how the long-run effects of Covid might affect equilibrium unemployment. Either could lead to stronger global demand or weaker supply and consequently higher prices. Higher sustained inflation remains a risk, but on balance we believe that the disinflationary trend which was established in the world economy before Covid-19 will reassert itself.

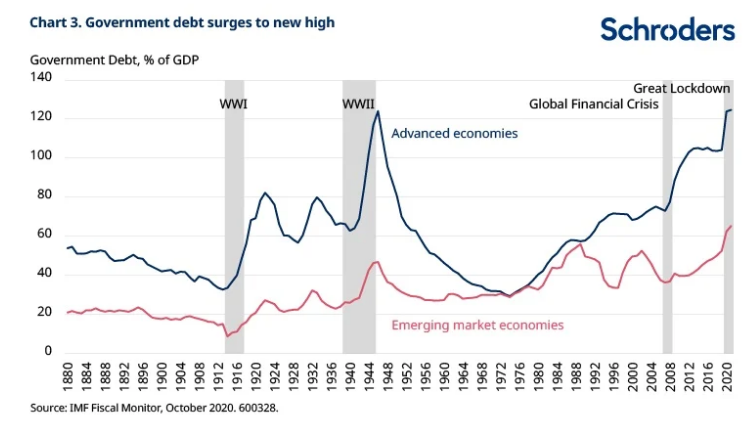

One reason why is simply the level of debt in the world economy. Figures from the IMF show that government debt in the advanced economies has reached levels last seen after the Second World War (chart 3).

High government debt levels will reinforce low rates

While some see high debt as a precursor to higher inflation, suspecting that the authorities will try to and succeed in devaluing their liabilities through inflation, this is not what we’ve seen in Japan.

High debt has been a constraint on growth in Japan as it limits the government's ability to use loose fiscal policy to boost growth. Meanwhile, high levels of debt in the private sector have limited the efficacy of monetary policy by reducing the willingness to take on more debt. Both monetary and fiscal policy are tapped out.

There are signs that others are heading in the same direction. The European Central Bank has argued for some time that it has reached the limits of monetary policy. Policy rates are below zero, there is significant support to the banking sector through targeted refinancing and the central bank is making large scale asset purchases.

In the US and UK interest rates are still positive, but monetary policy has been less effective in the real economy since the financial crisis.

We do see significant differences between Japan and other economies which means that they need not follow along the same deflationary path. For example, there is still room for manoeuvre on fiscal policy in the US, UK and eurozone (fiscal space) to stimulate growth as evidenced recently by President Biden’s American recovery act.

However, looking further ahead, with debt heading above 100% of GDP in the US and UK and both countries facing significant healthcare liabilities, fiscal space will become more limited.

In this environment, the pressure on central banks to keep rates low will remain strong. Not just to maintain overall policy stimulus, but to ensure that high debt levels remain sustainable. In this respect the Fed will become more like its Japanese counterpart where low interest rates are important to ensure government debt remains on a sustainable track.

Please see Are US Treasuries turning Japanese? for more on how monetary policy can become subservient to fiscal needs. The need to boost inflation and facilitate high budget deficits and debt mean central banks will keep policy loose as the world economy recovers. We are in unprecedented times, but the likelihood is that low interest rates will persist long after the world economy has shaken off the pandemic.

For financial markets, such an outlook will intensify the search for yield and no doubt create volatility and bubbles as investors chase returns in “the zero” environment.