All the Excitement of a Commodities Supercycle

A combination of factors is feeding through to strong performance of the Materials sector. Precious metals, in particular, have propelled the sector given their various applications and low stockpiles. Looking ahead, there are important themes that could propel the overall sector, including reflation, demand from China and sensitivity to economic growth.

Investors seeing the supercycle

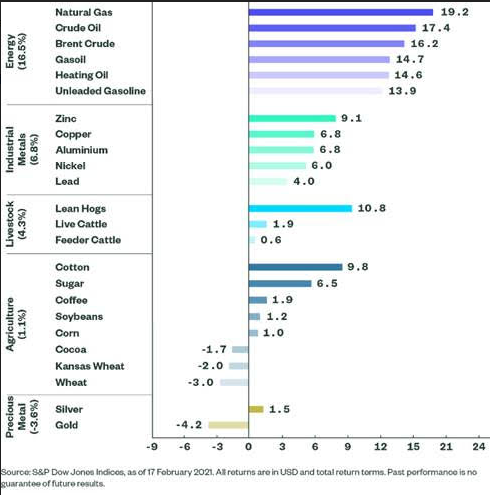

We have seen significant investor attention on reflation as one consequence of the economic reopening story. Among the headlines is the commodity supercycle and its implications for equities. Figure 1 shows how far a wide range of commodity prices have risen month to date.

The largest price moves have come from natural gas and crude oil. And while these moves are impressive, some of the drivers of this phenomenon (primarily the disruption to production caused by the deep freeze in Texas and surrounding US states) are likely transitory.

Meanwhile, the driving forces behind the rise in industrial metals may have more longevity. Interestingly, acceleration of US producer prices in January and a strong ISM manufacturing prices index have indicated that suppliers have pricing power for a range of intermediate materials prices like metals, chemicals and plastics.

In light of the above dynamics, one sector in particular should benefit: Materials.

What’s driving metals prices?

The fundamental reasons for this surge lie in the strength of demand, driven primarily by China. Moreover, moves have become increasingly synchronous on a global level as heavy industries start to recover, and restrained supply due to production and supply chain disruptions courtesy of the COVID pandemic has also bolstered the price.

Copper is particularly interesting. It is one of the most used industrial metals, with China accounting for nearly half of global copper demand. Prices of the metal have risen more than 80% from lows last year. Estimates suggest the price could rise further, based on:

While eventually price hikes are likely to drive a supply response, the usual multi-year lag-time for project commissioning means that significant increases in production will not happen for several years.

Materials plays into many of today’s market themes

Let’s look at MSCI World Materials, which has already shown strong outperformance compared with global equities, having bounced hard during the market recovery since late March 2020, and then in the cyclically orientated markets since the vaccine announcements of early November 2020. Among the industries in Materials, metals and mining (35% by market cap of MSCI World Materials) has seen the highest returns, with total returns of 118% since the March 2020 lows. Following in that industry’s wake, but still showing overall outperformance of the broad index, are the chemicals (51%), containers and packaging 6%) and construction materials (5%) industries.

This strength could continue, as recent results show that not only are mining companies proving adept at passing on metal price rises, but current conditions have enabled them to make positive dividend announcements.

Other important themes driving the Materials sector: