Vaccine Progress Driving Shift in Sentiment

Since the first week of November 2020 – when the first major positive vaccine announcement occurred – global equity markets have experienced a significant shift in sentiment. Over the last five months, market participants have been forced to adjust both earnings and inflation expectations higher as newly vaccinated consumers and producers emerge from the shadows of a global lockdown and return to the real economy.

Markets have clearly been shaken by fears over escalating US inflation. While the Federal Reserve (Fed) continues to point to higher inflation being transitory and largely driven higher by the base effects of having particularly weak price pressures during the early part of the pandemic, markets feel a more radical shift is underway.

Indeed, the PriceStats® indicator of price pressures, which is used by State Street Global Markets, points to more than just base effects at play with US CPI projected to rise to around 4% by the summer. The bigger question is the speed at which it falls back to more acceptable levels after that. Worryingly, for the Fed there are hints that this may be a slower-than-expected process. Warren Buffet, at the shareholders meeting for Berkshire Hathaway , indicated that prices were rising and that those price rises were sticking.

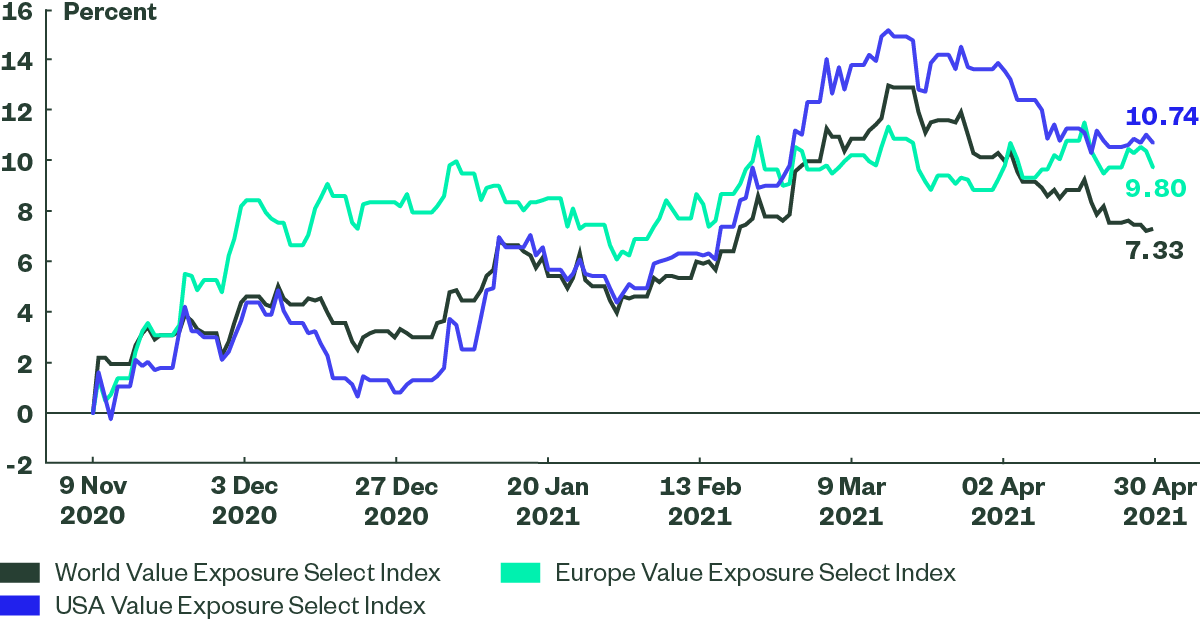

This environment of higher earnings and inflation expectations has provided tailwinds for SPDR ETFs tracking the MSCI Value Exposure Select indices (see Figure 1) across all regions, in the five months since the initial vaccine announcements took place. This trend accelerated in Q1 and peaked in late March, which delivered strong performance for Value stocks.

Figure 1: Excess Performance of Value Exposure Select (Since Vaccine Announcement)

Source: Bloomberg Finance L.P., as of 30 April 2021. Excess performance is measured versus the benchmark MSCI World, MSCI Europe and MSCI USA Indexes. Past performance is not a guarantee of future results.

Value Exposure Select indices take a sector-neutral approach, meaning most of the relative outperformance compared to the market benchmark comes from selecting cheap stocks, which benefit from the reflation trade. As such, the 7.33% of outperformance in the MSCI Value Exposure Select Index (compared to the benchmark MSCI World Index) was distributed across a variety of sectors. The selection effect accounted for an estimated outperformance of 2.51% in Technology, 1.02% in Consumer Staples and 0.93% each in Materials, Industrials and Consumer Discretionary stocks2.

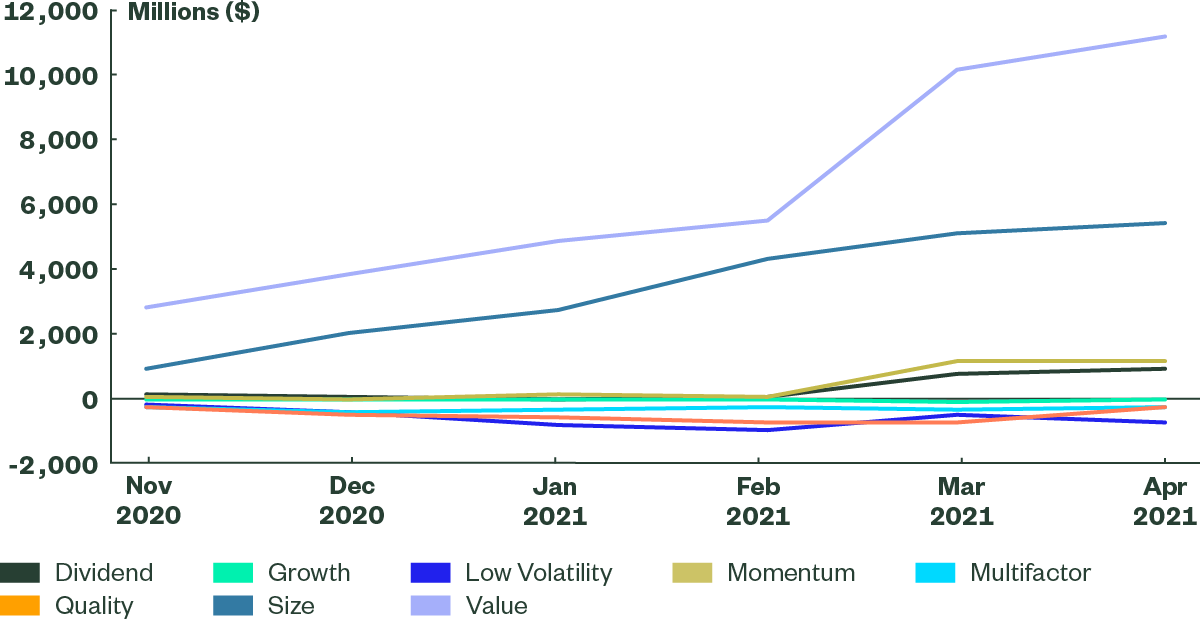

European ETF investors have put a significant amount of money to work into Value-focused smart beta ETFs since November of last year (see Figure 2). Investors who feel they have ‘missed the trade’ may view the small pullback in April as an opportunity to put money to work in Value stocks in May, as the reflation trade plays out approaching the summer months of 2021.

Figure 2: Flows into European-listed Smart Beta ETFs (Since Vaccine Announcement)

Source: Bloomberg Finance L.P., as of 30 April 2021. Flows are as of the date indicated and should not be relied upon thereafter.