By Nadia Gharbi & Frederik Ducrozet, Pictet Wealth Management.

ECB President Christine Lagarde did her best to convey a message of stability and continuity, but our impression is that a lot is going on behind the scenes as the hawks are pushing harder for a change in coming months. Given that the more difficult decisions were postponed until after the summer, the September meeting is shaping up to be an interesting one.

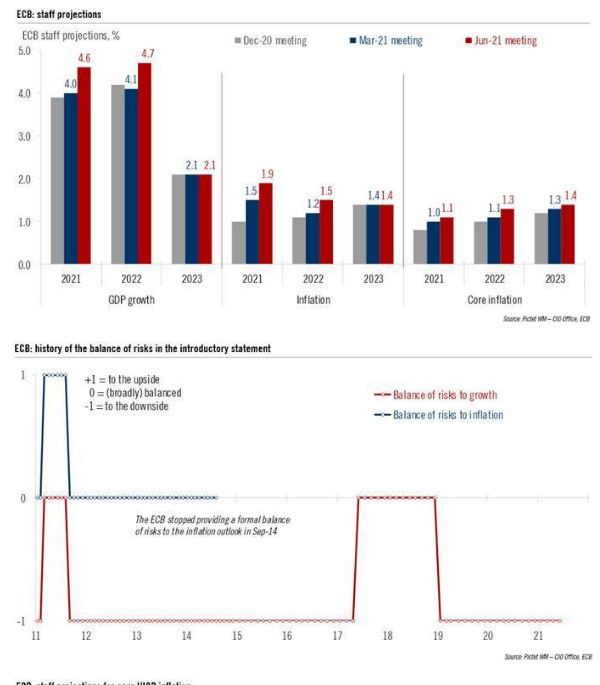

The main news today was that “the Governing Council expects net purchases under the PEPP over the coming quarter to continue to be conducted at a significantly higher pace than during the first months of the year”. Meanwhile Lagarde carefully avoided any discussion about a tapering of asset purchases which she described as “premature”. The ECB decided to keep a “steady hand” despite a fairly significant upgrade to the macroeconomic outlook. In other words, while today’s decision was in line with market expectations, it was dovish relative to the ECB’s assessment of economic conditions.

Indeed, several changes to the ECB statement point to a more optimistic outlook:

\

To be sure, those changes are backed by the improvement in the data as well as the hope for a more active fiscal policy stance. However, they can also be seen as concessions to the hawks, paving the way for a reduction in emergency support in September. While Lagarde said that there was the Governing Council unanimously agreed on the June statement, she then added that there had been a debate about the monetary stance leading to “some diverging views here and there”, including about the pace of PEPP purchases... which was the most important part of the statement.

In all, we expect the ECB to reduce the pace of PEPP purchases by removing the reference to “significantly higher” purchases at the 9 September meeting. One possible scenario would see PEPP purchases around €75bn per month on average in Q3 (accounting for “market conditions and seasonal factors”), slowing to €60bn in Q4, before a gradual taper is implemented in H1 2022. This scenario would leave some €50bn unused in the €1850bn envelope.

More importantly, the Governing Council should start discussing the tapering of the PEPP at the same time they comment on the outcome of their strategy review. We continue to expect the APP to be increased in 2022, from €20bn to €30bn, although other changes could be contemplated adding flexibility to APP purchases, but also reviewing its open-ended nature.

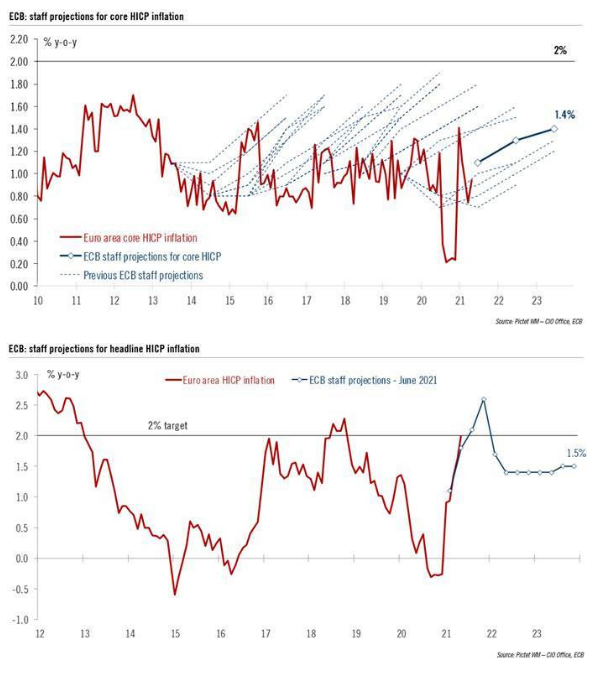

A lot can happen by September, but recent macro and market developments have been rather encouraging, including the bond market reaction to today’s US CPI print suggesting that investors continue to give the Fed the benefit of the doubt. The ECB needs more than that though – they need to remove any doubt over their commitment to bringing back inflation to their (symmetric) 2% target. There’s a long way to go.