Thomas Leys, Investment Manager, Aberdeen Standard investments

With the rapid need to decarbonise and limit the potential devastation of global warming becoming top-of-agenda for governments, companies and investors, demand for ‘net zero portfolios’ is soaring, and the knee-jerk reaction by investors is often to ditch the polluting high emitters in favour of cleaner, greener alternatives. But this could be the wrong approach.

Reducing a portfolio’s emissions by cutting out high emitters looks good, but it fails to achieve the essential real world emissions reductions required to put the world on the path to ‘Net Zero by 2050’. It also cuts off the supply of capital to the areas that need it most: the polluters who want to decarbonise. So forward-looking investors, who want to progress the transition to net zero, should instead consider how to identify the leading decarbonisers from the sectors with the highest emissions.

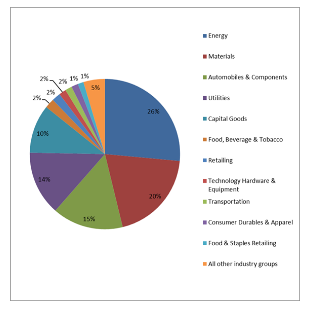

Share of total CO2 emissions (Scope 1+2+3) by sector * (%)

When looking at the emissions distribution of any broad index of either equities or corporate bonds, the same five sectors routinely dominate: energy, materials, automobiles, utilities and capital goods. Globally, these sectors account for more than three quarters of emissions but only a fifth of market capitalisation. The concentration of emissions becomes even starker when looking at the work of the global investor engagement group, Climate Action 100+. The 167 companies it targets account for more than 80% of corporate industrial greenhouse gas emissions. So, avoiding just a few companies can lead to instant, large reductions in portfolio emissions for investors.

However, without capital, how will these companies make progress? How will utilities switch from fossil fuel to renewable energy generation? How will auto manufacturers convert production from petrol to electric vehicles? How will industrial companies invest in the electrification of their processes? The green future requires massive investment and by picking the companies in these sectors that have ambitious and credible plans to decarbonise, investors should be willing accept high emissions now if they believe a company is on a downward emissions trajectory.

Concrete plans

There are many examples of high emitters, who have robust plans to improve – take global building materials giant, LaFarge LafargeHolcim . Not only does cement manufacturing require considerable heat, usually generated by fossil fuels, the chemical process itself (calcination) releases carbon dioxide gas. This helps explain why the company emitted over 148,000,000 tonnes of CO2 (scope 1, 2 and 3) in 2019.

This compares to the median company emissions of 241,000 tonnes for the MSCI All Countries World Index and puts LaFarge LafargeHolcim in the 98th percentile of emitters in the index. A simplistic, low carbon strategy would avoid this company, but LaFarge LafargeHolcim has some of the most aggressive decarbonisation plans in the sector. These begin with cement production with the lowest carbon intensity among its peers and then 2030 targets to reduce scope 1 and scope 2 emissions per tonne of cement by 17.5% and 65% respectively (from a 2018 base).

The group’s investments back these targets up: it is due to open the first net zero cement production facility, and over half of research and development spend is allocated to greener alternatives. Carbon-conscious investors should be supportive of these plans, despite the high emissions today.

Energias de Portugal ( EDP ) is another good example. Until recently, owing to legacy coal assets, it had one the highest carbon intensities in the European utilities space. However, it is successfully reinventing itself as a low carbon power company. By closing coal generation plants and investing heavily in renewables, it plans to reduce emissions from its own operations by 90% from 2015 to 2030. Furthermore, EDP ’s targets keep getting more ambitious: in February the company brought its coal phase-out deadline forward by five years to 2025 and now only spends 2% of its capital expenditure on the fossil fuel (purely for maintenance). The emissions trajectory for EDP looks impressive.

Not all targets are equal

Unfortunately, investors cannot simply pick the companies with the biggest decarbonisation targets. According to the International Energy Agency, around 40% of companies with net zero pledges have yet to set out any detail of how they plan to achieve them. A “net zero by 2050” target is easy enough to set, but the devil, as usual, is in the detail. Analysis by the Transition Pathway Initiative looking at the commitments of companies in high emitting sectors shows that very few have ambitious enough decarbonisation targets. Only by understanding the credibility of targets, and the plans to achieve them, will investors be able to identify high emitting names that are on the right path.

Share of total CO2 emissions (Scope 1+2+3) by sector * (%)

To get investment portfolios to net zero investors need to go beyond looking at a company’s emissions today. Emissions trajectories are what count. Stripping a portfolio of its highest emitters will lead to some quick-wins, but this denies certain sectors the funding they need and fails to achieve real world emissions reductions. Analysing decarbonisation plans to find the credible transition companies enables investors to finance essential climate change mitigation efforts. At the same time, investors gain exposure to companies that are leading their sectors when it comes to the transition to a net zero economy.