Richard Colwell, Head of UK Equities Columbia Threadneedle Investments.

In 2021, investing in UK equities began to feel a little less lonely. The FTSE 100 index rose by more than 10%1 for the year by early December and UK companies resumed dividend payments after the pandemic-induced economic freeze in early 2020 when all hope seemed extinguished.

Indeed, since the market’s March 2020 lows the FTSE 100 has returned more than 40%. But that is nothing compared to the runaway train that is the US S&P 500 Index, which has more than doubled in that time.2

In fact, despite an excellent year, the UK remains relatively unloved. Investors pulled £8 billion from UK equity funds in the first 10 months of 2021, from a total of £235 billion.3 This means there have been outflows for five out of six years since the 2016 Brexit referendum. One hedge fund called the UK the “Jurassic Park of stock exchanges” with investors not interested in growth and only hanging around for the robust dividend payments.4

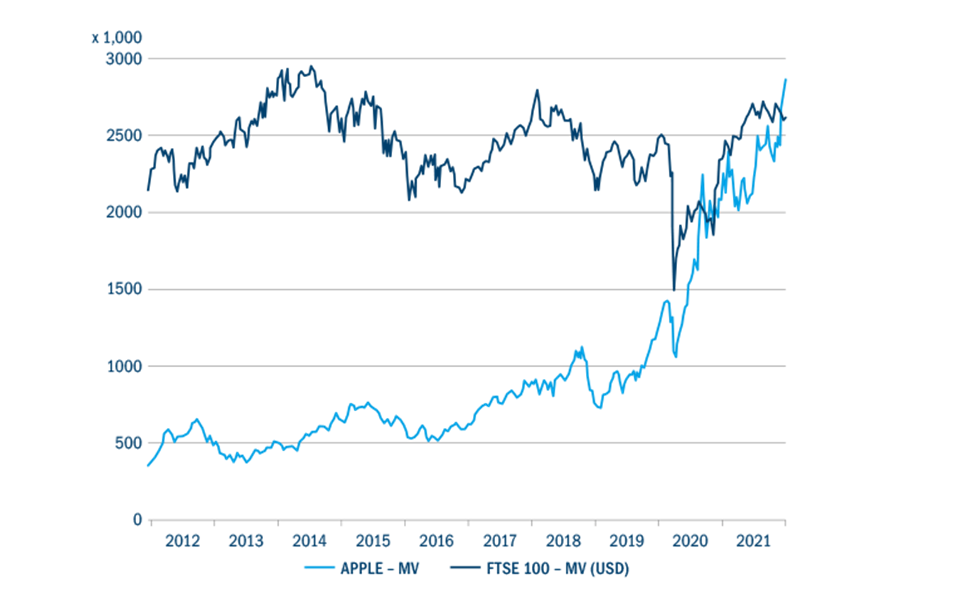

The absence of tech shares goes some way to explain this, as the US tech giants have totally dominated global markets since 2018 (Figure 1). But strip out the big six tech stocks – Alphabet , Apple , Amazon , Facebook , Netflix and Microsoft – and S&P returns suddenly look a lot like everywhere else, while the Nasdaq without its five tech giants is deeply negative year-to-date.5

Figure 1: Apple ’s market cap outstrips the entire FTSE 100

Source: Refinitive Datastream, December 2021

Source: Refinitive Datastream, December 2021Beware the bezzle

This has also been a time of what economist JK Galbraith termed the “bezzle” in the 1920s: an as-yet-unrevealed inventory of nasty shocks built up in the good times, which only reveal themselves when tougher times arrive. A whole generation is learning to trade crypto currencies and NFTs (non-fungible tokens) rather than stocks, and when they are dipping their toes into markets it’s via “meme stocks” popular among retail investors shared on social media platforms.

When tougher times arrive, this crowded capital could be exposed to bezzle assets that quickly plummet. Central bank backstops have conditioned investors to buy on the dip, but in fact have made the whole system more fragile. A shock such as the Omicron Covid-19 variant partially circumventing vaccines could be such a catalyst to send equities into a ferocious nosedive.

Back in business

The UK, meanwhile, is quietly going about its business. The volatility of the post-Brexit deal seems to have settled, JP Morgan recently turned bullish on UK equities for the first time since the referendum,6 and in the summer Bloomberg was hailing “the City’s IPO renaissance” as new listings during the first six months of 2021 rose by 467% with a valuation of $20 billion. All the while the UK retains its valuation arbitrage and remains cheap: M&A is at record levels, helped by the GBP which is at 35-year lows versus the dollar, and there have been 12 transactions above $500 million in the UK market in 2021 so far – the most since 2007 – with the average transaction value now at $2.6 billion, almost an alltime high. This has seen $10 billion in premia paid by the private equity community to public equity to close the valuation arbitrage – a record level – with deals such as that for WM Morrison Supermarkets supermarket.7

According to JP Morgan’s chief markets strategist, the majority of equity investors today don’t buy or sell shares based on stock specific fundamentals.8 But we do. The UK market is much more nuanced than people suppose – it’s a stock picker’s market – and we have the team for this. We know there are good companies out there because we engage with them. This is crucial to our process and is something we take seriously.

This rising number of passive investors, and trading-orientated managers, means we have a meaningful say in the way companies are run. So we actively engage to probe the reasons behind performance, and we have a say in stewardship and governance. We’re not afraid to vote against issues, but are confident in our process and happy to explain our rationale.

Looking ahead

While the UK has rallied a long way, it remains a reliable alternative to more highly valued, crowded markets and has further to go. The market is more nuanced than simply buying banks and commodities. Our fundamental research process uncovers hidden gems, with an eye for unloved stocks that have disappointed but remain good businesses. Meanwhile, our active engagement probes what is behind performance. We will be pragmatic and patient as the recovering UK delivers on its promise.

1 Bloomberg, December 2021.2 Bloomberg, December 2021.

3 Morningstar data, November 2021.

4 Daily Telegraph, London’s stock market still punched above its weight, 3 December 2021.

5 S&P Global Market Intelligence, 6 December 2021.

6 Daily Telegraph, London’s stock market still punched above its weight, 3 December 2021.

7 JP Morgan Conference, November 2021.

8 https://www.cnbc.com/2017/06/13/death-of-the-human-investor-just-10-percent-of-trading-is-regular-stock-picking-jpmorgan-estimates.html