Luca Paolini, Chief Strategist and Sabrina Khanniche, Senior Economist, Pictet Asset Management

Russia's invasion of Ukraine has unnerved investors. But the economic fallout from the conflict appears manageable.

Russia’s invasion of Ukraine has unsettled financial markets, causing a steep sell-off in equities and a rally in gold and oil.

The military assault could indeed have serious consequences for the global economy, but the range of possible outcomes is wide. While Russia has stated it does not plan to occupy the country, it is not clear whether it will settle for a limited offensive or is preparing a longer campaign that would lead to a wave of severe economic sanctions from the West.

Faced with these scenarios, investors could be forgiven for wanting to shore up their defences. Yet we would caution against taking drastic measures. History suggests that wars do not always lead to sustained declines in riskier assets. Much depends on how long the conflict lasts.

Take the Iraq war of 2003, for instance. While stock markets were weak in the lead up to the US invasion of the country, they began to recover within 10 days of the start of the military campaign.

At the same time, it is important to put Russia’s economic influence into context. It accounts for just 1.8 per cent of world output – a level that is lower than Italy’s. And while it has a population of 143 million, double that of France, it not a major export market for most countries.

All of which means that if a protracted conflict can be avoided, the economic fallout should remain manageable, allowing the world to build on its recovery from the pandemic and the bull market in equities to continue.

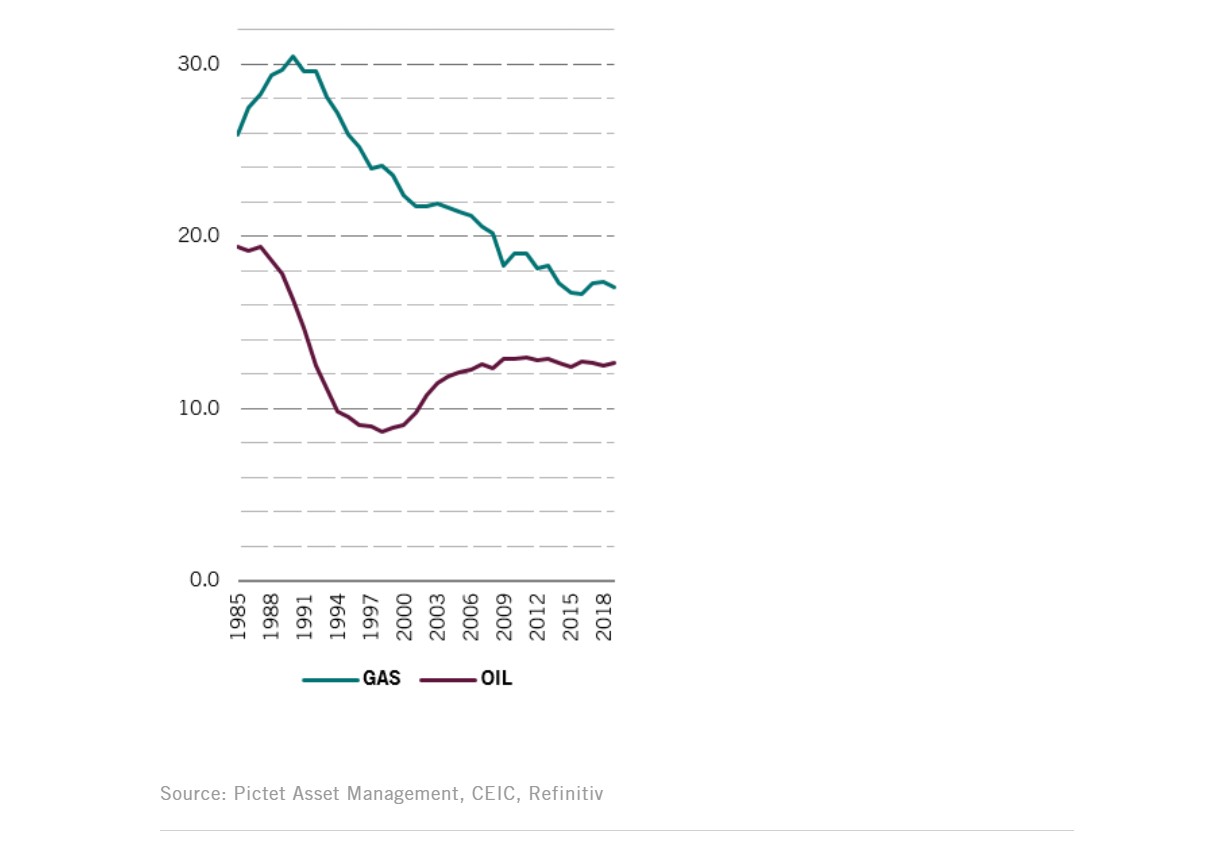

Fig. 1 - Oil and gas

Russia’s share of global oil & gas production (%)

Our analysis shows that economic growth remains relatively strong – we see global GDP rising by 4.4 per cent this year (0.2 percentage points higher than consensus forecasts). Crucially, savings levels – among both households and corporations – are high, while monetary and fiscal policies remain supportive.

Inflation is a much greater risk, particularly given that the Ukraine crisis has caused a surge in oil prices – which were already high in the first place. Even before the Russian invasion we had raised our forecast for global inflation to 5.1 per cent this year (from 4.1 per cent a month ago).

Russia is responsible for 13 per cent of the world’s oil production and 17 per cent of its gas. It is also a major producer of metals, particularly palladium, platinum and gold.

Taking Russian supply out of the equation could usher in a sustained rise in the price of oil and other commodities, adding to global inflationary pressures. Higher prices would reduce consumer purchasing power and possibly eat into corporate profit margins.

However, here too we see mitigating factors. The base effects on inflation are about to turn more favourable and Covid-related transitory factors (such as supply chain disruptions) are abating. Even with oil prices at around USD100, we would expect headline inflation to start declining in the coming months.

Another silver lining for the economy could be that central banks – having in recent weeks ramped up their hawkish rhetoric – see fit to scale back their monetary tightening plans.

Defensive measures

Still, there are some defensive measures investors might want to consider, particularly given Russia’s position as major oil, gas and metals exporter to several major economies.

From this vantage point, the euro zone also stands out as being at risk. Our analysis shows that 21 per cent of the euro zone’s energy imports come from Russia. Combine that with the more hawkish tone from the European Central Bank in recent weeks, and we think a more cautious stance on European equities could be warranted.

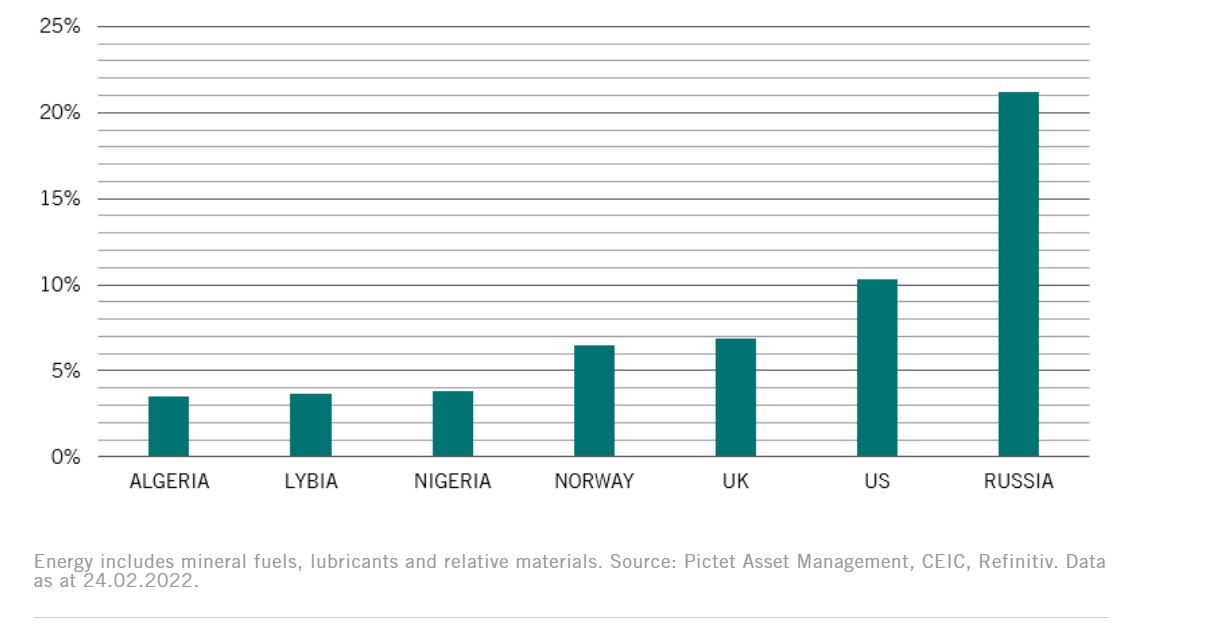

Fig. 2 - Euro zone powered by Russian oil and gas

Euro zone's energy imports by main suppliers (% of total)

However, it is important to point out that the euro zone’s trade ties are not strong outside energy, which accounts for two-thirds of the value of euro zone’s Russian imports. Europe does have some exposure via its banking sector but that, too, is modest. Even in Austria, whose banks have by far the strongest links to Russia within the euro zone, exposure is equivalent to just 1.7 per cent of GDP, according to our analysis. On the other side of trade, meanwhile, Russia consumes 2.6 per cent of euro zone’s exports.

Of course, there is a fine line between keeping calm and being complacent. The situation is clearly volatile. The conflict – and economic sanctions – could become more serious, which in turn would have more significant consequences for the global economy and markets. Raw materials, gold, Swiss franc and Chinese assets could all serve as potential hedges against such risks.