We expect Emmanuel Macron to win the French presidential election and markets are also priced for a Macron victory. But a surprise Le Pen victory could trigger a political shock in Europe. Here’s our take on Marine Le Pen’s prospects and the potential implications of an unexpected electoral outcome for investors.

By Elliot Hentov, Head of Policy Research at State Street Global Advisors

The first round of voting in the French presidential election is now complete. Since both Emmanuel Macron and Marine Le Pen are likely to outperform their 2017 numbers, the second election round, which will be held on 24 April, is likely to decide the outcome. In 2017, Ms. Le Pen’s vote share topped out at 46% in the second round of polls and declined following the presidential head-to-head debates.

This time around, she has yet to peak and there is one poll showing her at 49.5% – i.e., within the margin of error of victory. Average polls still show a narrow but comfortable 53-47 lead for Mr. Macron and markets are priced for a Macron re-election. But a surprise victory for Ms. Le Pen could have substantial consequences. With that in mind, this piece will assess Ms. Le Pen’s prospects and discuss some of the most notable potential investment implications.

Campaign Dynamics

Both candidates have risen in terms of their approval ratings and popularity, which suggests that the poll differential should be driven by an increased risk of certain voters not turning out for the election. These would mainly be left-wing voters that Mr. Macron did not court much during his presidency and throughout his current campaign. It would not be surprising, therefore, if in coming weeks we were to witness a massive fear campaign by Macron supporters to help drive a turnout of anti-Le Pen votes. Voters may be receptive to such a campaign in light of the ongoing Russia-Ukraine War, especially given Ms. Le Pen’s pro-Putin history.

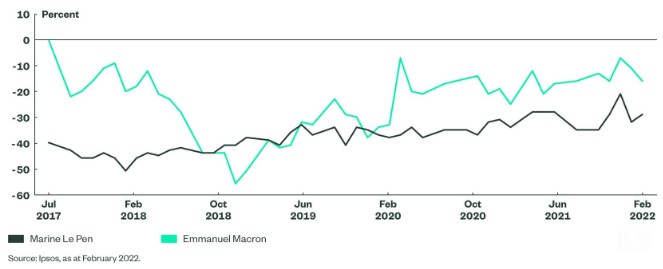

Structurally, France’s two-round system means that “disapproval” ratings historically have had more predictive power. Subtract disapproval from approval to arrive at net favorability – in France’s case, elites tend to be not favored and are hence in negative territory. But Mr. Macron enjoys structurally higher support than his rival, excluding the effect of the gilets jaunes protests. It is worth bearing in mind that no French president with lower net favorables has won the second round before, but one can never say never (Figure 1)!

Figure 1: Net Favorability of Macron vs. Le Pen

Market Implications

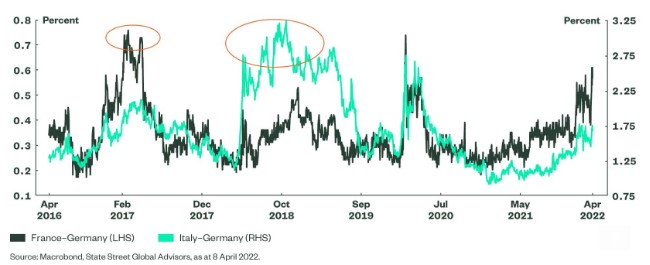

Figure 2 spotlights France’s last election in 2017 and the Italian general election in 2018. Although the recent spread widening was largely driven by the prospect of a tighter monetary policy, it could blow out ahead of the second round of election.

Figure 2: Government Bond Yield Spreads

It is helpful to recall that quantitative easing was in full force when France’s last election was held. Regardless, wider spreads are a certainty although there could be a short reprieve should Macron get re-elected. In the first round, while Mr. Macron won with 27.8% of the vote, ahead of Ms. Le Pen (23.2%), and Jean-Luc Mélenchon was placed third (22%), the results suggest that the run-off on 24 April may be very tight. Since the main opposition managed to gather a higher-than-expected vote share in the context of a lower-than-expected voter participation rate in this round, we might expect a sell-off in French OATs and Italian BTPs and some softness in the EUR.

We do expect Mr. Macron to win and markets are also priced for a Macron victory. At the same time, the European Central Bank (ECB) would be under enormous pressure to respond should a Le Pen surprise materialize. An ECB official recently made the following off-the-record remark when asked if it was their job to narrow spreads: “No, our job is to contain them.”

This means that it would be wise to expect a sharp repricing of bond curves and a big drop in the euro in the event of a Le Pen surprise. In that event, we would expect a larger risk-off event to ripple across global equities.