On the eve of Earth Day 2022, Pauline Grange and Jess Williams Companies analyse the four environmental themes for the next decade.

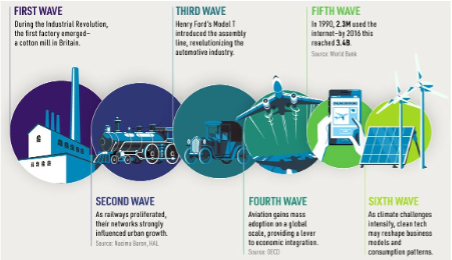

The economist Joseph Schumpeter developed the theory of innovation cycles or waves, using the term “creative destruction” to refer to the process of new technologies surpassing old. Clean technologies, along with digitalisation/AI and robotics, are increasingly being recognised as a key part of the sixth industrial wave (Figure 1).

Figure 1 : Innovation waves and key breakthroughs

Source:https://www.visualcapitalist.com/the-history-of-innovation-cycles/

We believe we are only at the start of this wave with clean or green technologies increasingly being a focus of capital investment, both at the public and private level, over several decades.

The energy transition: a bumpy road but accelerating towards net-zero

The transition away from fossil fuels was never going to be easy and in 2021 we hit the first bump on the road of this journey. Rocketing energy bills have affected most countries as the price of oil, coal and gas has soared over the past year. There have been several factors behind this crisis, but at its core it is a demand versus supply mismatch.

Demand for fossil fuels recovered swiftly as Covid-19 lockdowns were relaxed. Simultaneously, rising renewable energy within the total global energy mix has contributed towards greater variability in energy generation – the sun doesn’t always shine and the wind doesn’t always blow, with the UK for example seeing some of the lowest levels of wind in 70 years in 2021.

This, combined with droughts in Latin America affecting hydropower output in the region, which accounts for 45% of its total electricity generation, led to increased demand for fossil fuels.

But investment into oil and gas has been low in recent years with weak commodity prices and environmental, social and governance (ESG) related concerns limiting capital inflows into the industry. More recently, supply chain challenges have impacted production. Supply simply couldn’t keep up with demand and so prices squeezed higher.

We believe this energy crisis, along with rising global geopolitical tensions, will if anything accelerate investment into renewable energy and the technologies needed to make renewable sources more reliable, such as battery storage and green hydrogen.

However, more careful planning and balancing of the energy grid will be required as renewables start to exceed 30% of global electricity generation.

In addition, economies need to do a better job of winding down demand for fossil fuels. We still consume far too many, with global oil demand forecasted to not peak for another five to 15 years. You can’t start closing the taps when you’re still thirsty.

But energy-related transmissions in transportation, across industries and in heating account for 78% of global emissions.1 If we have any hope of achieving net-zero targets it is vital we transition to clean energy.

Put another way, currently only 17% of our total energy supplies come from clean energy – this must rise to 78% by 2050 if we are to achieve our net- zero aims.2

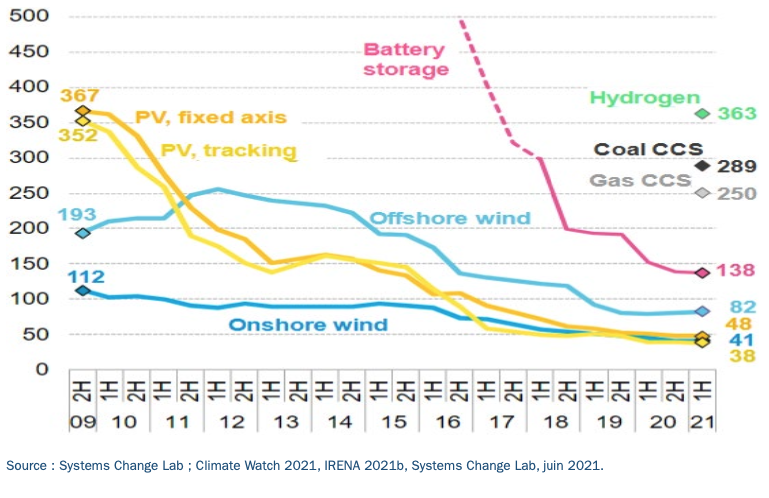

Increasingly, the transition to clean energy also makes economic sense. Renewables are now the cheapest form of new electricity generation across about 90% of the world by energy supply with the recent surge in fossil fuel prices further improving their relative cost competitiveness (Figure 2).

Once you factor in the economic costs of unabated climate change, forecast at more than 3% of GDP being lost every single year by 2030,3 the clean energy transition becomes even more attractive.

And although the large capital investment required is inflationary in the near term, over the long term transitioning to renewables means governments and companies will no longer be exposed to the volatility of commodity pricing. With 80% of people living in countries that are net importers of fossil fuels, this has huge social benefits as renewables provide a cheap source of energy.

Attractive economics, the electrification of economies and increasing government policy and consumer support are a powerful cocktail to accelerate investment into renewable energy. In fact, the IEA (International Energy Agency) forecast that by 2026 global renewable electricity capacity will rise more than 60% from 2020 levels to more than 4,800GW, with renewables set to account for almost 95% of the increase in global power capacity through to 2026 – this is equivalent to the total current global power capacity of fossil fuels and nuclear combined.4

Figure 2 : Levelised cost of energy (LCOE) for selected low-carbon power technologies ($/MWH)

Transitions are not easy, but it doesn’t mean they don’t happen. We have undergone previous energy transitions – in the 1800s the shift away from whale oil was equally inflationary as supply was cut faster than demand fell, but it didn’t stop the transition to a superior energy technology, which at that time was petroleum. We believe the same to be true for green energy.

Protecting biodiversity, protecting economies

Every day, even before we leave our homes, we will have benefitted from biodiversity. Healthy ecosystems help provide the clean air we breathe, the clean water we shower with, the coffee beans we drink, and even contribute to ensuring our flood-free commute to work.

The importance of biodiversity is subtle but wide-ranging. We receive benefits via soil health, pollination, natural resources, carbon storage and much more. Yet human activities have reduced wildlife populations on average by 68% compared to 46 years ago.5

Increasingly, there is a realisation that biodiversity loss is a big problem. Certainly, from an investing standpoint its economic importance cannot be understated: around $44 trillion of economic value generation – more than 50% of global GDP – depends on nature and its services.6 As we destroy biodiversity, we destroy the possibility of us coexisting sustainably with nature.

Investments that align to UN SDG 12, Sustainable Resource Management, look to address some of these issues. Take John Deere , which is a global leader in farming equipment.

The company is at the forefront of innovation around precision agriculture, which is vital to making farming more sustainable. Given its market dominance it can have an outsized impact. Its spraying technology, for example, allows for individual nozzles to be turned on and off to eliminate over application, and avoid waterways. Also, as these chemicals are very carbon intensive to produce, Deere estimates the precision technology can reduce plant herbicide and pesticide usage by 77%, vastly reducing the carbon footprint.

Regulation is also driving the need for targeted application with upcoming EU and UN regulation – such as the former’s “farm to fork” strategy – seeking aggressive pesticide reductions. Precision agriculture technology doesn’t just enable farming customers to be more sustainable in order to comply with new regulations; it also makes economic sense by facilitating more efficient use of inputs and improved yields, particularly important in a world of rising inflation.

The second part of the UN Biodiversity Conference (COP15) will start in April in Kunming, China, where we expect more focus from global leaders on this topic, not least because we are much earlier in the journey to understanding and quantifying the problem, unlike with carbon.

Green mobility

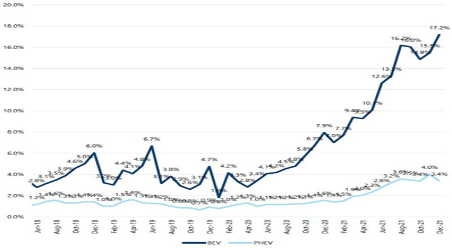

Throughout history, humans have underestimated the pace of technological disruption. It’s tough to envisage a future so different from the one you live today. For example, as a teenager one wouldn’t believe that future teenagers would spend a daily average of 7 hours and 22 minutes on their phones.7 Like the communications industry, the auto industry is ripe for disruption – and at a pace we expect will surprise investors. In fact, we have already seen demand for battery electric vehicles (BEVs) inflect higher in China in 2021 (Figure 3). The trigger for this inflection has been economic rather than environmental, with Chinese consumers citing lower operating costs as the number one reason for purchasing a BEV.

Figure 3 : BEV and PHEV penetration as % of new car sales

Source: Jefferies, CAAM Report, January 2022. BEV= battery electric vehicles. PHEV = plug-in hybrid electric vehicle.

China has benefitted from strong domestic battery supply chains – for example, it is currently responsible for 80% of the world’s BEV battery raw material refining8 – and semiconductor chip production, as well as supportive government policies which have allowed the industry to scale faster than other regions. This has enabled domestic brands like Xpeng to launch a wide range of cheaper electric models. The lower upfront cost combined with low operating costs has made the total cost of ownership of a BEV increasingly attractive for premium mass market consumers.

Interestingly, the number two reason cited for adoption is the overall better driving experience, with many EVs having vastly superior autonomous, safety and digital features. This is particularly important to the younger, digitally savvy consumer – as phones have become smarter, why shouldn’t our cars?

The US has been a clear laggard to- date, with BEVs as a percentage of new car sales remaining stubbornly in the low single digits. But we believe this is set to change with much stronger policy support under the Biden administration in the form of tax credits and subsidies. Part of the president’s infrastructure bill includes large investment aimed at rolling out national charging networks and investing in green energy infrastructure. At the same time, the American consumer loves large cars, which are now coming to market in the form of electric SUVs and pickup trucks.

To achieve net-zero targets we need to add an average of 35 million passenger EVs to the global fleet our global fleet each year between now and 2030.9 To put this in context, we only added an estimated 4.7 million electric cars in 2021. Some of the world’s biggest car markets have already announced the phasing outs of internal combustion engine sales between 2030 and 2040 to support their net-zero targets.10

As the range of EVs coming to market increases and the industry scales, there is no reason other regions won’t follow China’s inflection path. In fact, the cost of EVs is forecast to approach cost parity with combustion engines before 2024, with China expected to be the first to achieve this.

But there are challenges to replacing our global fleet of cars. Firstly, the current manufacturing capacity of batteries is hugely inadequate to meet this surge in demand – 14TWh of battery manufacturing capacity – or 88 times 2020 capacity – is required to reach 100% EVs by 2050.11

Secondly, EVs have much more mineral and material content – almost six times more than a combustion engine. We simply don’t have enough materials in reserves, let alone in production, to meet demand. A combination of battery recycling, more efficient material extraction, green supply chains and lower material content in new generation batteries is vital if we are to solve this.

Finally, a paucity of reliable charging points, particularly in rural locations, means that investment in high powered charging networks, as well as renewables in the energy grid, needs to be accelerated if we have any hope of powering this electric fleet of vehicles.

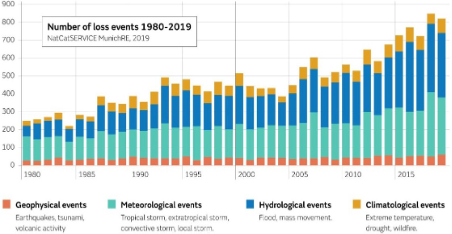

Figure 4: Weather events causing economic loss are now more frequent

Source : MunichRE, 2019.

But these challenges are not insurmountable. And so, as the EV market grows, we believe those companies producing the components necessary to produce and power EVs will enjoy a sustainable runway for future growth.

Future proofing for climate change

Sadly, the climate crisis is now a reality in many parts of the world. We are seeing both increasing severity and frequency of flooding and drought. The volume of extreme weather recorded in 2021 was exceptional by any standard, from the record-breaking heatwaves across the world to the wildfires that raged from Siberia to California. In addition, supply chain disruptions have not just been related to Covid but to weather as well, with severe flooding across Europe, the US and China causing severe disruption to logistics and manufacturing operations (Figure 4).

We are already at around 1.1C warming and swiftly approaching 1.5C.12. Governments are waking up to the fact that cities and populations need to be protected from the inevitable economic and social impacts of climate change. This requires upgrades to infrastructure to better insulate cities from the climate emergency, as well as an acceleration in “green capital investment” to avert worst-case climate change scenarios.

As countries face the prospect of increased flooding, we will need to flood-proof our cities and vital infrastructure. In fact, a recent report published by First Street Foundation shows that nearly a quarter of US critical infrastructure – utilities, airports, ports and more – are at risk from flooding due to climate change.

At the other end of the climate spectrum, the increasing severity of droughts will place increasing pressure on our water systems which, combined with population growth, will mean that increasing parts of the world will face absolute water scarcity. This will require large investments in water infrastructure not only to upgrade our ageing water networks, which globally lose about a third of the world’s water, but also investments in smarter water solutions that help promote the recycling of wastewater.

As heatwaves become more frequent, meanwhile, we will need to invest in bigger cooling systems for both our buildings and food transportation.

This will be particularly vital in densely populated cities which are worst affected by rising temperature as concrete traps and radiates heat, pushing temperatures even higher.

Without this the lives of society’s most vulnerable – the elderly and young – will be at risk. However, heating, ventilation and air conditioning systems also contribute to greenhouse emissions, so we need more sustainable solutions to help keep populations cool.

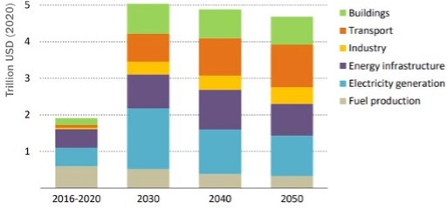

Countries like the US are proposing large infrastructure spending plans which have a focus on “green” investment. To electrify our economies we need to rewire how they work, which will require large-scale investment across not just the power sector – in both renewable energy and the electric grid – but also in green mobility, industry and buildings (Figure 5).

We believe this huge investment in infrastructure and buildings could create a multi-year capital investment super-cycle, the scale of which is being underestimated by many investors.

As such we are invested in those companies that are on the right side of this green capital investment we expect to come to market.

Figure 5 : Average annual energy investment 2016-20, and in the net-zero by 2050 scenario

Source: IEA 2021 world energy outlook report.

By Pauline Grange, Portfolio Manager & Jess Williams Companies , Portfolio Analyst, Responsible Investment Columbia Threadneedle Investments.

1 BNEF, New Energy Outlook, April 2020.2 BNEF, New Energy Outlook, April 2020.

3 Bloomberg, The $36 Trillion Bill for Neglecting Climate and Free Trade, 13 November 2020.

4 IEA, Renewable electricity growth is accelerating faster than ever worldwide, supporting the emergence of the new global energy economy, 1 December 2021.

5 WWF Living Planet Report, 2020.

6 World Economic Forum, 2020.

7 Barclays , China EVs report, February 2022.

8 Barclays , China EVs report, February 2022.

9 BNEF, NEO 2021 report. 10 BNEF, NEO 2021 report.

11 BofA Global Research, IEA, 2021.

12 FT.com, Global warming of up to 2.7C by century’s end forecast as COP26 pledges fall short, 9 November 2021.