Stocks suffered a brutal sell-off in April but there are signs that investor positioning is overly bearish.

Pictet Asset Management Strategy Unit.

Asset allocation: technical indicators suggest calmer times ahead

The investment climate appears to be getting harsher. Global economic growth is slowing, inflation is rising, no resolution appears in sight for Russia’s invasion of Ukraine and new Covid-related lockdowns are sweeping through China, impeding growth.

Faced with these challenges, investors could be forgiven for adopting a defensive stance.

Yet we prefer to remain neutral rather than underweight equities. And that is largely because investor positioning has become excessively bearish, reducing the scope for further market declines in the near term.

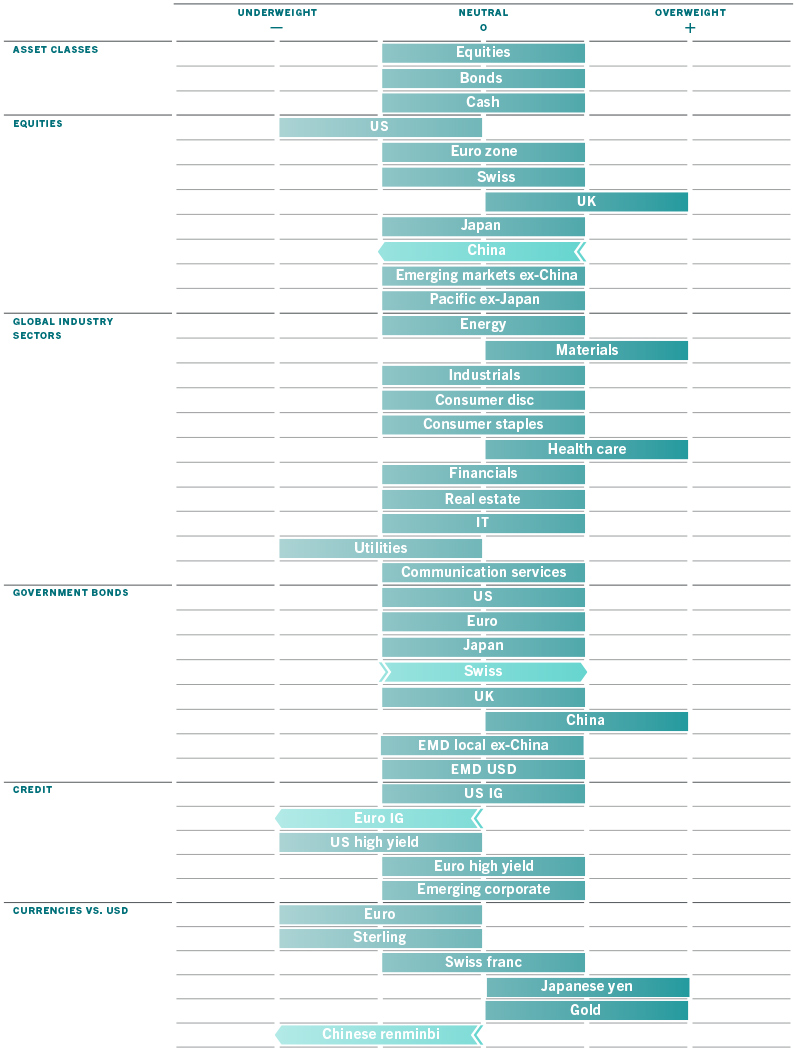

Fig. 1 - Monthly asset allocation grid

May 2022

Source: Pictet Asset Management

Indeed, the picture emerging from our technical indicators shows that both positioning and sentiment among investors is unusually pessimistic, discounting a significant loss of economic momentum in the months ahead. Yet history tells us that shorting equities in a bull market, even during the later phase of the cycle, when sentiment is very depressed is always very dangerous.

That said, we have tweaked our positions to adopt a slightly more cautious stance, but – for now – have decided to keep an overall neutral weighting on both global equities and global bonds.

While government bonds are looking increasingly good value after steep sell offs, we would prefer to wait until US inflation and inflation expectations have peaked before upgrading them.

Our business cycle indicators support our broad asset allocation stance. Although we have, yet again, reduced our economic growth forecast for 2022 to 3.4 per cent - from 3.5 per cent a month ago and 4.8 per cent at the start of the year – our estimate remains above both the long-term trend and the market consensus.

The US economy, in particular, continues to look solid: US real GDP contracted in the first quarter but final demand continues to gather strength thanks to an exceptionally strong labour market and positive trends in investment spending. Our US leading indicator is rising at a stable pace and remains in line with its historical average. In Asia, meanwhile, Japan and some of the region’s emerging economies are seeing improvements in activity and in consumer confidence.

Things look more problematic in the euro zone – not least due to its closer economic and geographic ties to Russia and Ukraine. A technical recession is a real risk, especially in Germany where consumer confidence has fallen to all-time lows.

The Chinese economy is also struggling. Purchasing manager indices are falling below 50, while exports are peaking. Authorities are offering some stimulus, but, so far, not aggressively enough to offset the weakness in the property sector and the consequences of the strict Covid lockdown in some major cities.

Our liquidity indicators show that China is easing policy much more slowly than US is tightening. Yield differentials between US and Chinese government securities suggest that the renminbi could fall to around 7 per dollar over the coming months.

Valuations look particularly concerning for euro zone investment grade bonds; US investment grade bonds appear more attractively priced by comparison.

For equities, valuations are generally looking more attractive, with the 12-month price-to-earnings ratio on MSCI All Country World Index having dropped to 15.5 times – roughly in line with the average of the past 20 years.