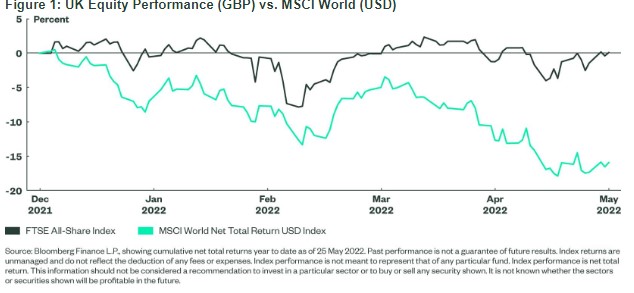

UK equities are one of the few regions that have shielded investors from the deteriorating macroeconomic and geopolitical backdrop so far this year. The key reasons behind the outperformance relative to other markets include fit-for-purpose sector composition, appealing valuation metrics and lower dependence on Russian resources compared to continental Europe. State Street SPDR ETF expects that the tailwinds for UK equities remain intact and should help to drive performance in the short to medium term. In addition, the GBP has weakened against the USD from 1.35 at the start of the year to 1.26 as of 25 May, providing an additional boost to exporters and global companies included in the UK FTSE ALL-Share Index.

Sector split tailored to answer challenges of today

The most important reason for the relative performance of UK equities is the sector and industry composition, which is well suited for the current environment.

One of the challenges equity markets have faced is a combination of rising yields and a flattening curve –the latter particularly present in the US. However, Financial companies in the UK, which account for 22% of the index, are well positioned in that regard as in addition to yield expansion, the UK curve is relatively steep, allowing to translate rising yields into improved net interest margins.

Investors also face the challenge of elevated commodity prices, which are one of the key drivers of inflation. We believe that, among core equity exposure, UK equities are the most suitable to play this theme. Energy, which is the most evident beneficiary of rising oil prices, accounts for 10% of the UK index, which is more than double the share in global developed equities.

The other sector that benefits from high commodity prices is materials. However, it is not applicable to the whole sector but more to mining companies. In that regard, the UK FTSE All Share Index offers compelling exposure to general mining companies, which account for 7% of the index while their share in MSCI World is less than 1%.

The significant presence of defensive consumer staples (15% of the index) and health care (12%) sectors provide necessary defensiveness against global economic slowdown. Finally, the consumer discretionary sector (11%) includes little to exposure to automobiles and parts, thus allowing investors to avoid some of the consequences of sanctions against Russia.

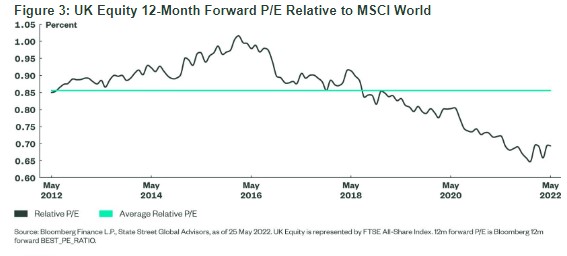

Krzysztof Janiga, State Street SPDR ETF strategist: “An important question to ask is whether UK equity outperformance can continue. We believe it can and continue to see a strong investment case, especially on a relative basis as the backdrop has not changed. Inflation is not abating with UK 9% CPI reported in April, elevated commodity prices persist, GBP depreciated against the USD and the UK yield curve remains steep, with at least four 25bps rate hikes priced in. Importantly, despite the year-to-date relative outperformance, UK equity valuations remain extremely undemanding compared to broader developed world equities, which implies that the tailwinds we noted may not be fully priced in. Indeed, an appealing 12-month forward earnings yield of 9.5% can provide level of protection against both monetary tightening and potential economic slowdown.”