Emmanuel Petit, Head of Fixed Income Rothschild & Co Asset Management.

The situation in the markets today is quite binary. Will the American central bank cause a recession in the United States to bring inflation back on target?

The answer to this question is obviously key to anticipating the behaviour of risky assets. Inflation figures suggest that the Fed will tighten financial conditions into restrictive territory, i.e., a policy rate above 3% Jerome Powell's ambition and the health of the US economy may prove him right, is to do so without causing a recession. But of course, there is no certainty... And if the inflation peak is not reached, the recession caused by a tightening of monetary policy seems inevitable. At present, the market is beginning to doubt that a rate hike of this magnitude will be possible, thereby stabilising long-term interest rate levels. If the inflation peak is near and monetary tightening expectations are stabilising, the question of the timing of reinvestment in credit bonds seems paramount.

However, visibility remains low, and a recession would obviously have an impact on the riskiest assets. So what is the right mix?

The parallel can be drawn with the European situation. Growth has also been impacted by the war in Ukraine, which has amplified inflationary pressures on commodity prices and, consequently, consumer confidence and growth. This growth gap reduces the European Central Bank's ability to intervene and is reflected in the wider rise in European Investment Grade(1) spreads than in the US.

Since the middle of last year, we have experienced a significant correction in the interest rate markets, particularly in the strongest part, with sovereign debt and Investment Grade credit, which has amplified the rise in sovereign rates. The correction was 10.9% on the European Investment Grade since the low point in rates last August, compared to 8.3% in March 2020, or 7.6% during the great financial crisis of 2008(2). In addition, and this is unusual, the segment underperformed the risk-adjusted high yield market(3), which fell by the same amount over the period.

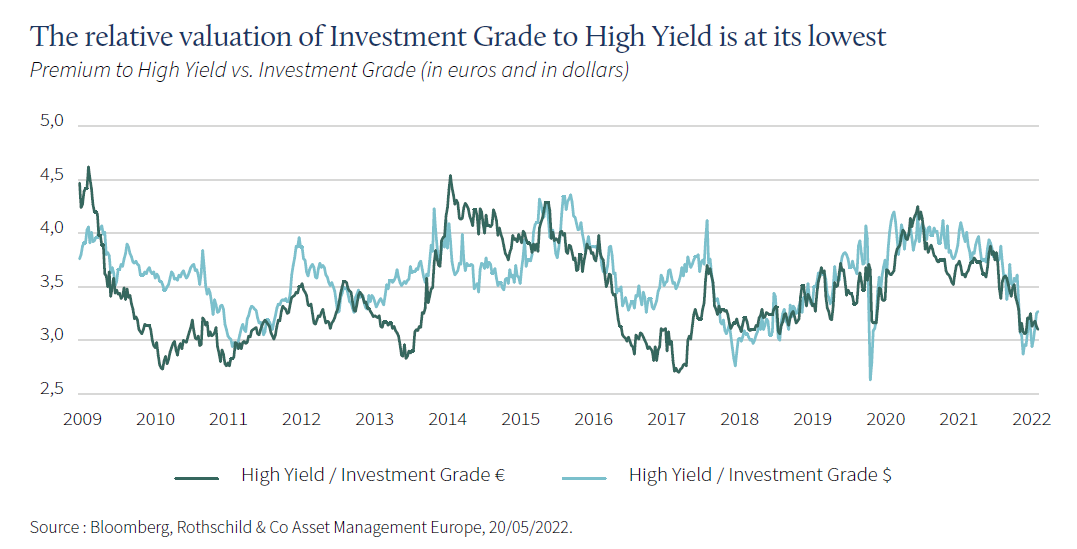

Investment Grade, therefore, currently offers an attractive return for the risk taken. Indeed, the companies in this segment have the necessary resilience to the turbulence that may be experienced, particularly after a period of improving their solvency and liquidity. Historically, we have been more tempted to reinvest in high yield in these correction phases. This time, we believe that the valuation of this asset class does not sufficiently reflect the risk of recession. We, therefore, favour buying opportunities on highly rated issues (between AAA and BBB-).

An Investment Grade portfolio with a 5-year maturity now generates around a 3% return, when it was paying just over 0% at the end of the last year(4). Beyond this average market return, the dispersion of opportunities is such that it is common to invest in issues that offer much higher returns.

Moreover, the primary market is less accommodating, with issue premiums at high levels, offering an additional yield relative to the market. As an example, we recently invested in a new issuer, TDC Net, a Danish company in the fixed and mobile telephony sector, rated BBB-, yielding 5.06% on a 6-year maturity(4).

The relative valuation of Investment Grade to High Yield is at its lowest

The tense market situation is also due to negative technical elements, notably fund outflows, the latter representing more than 4% of assets under management since the beginning of the year, i.e., €12 billion, on Euro Investment Grade(5) funds. However, we know that when buyers return, liquidity is as thin on the buy side as it was on the sell side in the bear market. Therefore, it is necessary to be able to reposition oneself before the others and reinvest when the market is selling because, after the rebound, the buying conditions are much less favourable.

A portfolio such as R-co Conviction Credit Euro, with its active management DNA, mostly invested in Investment Grade focused on BBB rating, has a yield of 4.4% for an average duration of 4(6). Therefore, the market allows us to have a level that we have not had for many years without significantly increasing the sensitivity to rate variations.

Our job as a bond manager is to optimise the risk/return ratio. We are now convinced that it is not necessary to take more credit risk to achieve a satisfactory return. We retain high yield issues with a positive, or at least resilient, credit trajectory, but our new investments are focused on Investment Grade. If we were to enter a recession, the portfolio would be better protected, as cycle recoveries are initially achieved through outperformance of Investment Grade.

(1) Investment Grade: Debt securities issued by companies or governments rated between AAA and BBB- on the Standard & Poor scale.(2) Source: Bloomberg, May 2022.

(3) High Yield: High-yield bonds are issued by companies or governments with a high credit risk. Their financial rating is below BBB- on the Standard & Poor scale.

(4) Source: Bloomberg, May 2022.

(5) Source: Bloomberg, May 2022.

(6) Source: Rothschild & Co Asset Management Europe - 25/05/2022.