The extended U.S. dollar rally has been both a cause and symptom of global risk-asset volatility in recent quarters. Global macro shocks and expectations for aggressive Federal Reserve (Fed) tightening intensified the bull run in early 2022, exacerbating financial strains and global economic weakness.

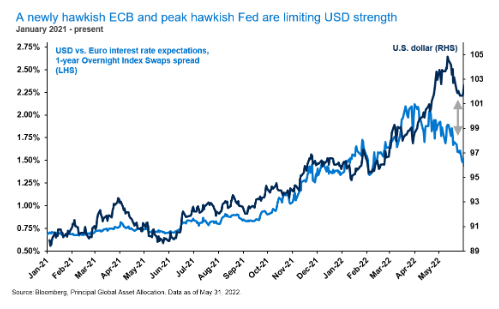

However, a recent reversal in U.S. and Eurozone market interest rate expectations, as measured by the 1-year Overnight Index Swaps spread, is starting to challenge the strong dollar. Since March, the Fed’s favored inflation measure, core PCE, has begun to roll-over, contributing to a growing “peak Fed hawkishness” narrative.

Meanwhile, with Euro-area inflation hitting a record high of 8.1%, the European Central Bank (ECB) is becoming more visibly concerned about price pressures and has escalated its hawkish tone. Recent comments from ECB Governing Council members suggest they will raise policy rates at each of this year’s remaining four meetings.

With U.S. dollar valuation signals also flashing red in recent months, a modest correction in the greenback may have been overdue. If the USD has indeed peaked and continues to weaken meaningfully from here, it could have reflationary implications for global risk assets. Unfortunately, though, with Europe likely to enter recession within the coming quarters and China still challenged by its strict COVID response, only a modest dollar depreciation is likely—hardly a gamechanger for struggling risk assets.