Luc Luyet & Alessandro Cortese, Pictet Wealth Management

- Precious metals have been hit hard by an ever hawkish Fed, high interest rates and a strong US dollar.

- In the short term, we see gold as the most resilient precious metal, given rising recession concerns.

- In the longer term, the structural shift towards green energy should lead to stronger industrial demand for silver and platinum, whereas palladium is likely to suffer from the shift.

Gold: waiting for a less hawkish Fed

Gold is mostly driven by investment demand, which in turn depends on the attractiveness of gold as a hedge against a decline in US dollar value, against high inflation and against general economic uncertainties. Investment demand is also significantly impacted by the opportunity cost of holding non-yielding gold.

Currently, the Fed’s monetary stance is particularly aggressive (brushing off recessionary noise), supporting a strong US dollar. Coupled with the high opportunity cost (given a positive US 10-year real interest rate), investment demand is unlikely to prove particularly supportive for gold, despite high inflation. A peak in US inflation and clearer signs of a marked deterioration in the US economic outlook are likely needed for the Fed to turn more sensitive to the recessionary narrative.

A Fed that softens its monetary stance, driven by economic growth concerns, would likely weigh on interest rates. Such environment may also prove less supportive of the US dollar. While global risk appetite may improve as the Fed returns to its old habits of nurturing the economic growth, the elevated global geopolitical tensions following the war in Ukraine are likely to last and could keep gold as an attractive option for investors looking for an hedge against global uncertainties.

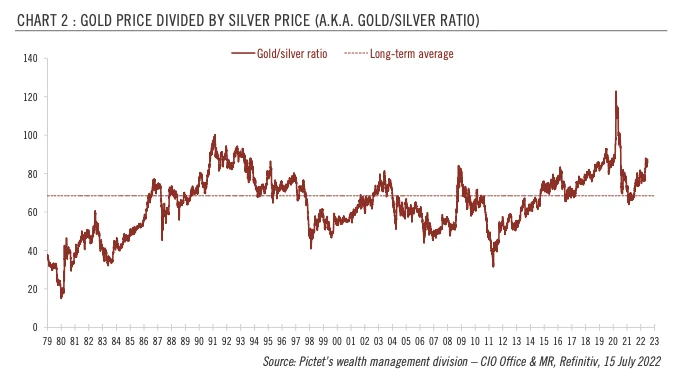

However, in the short term, US job and inflation data for June are definitively not favouring a softer Fed monetary stance (market expectations even point towards front- loading rate hikes for the next few meetings), which should keep gold under pressure. But our central scenario suggests that the Fed could turn more cautious on rates in September. That would also coincide with a seasonal surge in jewellery demand in the fourth quarter, setting the stage for a more supportive environment for gold. But the yellow metal may remain particularly vulnerable in the next few weeks, especially as sentiment in the futures market is significantly deteriorating from a high base (see chart).

Overall, we have decided to lower our three-month projection at USD1,750 per troy ounce (vs. USD1,780) to take into account the recent change in projections for the US dollar and the risk that the Fed remains hawkish longer than previously thought. We also acknowledge that in the next weeks, risks are clearly skewed to the downside (and a test of the key technical threshold at around USD1,680 looks likely). Our six-month and 12- month projections are also adjusted somewhat lower to USD1,820 (vs. USD1,860 previously) and USD1,860 (vs. USD1,900 previously) respectively.