By Peter Garnry, Head of Equity Strategy, Saxo Bank

The brief rally in global equities that lasted two months is now over as equities have rolled over. Equities recently have taken a big hit as the Jackson Hole conference made it clear to the market that inflationary pressures are still way too high despite the much tighter financial conditions. As a result policy rates will be tightened further putting the economy at risk of a recession and pushing up interest rates which will likely further lower equity valuations. All of this is not positive for equities and thus we expect more headwinds for equities as we get closer to yearend.

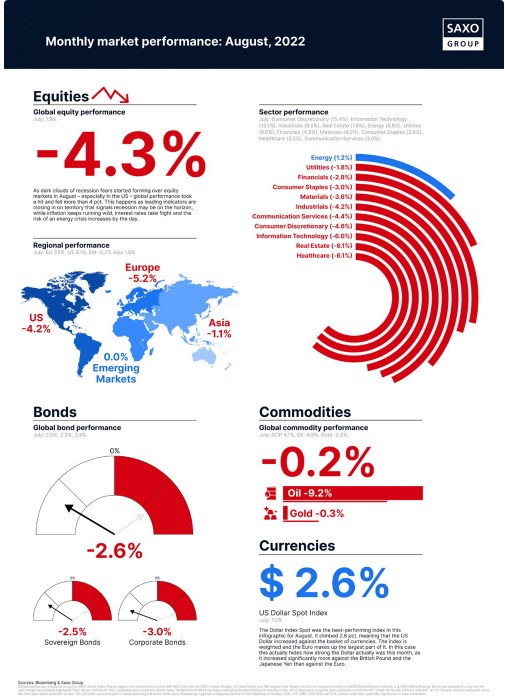

From 17 June to 16 August global equities rallied 14.7% as investors were convincing themselves that the world was turning a corner for the better on inflation. Speculative excesses that have not yet been slammed to zero by higher interest rate came bubbling back to the surface with meme stocks growing in fashion again. Then in August signs emerged that the nominal economy is remaining remarkably strong despite the tightening of financial conditions through higher central bank rates. The market suddenly felt less secure about its bet on inflation let alone bet that the Fed would begin easing early in 2023. Jackson Hole was the event that finally opened the door to reality for global equities and are now down 7.6% from the peak in August and down 4.2% for the previous month.

Equity valuations are still above the average since 1995 justified by the current revenue growth, operating margins, and cost of capital we are seeing. But one of these factors are about to become a key downside risk to equities, and that is the operating margin. It is right now historically high being around two standard deviations above the average since 1995.

For now companies have been able to pass on inflation to consumers because their savings from the pandemic shielded them. As the global energy crisis has intensified with energy costs in percentage of GDP expected to hit 13% this year consumers might be less able to absorb higher prices. Companies will most likely feel this dynamic in the quarters to come as they will experience price increases having a direct negative impact on volume and thus ending destroying more revenue than thought. The only natural response will be for companies to eat into margins which will likely offset and more the gains from higher revenue growth.

The growing worry as we are rolling into September is that the economy is headed for a recession in real terms but not in nominal terms also called stagflation. Normally central banks would begin cutting interest rates and loosen financial conditions but when you have recession while nominal prices are soaring you have an inflation problem and thus interest rates will not be cut but increased even more. Our hypothesis and best guess is still that structural inflation will be higher for longer than what the market is pricing in because energy deficits, deglobalization, and high nominal wage growth.

The US leading indicators are now at 0% y/y raising the probability of a recession over the next six months. The 2007 recession started in December after leading indicators were down 6% from their peak, and if we apply the same methodology this time and extend the current decline then the US economy could be in a recession by March next year. The main catalyst is the soaring energy costs as they suck out GDP that would otherwise have been spent on consumption of various goods and services.

Our main equity stance is still defensive. We are still overweight themes such as commodities, logistics, renewable energy, defence, India, and cyber security. We have changed our view on semiconductors from positive to negative as the industry will go through a massive adjustment with the news today that Nvidia can no longer sell chips to China is an evidence of. In terms of equity factors value and quality will continue to outperform growth.