By Ole Hansen, Head of Commodity Strategy, Saxo

Commodities suffered a broad retreat during a week where most of the directional input was being provided by another across-the-curve rise in US bond yields, a development that saw the 10-year US note’s yield jump to 4.33%, the highest level since 2007. A development being driven by the market once again being forced to re-evaluate the level of pain the US Federal Reserve is willing to inflict on the market through higher rates in order to bring inflation under control. Ole Hansen |

While the dollar from a broad perspective traded close to unchanged, the Japanese yen weakened beyond the closely watched 150 per dollar level, driven by a widening gap between rising US yields and the Bank of Japan-managed 0.25% ceiling on ten-year JGB’s. The mentioned rise in US yields followed on from hawkish remarks from Fed officials that led to the market now pricing in a 5% peak policy rate in early 2023, i.e. another 1.75% on top of the current rate.

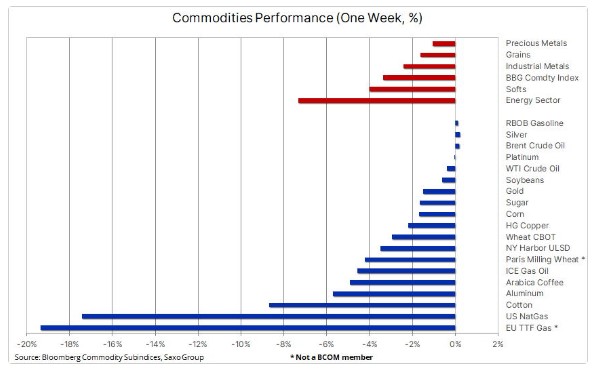

As the table shows, the losses across the commodity sector were broad with all sectors suffering declines. The Bloomberg Commodity Index which tracks a basket of major commodities spread evenly between energy, metals and agriculture traded softer by 2.5% with the index hovering near a March low. The weakness being primarily driven by natural gas which, despite having dropped by more than 40% since August, still trades up by more than 50% year-to-date, the result being an overly large index weight of 12.6% compared with its 8% target weight.

Gas prices in Europe and US see steep weekly declines

US natural gas futures headed for their longest stretch of weekly declines since 1991 as stockpiles continue to build at a faster than expected pace ahead of winter. The November front month contract traded down by more than 20% on the week and overall, it has now lost more than 45% of its value since the August peak, driven by mild autumn weather and rising production. In addition, the Freeport LNG export terminal explosion on June 8 has reduced exports, thereby supported an unusual strong inventory build. Total stocks have risen to 3342 billion cubic feet to trail the five-year average by only 5%, compared with 17% back in April.

In Europe, the price of Dutch TTF benchmark gas continued its week-long collapse and at one point traded close to €100/MWh, a level we did not think it could reach until the winter demand outlook became clearer into January. There are multiple reasons why the spot price has more than halved since September, the most obvious being the fact the price should never have traded above €300/MWh in the first place with no shortages seen at any point during a six-month period of pain for European consumers and industry. That aside, gas prices are falling due to:

Gas storages operating close to full capacity.

- A mild start to the autumn combined with consumers and industry cutting demand.

- LNG carriers lining up to offload cargoes into a current oversupplied market, a development which in the short term could drive prices even lower.

- Russia’s Gazprom ’s ability to shake the market has been much reduced with just two pipelines currently in operation.

- EU leaders agreeing to support further work toward a price cap to contain the energy crisis.

The biggest risk to successfully navigate through the coming winter is complacency from consumers showing less demand constraints amid lower prices.

Crude oil : stuck in neutral

The crude oil market remains stuck in neutral with multiple uncertainties regarding supply and demand keeping prices locked within a relatively narrow range. The slight weakness seen this past week once again being driven by recession risks as US interest rates continue their rapid ascent. Crude and its related fuel products however continue to be supported by the risk of continued tightness driven by a period of supply uncertainty in the coming months as OPEC+ cuts supply, and the EU implements sanctions on Russian oil.

The tightness being clearly visible through the shape of the forward curve where an elevated level of backwardation in crude oil continues to show solid demand for barrels that can be delivered immediately. An example being the $5.3 per barrel spread between the December 2022 and March 2023 contracts, currently the highest in almost two months. The main focus in terms of tightness remains the northern hemisphere product market where low available supplies of diesel and heating oil continues to raise concerns.

A situation that has been made worse by the OPEC+ decision to cut production from next month. While the continued release of US (light sweet) crude from its strategic reserves will support production of gasoline, the OPEC+ production cuts will primarily be provided by Saudi Arabia, Kuwait and the UAE, all producers of the medium/heavy crude which yields the highest amount of distillate.

Next week, the focus will turn to quarterly earnings reports from five of the western world’s biggest oil and gas majors, who have a combined market cap of more than $1 trillion. Royal Dutch Shell and TotalEnergies results are due on Thursday, along with Chinese PetroChina, while Exxon, Chevron and Equinor will deliver their results on Friday. The market will be watching for their respective outlook on demand and whether the growing political pressure for spending on new supplies will translate into improved investment appetite.

Gold holds onto support despite another jump in US yields

Gold traded lower on the week in response to the mentioned spike in US bond yields and the market upgrading their expectations for how high the Fed funds rate will go before the Federal Reserve feel comfortable that rates are high enough to bring inflation under control. While rising yields will continue to create a great deal of headwinds for precious metals, the reason why gold has so far managed to hold onto support at $1617, the September low and 50% retracement of the 2018 to 2020 rally, is likely to be driven by a very challenging geopolitical situation.

However, these supporting concerns did not prevent a continued exodus from bullion-backed ETFs which gathered pace this past week. With the dollar being the main safe-haven bet, some investors have started to find value at the short end of the US yield curve where the two-year note is now paying a yield close to 4.6%.

Looking ahead, we see no reason to change our long-term bullish view on gold, with support potentially coming from the risk of a policy mistake sending US economic growth, the dollar and bond yields lower. In addition, we fear that the long-term inflation level may end up at a higher level than is currently being priced in by the market. Failure to bring long-term inflation down towards market expectations may trigger a major, and gold supportive, realignment between (rising) breakeven yields and (falling) real yields. For now, and until we get a clearer idea about when US interest rate expectations start to roll over, the precious metal market is likely to trade defensively.

Cotton and coffee drops as consumers tighten their belt

Besides the natural gas led slump in the Bloomberg Commodity Energy Index, the soft commodity sector has taken a tumble with losses being led by cotton and coffee, both depending on a healthy spending behaviour by consumers across the world. Cotton, down 42% since May, has been troubled by demand headwinds with US, one of the major shippers, seeing export demand tumbling from a year earlier, especially from key buyers in Asia. Adidas and other clothes vendors have seen inventories rise due to lower consumer demand in major western markets.

The same developments are also increasingly impacting coffee prices which up until recently had weathered most of the economic slowdown storm amid a very tight supply outlook. This past week, however, the price of Arabica coffee dropped to a 13-month low on a combination of weaker demand and reduced worries about the supply outlook in Brazil, the world’s top exporter.