By Peter Garnry, Head of Equity Strategy at Saxo

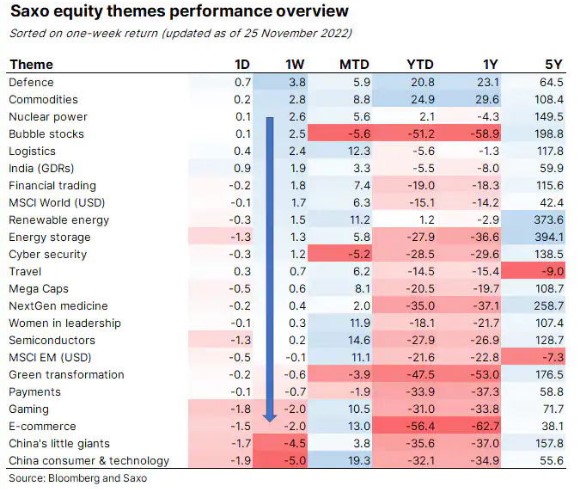

The defence basket is continuing its momentum up 3.8% last week. The performance means that the defence basket could get closer to end the year as the best performing theme basket this year. The biggest gainers in the defence basket last week were Rolls-Royce and Leonardo.

Peter Garnry |

Our Chinese equity baskets, on the other hand, were down around 5% last week as China is finding it increasingly more difficult to leave its strict Covid zero policies behind as case figures are surging again and protests are erupting across several locations in the country including the main manufacturing hub for Apple and its iPhone.

Could defence stocks end the year on a high?

The defence basket was the best performing basket last week gaining 3.8% as the ongoing geopolitical landscape in Europe around the war in Ukraine will continue to drive military spending higher. With just one month to go and the Chinese reopening narrative shattered to pieces over the past week commodities could be under pressure, so if defence stocks can muster more momentum they might even end the year as the best performing theme basket.

The two best performing stocks in the defence basket last week were Rolls-Royce and Leonardo up 7.5% and 6% respectively. Roll-Royce seems to have turned a corner and 10 days ago the company’s credit was lifted to positive outlook by S&P from stable suggesting the underlying cash flow generation is improving. Leonardo is still enjoying the tailwind from its good Q3 results and the Q4 performance will likely be driven by another good quarter in its defence and helicopter segments despite looming inflationary pressures on its input costs.

China continues to be out of sync with the world

The biggest outliers last week among our equity theme baskets were our two Chinese equity baskets declining 4.5% and 5% respectively as rising Covid case figures dented the narrative that China can smoothly reopen their economy. Already last week there were increasing protests at different locations in China including Apple ’s biggest factory that produces its key product the iPhone. This has led sell-side firms to cut their forecast for iPhone production and investors are increasingly worried Apple ’s supply chain risks. The protests against China’s Covid zero policies have not eased over the weekend so this theme will continue to impact markets this week.

If we zoom out and take a longer look at Chinese equities it has been miserable period since early 2010 with Chinese equities underperforming MSCI World in total return USD terms by 7.9% annualized. But especially the period since mid-2021 has been brutal with the Chinese economy undergoing severe calibrations amid a troubling real estate sector and now the disruptions from the strict Covid zero policies. We remain underweight Chinese equities long-term as the common prosperity policies will continue cause headwinds for Chinese corporate sector profitability which has been very weak since the pandemic started.