Review – No conciliatory end to the year

Market review & Outlook by J. Safra Sarasin

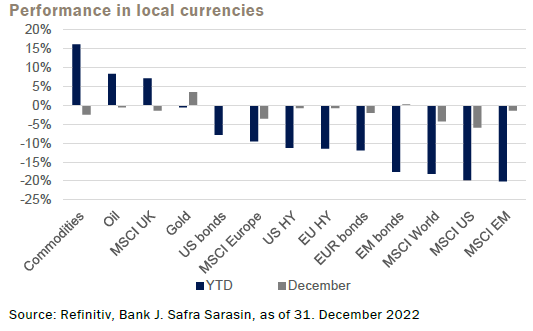

The month of December is typically the time to look back not only on the past month, but on the whole year. Hence the sorting according to annual performance in the following chart. Commodities – especially energy – performed strongly positive, which is why the UK stock market, which is heavily driven by commodities, also ended the year on a positive note. On the other side of the return spectrum are the other equity markets. Emerging markets equities suffered the biggest losses, followed by US equities.

Bonds end the year on a negative note primarily due to the very rapid rise in interest rates and the associated revaluation. The riskier bond spectrum, emerging markets as well as high yield bonds, have lost more in this environment than higher quality investment grade bonds. Gold has disappointed this year. Record high inflation and a war in Europe were not enough to offset the negative effects of sharply higher real interest rates and a stronger US dollar.

Macro Outlook – From Inflation to Growth Concerns

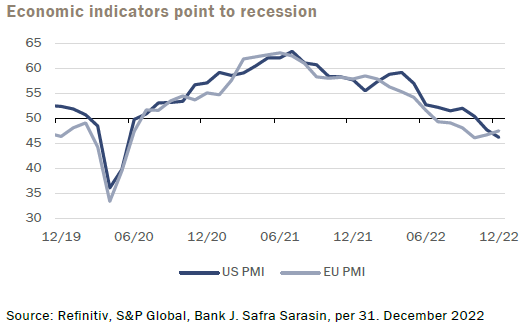

The beginning of the year was dominated by inflation concerns, driven in particular by Russia's war of aggression against Ukraine. Following massive interest rate hikes by global central banks, inflation rates have now started to fall again. However, lower inflation is also a consequence of weaker demand due to deteriorating economic prospects. Numerous indicators are already pointing to a recession in Europe. And in the USA, too, it seems likely to be a reality in the coming year.

The monetary policy turnaround by central banks in response to the rise in inflation is unprecedented in the historical context in terms of the speed as well as the extent of interest rate hikes, giving them room for monetary action again. However, central banks emphasize the continued need for further control of inflation. In-terest rate cuts this year are thus rather unlikely.

Bonds – Massive rise in yields leads to losses

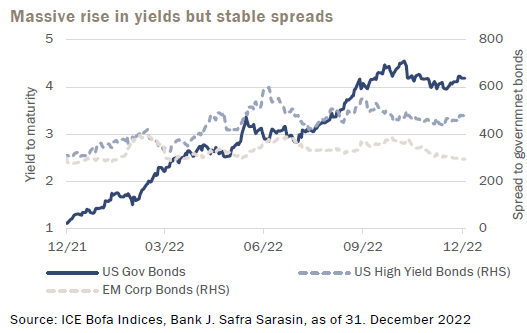

Yields have risen not only at the short end of the yield curve. The long end has also corrected massively, as the following chart shows. A year ago, we had some thoughts on “alternatives to Bonds”. After the significant rise in yields this year, this question has become obsolete. Surprisingly, corporate bonds have been ro-bust relative to government bonds in this environment, as evi-denced by the narrow ranges of spreads on high-yield bonds as well as emerging market bonds. However, with tighter monetary policy and a weaker economic cycle, we also expect default rates to rise in the coming year. This should also be accompanied by correspondingly higher spreads.

Equities – Earnings expectations remain strong

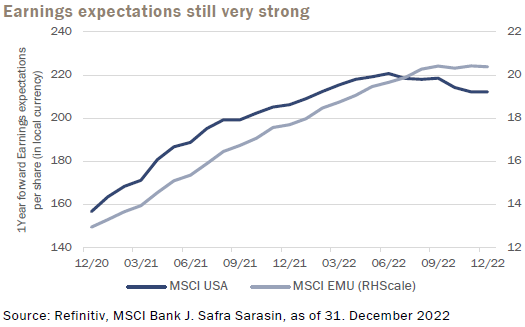

Equity markets have corrected sharply this year, mainly due to in-terest rate developments, especially higher real yields. However, corporate earnings expectations remained high and have even risen since the beginning of the year. Nevertheless, the worsening economic environment is likely to ultimately leave its mark and have a negative impact on companies' earnings and margins, which is also likely to be reflected in the stock price.

However, if China's changed COVID policy leads to strong positive momentum and thus an increase in consumption in China, the eco-nomic outlook in other parts of the world, especially in Europe, could also improve. In particular, consumer and travel activity around the “Chinese New Year” at the end of January should be instructive in this regard. Our research sees the possibility that a recession can be mitigated by the opening of the Chinese econ-omy. However, we remain cautious due to conflicting information on current COVID case numbers and wait for further clarification and positive indicators.

Asset allocation – Cautious positioning at the beginning of the year

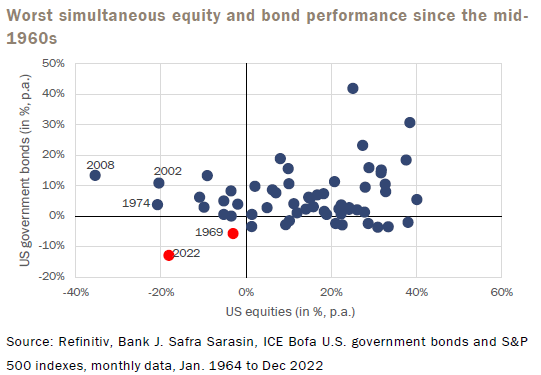

As mentioned and evident in the chart, equity performance is among the worst five years since the mid-1960s (data availability). In the other negative years, however, government bonds have helped to mitigate within the portfolio context. The only year with both negative equity and bond performance was 1969, but to a much lesser extent. On the bond side, this year's performance is by far the worst.

While a large part of the correction in bonds should be behind us, the risk of a further correction on the equity side remains high, es-pecially if earnings expectations turn out to be disappointing. Ag-gressive central bank policies also make a “soft landing” scenario without recession unlikely at present. For this reason, we remain underweighted in equities at the beginning of the year and defen-sively positioned within the equity allocation.

In fixed income, we prefer short-dated investment grade bonds due to their attractive yields. We remain underweight in the risky high-yield and emerging market bond segment and expect better entry points after the recession subsides and, subsequently, credit spreads have widened.

Among alternative investments, we see good prospects for catas-trophe bonds, especially after the reassessment of hurricane “Ian”. In addition, gold appears to be a reasonable addition for di-versification and risk mitigation in the environment of increased uncertainty – both political and economic. Broadly diversified com-modities remain interesting in the long term due to the current “su-per cycle”. In the short term, however, they are also affected by the deteriorating economic environment.