By Charu Chanana, Market Strategist at Saxo

Even as inflation concerns continue to be the top concern for markets, weak US retail sales and industrial production data overnight has sparked some concerns of an economic slowdown. The strength of the labor market still provides room to argue in favor of a soft landing vs. a steep recession, and markets will becoming increasingly sensitive to payroll data going forward. Earnings will also start to take a bigger focus with major tech players starting to report next week.

The global economic cycle is at a critical juncture, and investors are trying to weigh up the options between whether we get a soft landing or a recession. While US housing data and survey data has been weak for months now, it is the real economic data that is now starting to show a significant deterioration.

The markets are also evolving on their interpretation of economic data, coming from a point where bad news was good news and suggested that the Fed will pivot on its rate hike cycle which provided a bid to equities. Now, bad news is bad news, and it is starting to send shivers about what the Fed’s tightening cycle means to the growth outlook.

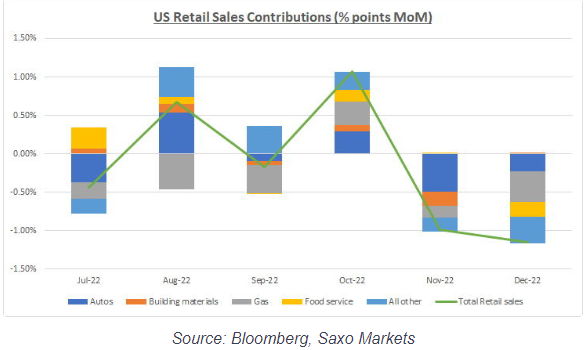

This shift in perspective comes from a weak set of US data last night. December US retail sales fell 1.1% M/M, deeper than the consensus 0.8% decline with a sizable downward revision for the prior to -1.0% from -0.6%. Industrial production fell 0.7% M/M in December, deeper than the consensus -0.1%, with the prior downwardly revised to -0.6% from -0.2%. Manufacturing output also declined by a larger 1.3%, deeper than expected -0.3% and the prior revised to -1.1% from -0.6%

The state of the US consumer; payroll data will be key

This shift in narrative is raising some key questions about the strength of the consumer which has been the key pillar of strength in this extremely tough macro environment. With inflation and interest rates in record high territory, consumers are likely to find ways to cut costs. This translated into a reduction of excess savings last year, as spending shifted from goods to services and from high-priced goods to lower-priced goods. Some risks have emerged to a deterioration in services demand as well, with the December retail sales print also showing a deterioration in restaurant sales, which serves as a proxy for spending on services.

But with the labor market still tight, it is hard to see consumer spending decelerate sharply. That being said, markets will continue to look for more signs to judge the state of the US consumer and a big focus will be on labor market and wage data going forward. Wage pressures are cooling, especially in industries that saw the largest wage gains over the past year due to labor shortages, including leisure and hospitality and wholesale trade. But for now, jobs are still growing and that keeps the outlook of the consumer supported against any sharp and steep reversals. In the weeks to come, we could see market volatility shifting away from CPI days to NFP (nonfarm payroll) days as the jobs data comes under greater scrutiny.

Watch for earnings

The next nonfarm payroll data is after two weeks (due 3rd February). In the meantime, markets will be getting a lot more to digest from the earnings front. Consumer staples giant Procter & Gamble reports today, followed by Kimberly Clark next week. After Netflix reports today, tech earnings also pick up next week with Microsoft and Tesla reporting, while Apple , Amazon , Alphabet and Meta report earnings a week later.

Factset estimates that S&P500 will report earnings decline of 3.9% YoY in Q4, as analysts are revising their estimates lower. Our Equity Strategist Peter Garnry has also written numerous equity notes suggesting that company earnings and margins are likely to come under pressure this year as pricing power declines and costs (esp wages) remain sticky.

Investment Implications

We believe that earnings disappointments will continue to spark further fears of an economic slowdown. But the global recession fears are for now taking a backseat with Europe weathering the energy crisis better and China’s economy reopening at a rapid pace. For now, inflation fears continue to be somewhat more pronounced but if recession fears start to take a firmer hold, that could likely nudge investors towards safe havens such as bonds.

If market pricing for economic growth deteriorates further, earnings estimates could get hurt even more and we could potentially see more pain for growth stocks. This necessitates the importance of a diversified and balanced portfolio once again, despite dismal results for a 60/40 portfolio last year. We also believe Asian equities have the potential to outperform US equities in 2023, as discussed in this video, and provide some attractive valuation levels to consider.