By ODDO BHF AM

Since the beginning of the year, all ODDO BHF Polaris funds are allowed to invest in gold certificates as a diversifying addition to the portfolio. Previously, this was only possible for the ODDO BHF Polaris Moderate. A reason to take a closer look at the precious metal. "All that glitters is not gold" is a well-known saying. Especially during severe economic crises, many investors remember this phrase. When shares go downhill or inflation gnaws away the value of bank deposits, gold is seen as a haven of stability. The most important reasons for this are that the supply of gold is limited and cannot be artificially increased as is the case with paper currencies that can be created indefinitely (e.g. US dollar, euro, renminbi). In combination with its resistance to wear and its seductive shine, gold has been sought after for thousands of years as a means of storing value. These characteristics mean that the price of gold often moves in the opposite direction to share prices. As a result, gold can significantly reduce the volatility of a portfolio.

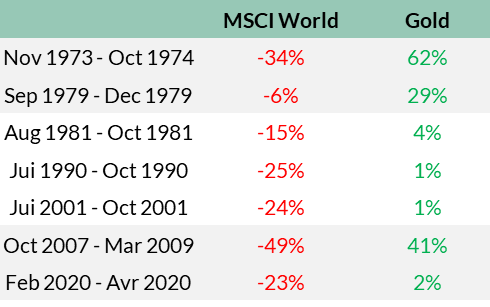

The table below shows the cumulative performance of MSCI World and gold in bear markets just before or during recessions over the past 50 years. Across all bear markets, especially during the 2008 financial crisis, gold has done a very good job of stabilising the portfolio. Even in the current economic headwinds, gold has so far proven its stabilising effect. From February 2022 to January 2023, gold gained 7% in euro terms, while the MSCI World lost 13% in euro terms. In our view, a gold allocation of up to 10% in a pure equity portfolio (correspondingly less in a mixed portfolio) can therefore have a stabilising effect on the portfolio return.

Figure 1: Cumulative performance of the MSCI World & gold in bear markets during recessions

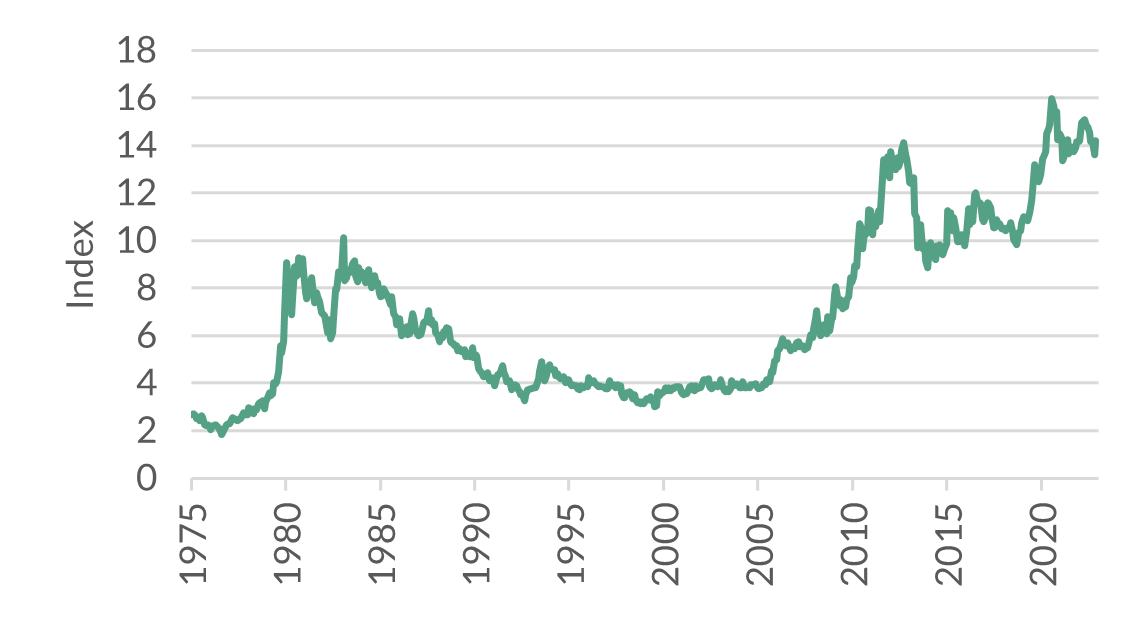

Looking at the real (inflation-adjusted) gold price, it has corrected somewhat since its all-time high during the Corona crisis in August 2020. Nevertheless, the real gold price remains at historically high levels. Against this background, is it attractive to use gold as a means of diversification?

Assuming a return to the long-term mean, one should be cautious. Bonds have become more attractive due to the rise in interest rates, especially since gold does not yield any returns. However, the gold price has recently withstood the headwind of interest rate hikes and a firm US dollar surprisingly well. After all, there are plenty of reasons for a further rise in the gold price.

Figure 2: Real gold price

Central banks have been buying more and more gold in recent years. The freezing of Russian foreign exchange reserves, which were denominated in euros, Swiss francs, pounds or yen, has shown many countries that maintaining gold reserves in their own countries can be very important in order to be able to continue paying for imported goods. According to the World Gold Council, official gold reserves held by central banks are at a record high. The top buyers are emerging countries like Turkey, Egypt, Iraq, India or Argentina, which want to become less dependent on the US dollar.

Furthermore, stubbornly high inflation could support gold. The higher the price increase, the more the value of bank deposits melts and confidence in central banks dwindles. In addition, inflation increases production costs for gold miners (at ~US$1,200 per troy ounce in Q1 2022), which favours a rise in gold prices.

In the flexible multi-asset funds of the Polaris fund family, it therefore appears attractive in our view to have the possibility to invest into gold at the right moment.