By Jan Bopp, Sarasin

Macro data remain robust and inflation data higher than hoped for. After a short breather, interest rates continue their upward trend and equity markets come under selling pressure.

Jan Bopp |

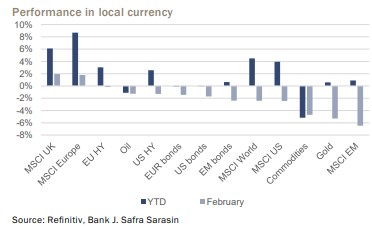

Performance in local currency

Source: Refinitiv, Bank J. Safra Sarasin

On the government bond markets, this development led to a significant rise in yields back to the levels seen at the beginning of the year. Accordingly, investment grade (US -1.7% / EUR -1.5%) and high-yield bonds (US -1.4% / EUR -0.2%) declined sharply, with US and especially emerging market bonds (-2.4%) coming under pressure. For commodity markets (-4.7%), this month was also characterized by significant price declines. A stronger US dollar and rising interest rates weighed particularly on the gold price (-5.3%). Oil declined by -1.3%. Macro outlook – Persistent inflation As recently as last fall, a majority of economists were worried about an impending deep recession. Fears of empty gas storage facilities, idle industrial plants and high unemployment dominated the market outlook. A hard landing of the economy seemed inevitable. Now, several months later, it is hard to ignore the fact that the currently clearing clouds on the economic horizon - in the US, for example, there are few signs of an imminent contraction in economic activity - are accompanied by a not inconsiderable problem: Upside risks to underlying inflationary pressures. The latest inflation figures from the US and the euro zone are already pointing in this direction, which has led the rates market to price out most of the rate cut fantasies for the second half of the year, and the terminal rate has climbed to a new cycle high.

Bonds – Reality check

In the face of renewed inflation and interest rate concerns, the performance of global bond markets is back to where it started after a brilliant start to the year. Two-year US government bond yields recently soared to levels as high as 4.85%, the highest since 2007, while ten-year yields reached their highs for the year at just under 4%. Ten-year Bund yields, in turn, recently retested this year's highs of just under 2.6%.

The reality check and the associated reassessment stem not least from the gradual realization that hopes of a smooth disinflation in the direction of the 2% target levels of the US Federal Reserve and the European Central Bank and thus of key interest rate cuts before the end of this year, garnished with a “soft landing” of the economy, were not sustainable in this form, regardless of monetary policy braking effects.

Equities – Looking for direction

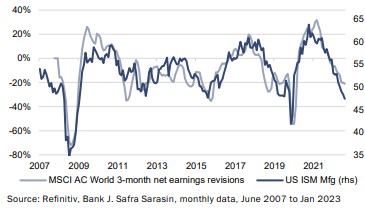

Equity markets are also looking for new orientation in this environment. As usual in such phases, attention is focused on the classic market drivers such as corporate earnings and interest rates. With regard to the former, the reporting season for the fourth quarter of 2022 provided only limited insights. There was by no means the massive downward revision in the outlook for the coming quarters feared by some, but at the same time no improvement either. With regard to earnings revisions, on the other hand, downside risks remain unchanged in view of the environment of considerable growth uncertainty and likely rate increases.

Earnings revisions remain under pressure

In the current year, the world's growth focus is likely to move away from the US toward Asia. The dollar should suffer as a result. This will benefit equities from the emerging market regions as the pressure on central banks in these countries will also be reduced.

Asset Allocation – Higher for longer

The sharp decline in equity risk premiums, especially for US equities, due to easing growth concerns remains a concern as it makes the asset class vulnerable to macroeconomic surprises. While we have tactically reduced some of our underweight in equities over the past months against the backdrop of easing economic risks and stronger macro data, we remain vigilant. The high degree of uncertainty surrounding the direction of central bank policy with regard to further tightening of the monetary stance is forcing market participants to take a close look at short-term economic developments. Looking ahead to the second half of the year, investors should keep in mind that a slowdown in economic momentum is, however, almost inevitable. As soon as the interest rate hikes fully unfold their restrictive effect, private consumption in the US and the euro zone should also decline noticeably. At sector level, following the strongly cyclical equity market rally of recent months, we favour defensive sectors in particular.

Cyclical sectors outrun macro data

However, given the scale and speed of the recent rate hikes, the fixed income market is likely to have already priced in quite a bit of good growth news. For a further significant rise in yields, the upcoming data releases would have to underpin a continued positive growth picture. In the short term, this suggests that interest rates are likely to consolidate at current levels. We continue to favour short-dated government and corporate bonds from the upper rating spectrum as well as inflation-linked bonds due to even more inverted yield curves.

The low credit spreads on high-yield bonds are to be viewed with a critical eye. We therefore remain cautiously positioned in this segment despite high interest rates. By contrast, the outlook for emerging market bonds is brightening in the medium term. The positive growth differential for emerging market economies, easing inflationary pressures and a weaker dollar all speak in favour of the asset class. At the same time, however, it would be wrong to spread too much undifferentiated optimism about emerging markets. Selectivity remains crucial for investment success.

We are neutrally positioned in alternative investments. We have increased our allocation to commodities as the structural changes, in particular due to the pursued de-carbonization of the global economy, are likely to usher in the start of a new super-cycle in commodities and the increasing demand for resources from China will also support the segment in the short term.