By Peter Garnry, Head of Equity Strategy at Saxo

The keyword for our team after the Powell speech is 'recession by design' as the Fed has clearly moved closer to panic mode indicating a willingness to push the policy rate higher than previously thought and for longer.

Peter Garnry |

The outlook on inflation seems more uncertain and the policy rate trajectory is now leaning towards a new policy mistake where the Fed maybe gets too aggressive in their panic to lower inflation creating a recession. Seen in that light the valuation premium in S&P 500 relative to the historical average since 1994 seems illogical and thus the downside risks in US equities are coming into play again.

Recession by design as panic creeps in

Powell delivered a hawkish message yesterday on US policy rates immediately causing a repricing the next FOMC rate decision from 30% probability of a 50 basis points hike to above 70% probability. There was a sense of panic with the Fed getting uncomfortable about inflation and is concerned that it is getting too sticky at a higher high level. It seems the only way to get inflation under control is to design a recession to reduce demand enough for inflation to come down. If we agree on the premise that central banks do not have a good model for inflation dynamics, which is why we ended up with late policy response in the first place, then the risk is now that the Fed due to being in panic mode will move the policy rate too aggressively causing a recession.

The most energetic market response was in the US 2-year yield climbing above the 5% level, the highest level since 2006 before the credit boom was killed triggered the Great Financial Crisis. The US 10-year yield was more muted remaining around the 4% level and likely the cause of the somewhat relaxed response to Powell’s clear hawkish message and signal to push policy rates higher than anticipated. But as time goes the pressure on short-term interest rates will slow down the economy, unless of course that fiscal measures keep things hotter for longer which seems to be the case. The US fiscal deficit has expanded by over 300 basis points since July as the US government is stimulating the economy and helping lower income families with the pressures from inflation. It is a natural reaction function in politics but it prolongs the adjustment. S&P 500 futures were 1.6% lower yesterday and are already attempting to rebound this morning in early trading hours.

There is a fundamental disconnect in US equities

The equity option market also remains calm relative to the recent past with the VIX Index still below 20 suggesting that Powell’s message has not been heard in the hallways of equities. Is it intentional that equities are overlooking the lurking dangers of a Fed in panic or is it a sign of ignorance? It is tempting to suggest that it is the later as the new message from Powell cannot be anything else than increasingly a one-way risk-off road for US equities.

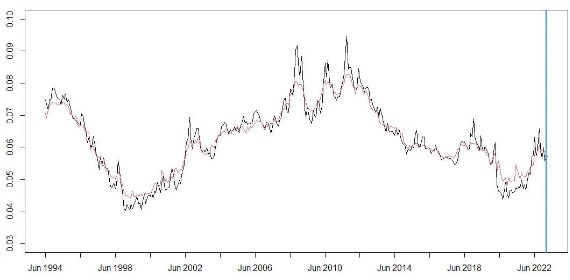

The current 12-month P/E ratio in the S&P 500 is 17.5x which is above the 16x average since June 1994. Given the uncertainty over inflation, the war in Ukraine, tensions with China, and the repricing of policy rates it is just odd that investors are willing to pay a premium above the historical average. It is also important to note that in Q4 last year, when equities were under pressure and were down more than 20% from the peak, that Berkshire Hathaway was not a net buyer in either private equity or public equity markets. Charlie Munger and Warren Buffett that are the most experienced equity investors alive today have both taken the position that time is on their side and they are in no rush to be aggressive.

When we take a look at our S&P 500 valuation model, which aims to explain the variance in the 12-month forward P/e ratio, then the most important variables that explain the forward P/E ratio are USD spot rate, housing market indicators, consumer confidence, M2 money supply growth, hourly earnings, and the 2-year yield. When we take all the macro indicators into account there is no short-term mispricing. However, the more important thing is in which direction these indicators are moving. Given Powell’s message yesterday most on the important indicators are likely to move in the direction that would dictate a lower P/E ratio. It feels a bit like the calm before the storm.

The plot shows the 12-month forward earnings yield (black line, inverse of P/E ratio) and our model’s 12-month forward earnings yield (red line) based on multiple macro indicators.

S&P 500 12-month forward earnings yield vs Saxo model | Source: Bloomberg and Saxo