From TINA to TAPAS: there are alternatives again

Prof. Dr. Jan Viebig, Global Co-CIO ODDO BHF AM

So far this year, stock markets have shown their friendly side. Especially European markets which, measured by the Euro STOXX index, have achieved a total return of around 13 percent since the beginning of the year. This is also true of US markets, with a total return of around 3.5 percent for the S&P500 index and 10 percent for the technology-heavy Nasdaq Composite index. Various reasons explain these positive performances: towards the end of 2022, the energy supply situation in Europe began to ease. Energy prices retreated. As a result, the scenario of a severe crisis receded into the background.

Falling energy prices also fuelled hopes for an end to the energy supply shock. Furthermore, with the abandonment of the zero-covid strategy and the transition to a more expansionary fiscal and monetary policy, a revival of economic growth in China also appeared increasingly likely. After a disappointing year in which Chinese real GDP growth only reached 3 percent, Beijing is now targeting growth of "about 5 percent" for 2023.

In the current interest rate environment, there are attractive alternatives to equities again for the first time in many years.

However, market participants underestimated the persistence of inflation. The massive surge in inflation over the past year and the sharp rise in producer prices are contributing to large adjustments in the macroeconomic price structure. Wages in the USA are rising. In Europe - especially in Germany - trade unions are demanding significant wage increases. In the face of sharply higher producer prices and rising salary demands, upward price pressures are broadening. Core CPI inflation in the US remains at 5.6 percent, well above the Federal Reserve's 2 percent target. In the euro area, the core inflation rate continues to point upwards, with a February 2023 figure also reaching 5.6 percent, according to Eurostat estimates. Prices for services and food in particular (not included in the core rate) are fuelling inflation in Europe.

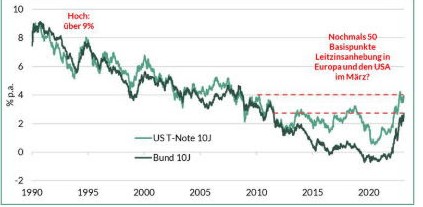

As a result, investors have had to revise their expectations regarding interest rate policy. In view of recent developments, central banks are likely to head for significantly higher interest rate levels than previously expected. Hopes for an imminent turnaround in monetary policy may be premature. ECB President Christine Lagarde recently reaffirmed her intention to raise key rates by 50 basis points in March and held out the prospect for further hikes. Austria‘s central bank Governor Robert Holzmann even spoke of four further increases of 50 basis points each. We expect the ECB Governing Council to raise key interest rates by 50 basis points on 16 March 2023 as already announced. Currently, the money market is forecasting an increase in ECB deposit rate to around 4 percent by the third quarter of 2023.

At the beginning of February, the US Federal Reserve initially slowed the pace of interest rate increases, which was limited to a 25 basis points rate hike. However, high core inflation and strong labour market data have forced it to backtrack. At his hearing before the Senate Banking Committee, Fed Chairman Jerome Powell expressed dissatisfaction at the extent of the inflation slowdown and hinted at the possibility of increasing the pace of rate hikes again: "... the latest economic data have come in stronger than expected, which suggests that the ultimate level of interest rates is likely to be higher than previously anticipated."

For years, TINA has applied to investors. The abbreviation, which stands for "There Is No Alternative", became a catchphrase among market participants. It meant that in an environment of very low or negative interest rates, investors could only generate a significant return with equity investments. The era of low interest rates is a thing of the past. With bond yields picking up, investors are now, and for the first time in many years, faced with the question of which asset class to choose. Creative analysts have already come up with an acronym for that: TAPAS. Not a reference to the Spanish appetisers, but to the fact that there are alternatives to equities again in an environment of rising interest rates. TAPAS stands for "There Are Plenty of Alternatives".

And indeed, the graph shows that yields on US and German government bonds have risen significantly in recent months. For 10-year US government bonds, investors currently receive a yield averaging 4 percent. For 2-year US government bonds, the yield is even higher than 5 percent. Bonds of the Bund with a 2-year residual term are currently yielding about 3.3 percent, almost 80 basis points above the level at the beginning of February. The yield of 10-year federal government securities is about 2.7 percent.

Once again, the inversion of the yield curve is very pronounced. Corporate bonds look even more attractive than government bonds, since not only the supposedly risk-free interest rate, but also the risk premiums of corporate bonds are again significantly higher than in the nearforgotten times of negative interest rates. In the current interest rate environment, there are attractive alternatives to equities again for the first time in many years.