FOMC statement and updated dot plot/economic projections at 7pm CET - Wednesday Chair Powell press conference at 7:30pm

Frederik Ducrozet, Head of Macroeconomic Research, at Pictet Wealth Management ahead of tomorrow's Fed meeting (March 22, 2023).

We expect the Fed to hike rates by 25bps, keep QT unchanged, and remove the forward guidance of “ongoing rate increases”. Focus should be squarely on the 2023 median dot and distribution, although Chair Powell will most likely downplay the importance of dots given elevated economic uncertainty. We expect the median dot to remain unchanged at 5-5.25%, which would imply another 25bps rate hike in May (assuming they hike by 25bps tomorrow). We see risks that some dots will already show cuts or pause this year. We see non-zero risk of a stop in QT at this meeting, or of Powell signaling a willingness to adjust QT going forward based on financial market developments.

Powell Press Conference

Chair Powell will have to walk a fine balance – he’s likely to suggest a preference to use existing and emergency liquidity tools to address financial stability, while suggesting using interest rates to bring inflation down to target. We expect him to acknowledge the recent tightening in financial conditions, and suggest policy rates could become lower than previously expected (which moved up following stronger than expected economic data YTD). He’s likely to emphasize the FOMC expects recent policy backstops to be effective, but also suggest the Fed is ready to act if further measures are needed to defend financial stability.

Chair Powell is likely to suggest the underlying bias to monetary policy, absent a credit crunch, remains one of tightening. He will most likely emphasize the significant uncertainty to economic projections and the policy rate path, and downplay the importance of dot plot/SEP. Although the FOMC won’t have the Q1 Senior Loan Officer survey on bank lending conditions with them at the meeting this week, we suspect the Fed has gathered much information from their banking contacts during the intermeeting period. A bias in Powell’s communication one way or another could give a glimpse into their readings on the amount of contraction in bank lending activity so far.

Rate Decision

We expect a 25bps rate hike, and see risks of a pause. Market is priced for ~20bps. Street economists are split between hike (23 dealers)/pause (4)/cut (1). We could see one dissent from a regional bank president in favor of a pause.

Dot Plot

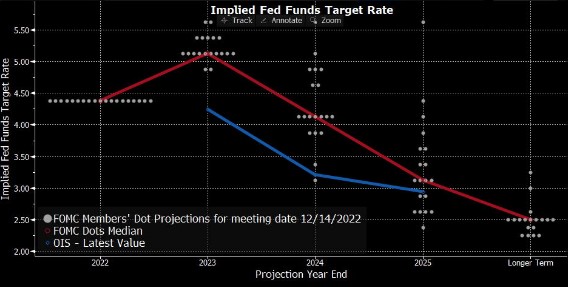

Focus should be squarely on the 2023 median dot and distribution, although Chair Powell will most likely downplay the importance of dots given elevated economic uncertainty. We expect the median dot to remain unchanged at 5-5.25%, which would imply another 25bps rate hike (assuming they hike by 25bps tomorrow). We see risks that some dots will already show cuts or pause this year, but don’t expect that to be the median projection. Most street economists see either unchanged or another 25bps upward adjustment in the median 2023 dot, while the market is priced for more than 60bps of cuts starting from June (bottom chart).

There’s an outside chance the Fed skips the dot plot, but that could be taken as significantly dovish, and not our base case. For reference, the FOMC skipped publishing the dot plot in March 2020 due to extreme COVID-related uncertainty. The dot plot and economic projections were first submitted last Friday (Mar 17th), but officials could revise their forecasts up until tonight (Tuesday).

QT

We expect no change to the Fed’s existing plan of balance sheet runoff on Treasuries and agency MBS. QT remains a tool to remove monetary accommodation. However, we see non-zero risk of a stop in QT at this meeting, or of Powell signaling a willingness to adjust QT going forward based on financial market developments.

Policy Statement

Forward guidance that “ongoing increases in rates will be appropriate” will likely be removed. We expect the statement to add the Committee is closely monitoring the global economic and financial developments and is assessing their implications for the labor market and inflation. Risk is the statement could point to a bias toward further tightening, suggesting that further increases could be appropriate if baseline economic projections hold. But we think it’s more likely that Chair Powell conveys the message at the press conference.

Summary of Economic Projections (SEP)

The range of economic forecasts, and the distribution and uncertainty of the forecasts, should be more important to analyze than a single point forecast. We expect largely unchanged median projections, but we could see more negative outlook on growth and the unemployment rate, and a much wider uncertainty band. Inflation expectations could move up marginally. We expect risk assessment to the outlook to mostly shift to the downside.