By Peter Garnry, Head of Equity Strategy at Saxo

With the focus on reducing carbon emissions, economies such as Europe are committed to drastically reduce emissions by 2050. The main engine behind achieving this goal is to electrify heating and transportation which will dramatically expand electricity consumption.

Peter Garnry

According to Bloomberg New Energy Finance, Europe’s path to clean energy (net-zero) in 2050 is a $5.3trn investment opportunity. In the main scenario, fossil fuels need drops by 28% driven by a sharp reduction in coal primary energy source in power generation. Oil demand could fall 30% driven by adoption of electric vehicles. Natural gas demand will only drop 5% as the energy source is still key in base load power generation. In these forecasts, wind is expected to be the main supplier of primary energy, with offshore wind as the main component, driven by developments in battery and hydrogen electrolysis technologies mature. Electricity demand is expected to increase 82% towards 2050 driven by the adoption of electric vehicles, heat pumps, and electrified industrial processes. The residential sector is roughly 30% of total electricity consumption, but this share is expected to increase over time.

In McKinsey’s Transformation of Europe’s power system until 2050 the consulting firm lays out its assumptions which is only 40% power demand increase until 2050 as it assumes an annual 2% energy efficiency improvement. McKinsey sees a slightly bigger role for nuclear but it is still renewables that will drive the transition. Europe’s supply and demand regions will also decouple and McKinsey expect the current power pricing mechanism to be broken as the mix of renewable energy increases. In a Nordic energy report it is expected that electricity demand will rise 60% until 2050, so there is a wide range of forecasts on electricity demand.

All the forecasts above indicate a slow smooth progression to the end point in 2050. However, technology has a tendency to surprise and our view is that electrification will accelerate at a much higher rate than expected above. In this analysis from Denmark in 2020 the expectation is that electricity consumption will double towards 2030. Current Danish electricity consumption is 35 TWh with the following increase by 2030: +10 TWh from power-to-X, +9 TWh from heat pumps, +7 TWH from data centres, +4 TWh from cars, busses, and trucks, +3 TWh from other transportation, +2 TWh from expansion of North Sea oil and gas production (running production platforms) until 2030, and finally +1 TWh from trains.

The forecast above indicating a doubling seems more reasonable given the adoption rates we currently see from EVs and heat pumps. The average household electricity consumption in Europe is around 3.7 MWh. It is estimated that a heat pump use 4 MWh of electricity annually and the US Energy Department estimates that one electric vehicle requires 3.8 MWh per year of energy generation. Excluding any efficiency gains one household in the EU replacing gas heating with heat pump and replace one gasoline car with an EV will increase electricity consumption by almost 200%. Many households have two cars which over time will be EVs, so that is another increase. Electricity power generation will undoubtedly enter its second age of booming.

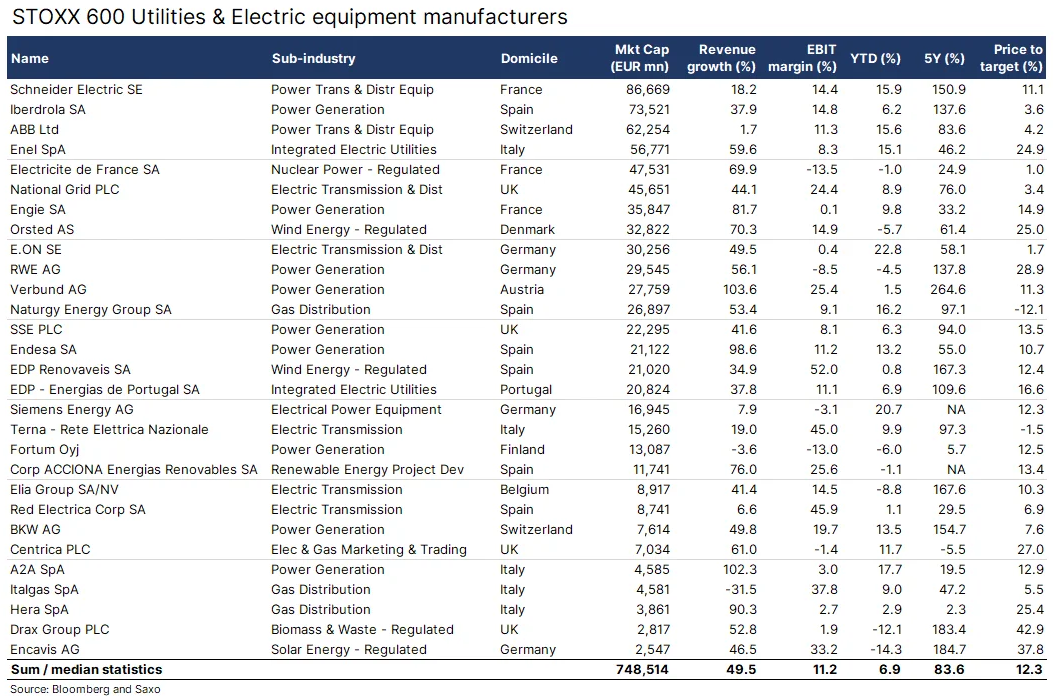

Opportunities in Europe’s utility sector

We are overweight the green transformation because investors should miss out on the biggest transformation of society since the steam engine was invented unleashing the carbon based economy for the next 250 years. The table below shows 29 companies in the European utility sector (excluding water utilities) including three electric equipment manufacturers ( Schneider Electric , ABB , and Siemens Energy). Due to high electricity prices post Russia’s invasion of Ukraine revenue growth has been very high for electric utilities at 49.5% y/y. Investor demand for shares in European utilities has been robust this year with shares up 6.9% this year and over the past five years these stocks have risen on average 84% with the best performing stock being Verbund , one of Europe’s largest hydropower companies which operates at the lowest marginal cost of electricity.

The utility sector can be broken into different parts. Utilities generate the main part of their electricity from an energy source which is either natural gas, hydro, solar, wind, or nuclear. Some companies are big in distribution while others have a lot power generation assets. Other companies are more project oriented such as Orsted which means that they deploy know-how and capital in building out a power generation asset such as an offshore wind power farm and then they sell it to infrastructure investors such as pension firms. Finally there are the electric equipment manufacturers.

One of the main features of the forecasts mentioned in the first section is that they all assume wind power to dominate the transition which might be the case if electrolysis costs come down enabling large scale green hydrogen production. It seems many are still underestimating solar which actually expected to grow in annual capacity from around 200 GW in 2022 to around 500 GW in 2026. Solar in many ways have shown better technology improvements that wind and it is less complicated to build out than wind power with less maintenance. In any case, the future is difficult to predict and an investors should be bet on many different energy sources.

As we have highlighted in other previous equity notes the electrification will create opportunities in other areas such as copper mining, lithium mining, electrolysis equipment, electric vehicle makers, wind, solar, fuel cells, batteries, and charging stations.

The history of electricity started in the years 1831-32. Electrification did once captivate investors. In the coming decades it will for sure come with many opportunities and maybe a new speculative bubble.