By Peter Garnry, Head of Equity Strategy

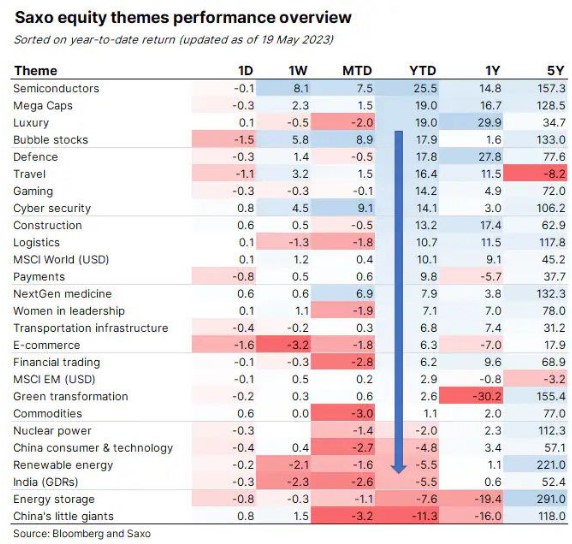

Semiconductors are so far the winning theme this year up 26% as the hype around AI technology related to the generation of chatbots and rising expectations of Fed rate cuts later this year have driven sentiment higher. The demand outlook for semiconductors is strong but it will come with several risks around geopolitics and potential rising production costs from bans related to the use of the chemical PFAS.

Best performing theme basket in 2023 driven by AI hype

Semiconductor stocks were hit hard during the 2022 reset as interest rates galloped higher deflating equity valuations. In addition global supply chain bottlenecks eased reducing some of the pricing power that many semiconductor companies had enjoyed during the early hectic months of the pandemic and especially in 2021 as the world came back online. A combination of AI hype around the new chatbots (ChatGPT and Bard ) and expectations of Fed rate cuts later this year have pushed semiconductors into the top ranking on theme basket performance up 25.5% this year outpacing other themes such as mega caps, luxury, bubble stocks, and defence.

The semiconductor industry will likely continue to deliver high long-term growth as semiconductors are essential for our modern economy ranging from cars, smartphones, datacenters, AI and machine learnings systems, and defence systems. The ongoing AI race between Alphabet and Microsoft is an additional growth driver on top of what is taking place already. The industry has grown revenue by 13% the past year and the industry enjoys a high barrier to entry through being capital intensive and intellectual property rights heavy providing the industry with high profit margins.

China’s ban on some Micron Technology chips highlights geopolitical risks

While the demand outlook for semiconductors remains attractive it will not come without risks to shareholders. Micron Technology shareholders experienced that over the weekend when China banned some of its memory chips in China over cyber security risks. For Micron Technology the ban meant a 2.9% decline in its share price as investors realized that the ban was very narrow and that Micron Technology is only getting 16% of its revenue from mainland China and Hong Kong. For China these memory chips can easily be replaced from domestic production or South Korean manufacturers, but it has raised the stakes that China might go after Qualcomm and Intel as well, but the risk for China is that it will wreck its own supply chains in such a move.

The geopolitical confrontation between the US and China started during the Trump administration years when the former US President basically said that globalisation for not a one-way street of wealth creation. It had real consequences for a larger part of the population in the US and Europe. With Russia’s invasion of Ukraine the geopolitical risks increased further and the US has taken steps to re-write industries with national security interests. One of these industries is the semiconductor industry which consists of a highly fragile global supply chain that creates vulnerabilities for the US and Europe.

The US CHIPS Act announced back in August 2022 has a clear intent of subsidizing and setting up an attractive investment framework for US-based semiconductor manufacturing. The US has also introduced several restrictions on semiconductor exports to China and the pressure has been increased on the Dutch government to make restrictions on exports of ASML ’s extreme ultraviolet lithography machines to China. Making things even more tense, Japan has announced a set of chipmaking curbs related to China which according to China’s semiconductor industry are potentially even worse than the curbs set by the US. In April this year the EU Commission released its European Chips Act in a step to offset its weaker competitiveness against the US post the US CHIPS Act and decrease supply chain risks related to semiconductors. Around 10% of the global semiconductor production is located in the EU.

Are semiconductor driving full speed towards the PFAS roadblock?

Another risk to the semiconductor industry is class of chemicals known as PFAS which are critical for production of microchips. However, recent research has shown that PFAS is dangerous for human health and can even by carcinogenic. This led 3M to announce in December 2022 that it is exiting PFAS production by the end of 2025 as the profits are no longer enough to justify the potential costs from litigation in the future. This decision has set the chipmaking industry on edge because a lack of PFAS supply or other type of restrictions, the EU announced in March that it is planning a ban with a 13,5 years of transition period, would severely constrain the semiconductor industry going forward. To make things worse that are no ready available options to replace PFAS and thus this issue might to a severe roadblock for computer chips and thus overall technology. In the best case scenario a substitute for PFAS is found at equal costs, but a more likely scenario is a replacement but at additional costs. Again another component pointing towards more inflation in the future.