Frederik Ducrozet, Head of Macroeconomic Research, chez Pictet Wealth Management.

After raising rates by 500bps at each of the past ten FOMC meetings, we expect the Fed to “skip” and keep rates unchanged this week, while retaining a hawkish bias. The risk is for a 25bps rate hike, of which the markets are currently pricing a 27% chance. We expect the median dot to shift up by 25bps to 5.25-5.50%, implying one more 25bps increase this year. The economic projections are likely to see upgrades to higher growth, lower unemployment, and slightly higher core inflation. We don’t expect much change in the policy statement as it will continue to note “the extent to which additional policy firming may be appropriate” and we don’t expect any changes to QT. One or two hawkish dissents from the regional Fed presidents in favor of a hike would not be surprising to us, although a dissent from a Fed Governor has not occurred this cycle.

Barring a significant upside surprise in CPI (reported on the first day of the FOMC meeting) or media reports of a change in policy stance (given the Fed is in blackout), the most likely outcome remains a hawkish skip.

Powell Press Conference

Since the last FOMC meeting, the debt ceiling crisis has been resolved and the banking sector stresses stabilized. Overall unemployment remains low and inflation stays way above target. However, labor market data have shown tentative signs of cooling and inflation pressures are easing somewhat. Importantly, Chair Powell and some Fed governors, the core of the committee, have recently signaled a willingness to skip a rate hike in June to better assess lags of monetary policy tightening and any impact from banking sector stress. Chair Powell is likely to signal a pause in hiking at this week’s meeting does not mean the Fed is done fighting its inflation battle. He will likely continue to push back against rate cuts pricing, noting that although rates are near or possibly at sufficiently restrictive levels, the next move is more likely to be a hike than a cut and rates are likely to stay restrictive for some time.

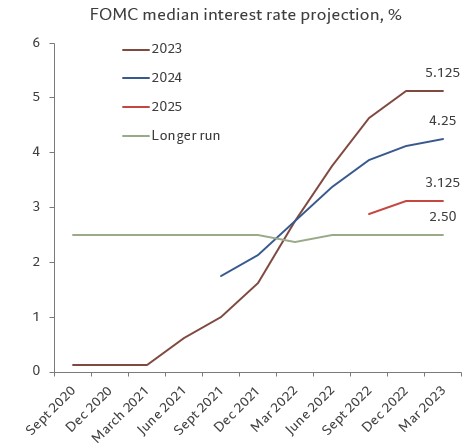

Dot Plot and Summary of Economic Projections

We expect the median 2023 dot to shift up by 25bps to 5.25-5.50%, which would imply another 25bps rate hike (assuming they hold in June, chart 1). We expect the dots to show split opinions on the committee, with some dots showing no change, and some showing more than one more rate hike this year. There has been increasing focus on the Fed’s longer run interest rate estimate in light of the relaunch of estimates of the real neutral rate r*, which argues for a continuation of a low rate environment that existed pre-pandemic. The Fed’s longer run estimate has been remarkably stable throughout the pandemic and we expect it to remain unchanged at 2.5%.

The economic projections are likely to see small upgrades to higher growth, lower unemployment, and slightly higher core inflation, given data surprises between the March and June meetings. The dot plot and economic projections were first submitted last Friday (June 9th), but officials could revise their forecasts up until Tuesday night (after Tuesday’s CPI report).

QT

We expect no change to the Fed’s existing plan of balance sheet runoff on Treasuries and agency MBS. The ongoing surge in T-bill issuance is likely to drain both bank reserves and the ON RRP facility at the Fed. The risk is if the majority of the issuance was absorbed by falling bank reserves (instead of a decline in RRP), reserves could approach the minimum comfortable level sooner than expected, leading to an earlier end to QT. (Rough estimate for the minimum level is around 8% of GDP or around $2.4-2.8trn, although big error bands). Our base case remains that QT will continue until at least the end of this year.

Policy Statement

We don’t expect much change in the policy statement as it will continue to note “the extent to which additional policy firming may be appropriate”. A hawkish risk is if the statement added that further policy tightening could be appropriate at an upcoming meeting, which would hint strongly at a hike in July.