By Peter Garnry, Head of Equity Strategy at Saxo

Japanese equities are on the radar of global investors in a way we have not seen in decades. The equity market in Japan was historically a hunting ground for deep value stocks, but the Japanese corporate sector has changed a lot since Abenomics was introduced in 2012 and today it is more interesting to find the country's high quality companies. Among these high quality companies is Advantest, a leading semiconductor test equipment maker, which has delivered almost 30% annualised returns over the past decade.

The Japanese equity market has been one of the bright stories this year outside the crazy AI hype driven US technology segment. The TOPIX 500 Index is up 22% in local currency this year reaching a new high in today’s trading session. We wrote earlier this year two equity notes called Will the sun rise over Japanese equities? and Japan and Greece: the two comeback countries highlighting the attractiveness of Japanese equities. Since those two notes the Japanese equity market has not disappointed and when we look at equity valuations they are still more attractive than US equities.

One important thing to note is that the rally this year has not been led by either growth or value stocks using MSCI methodology suggesting that there are no clear quant factors driving the rally, but rather a broad-based rally. Japan has been put on the map on the map by global investors since Warren Buffett’s Berkshire Hathaway made their investments in Japanese commodity trading firms. The rising tensions between the US and China have also put Japan on a path to become a more important manufacturer of physical goods for Western companies to reduce their supply chain risks.

Finding the rare gems of Japan’s corporate sector

Japan was known for decades to be a hunting ground for deep value stocks, meaning the companies were valued below their net liquidation value and here we are not talking about book value, but below the net-working capital position. This was the old classic Benjamin Graham, the mentor of a young Warren Buffett, yardstick for value, but has since disappeared because understanding of equity valuation has removed such rare deep value stocks. These opportunities only existed in the post 1929 crash market because investors were simply scared of stocks.

Fast forward to Japan in 2023 and investors can still go on deep value hunting, but this segment is what Warren Buffett would call looking for cigar boxes with maybe one last cigar puff. In general we would argue that it is more interesting to hunt for high quality companies and a good way to start is to isolate companies with a high return on invested capital as that is typically a signal of a strong business model and product.

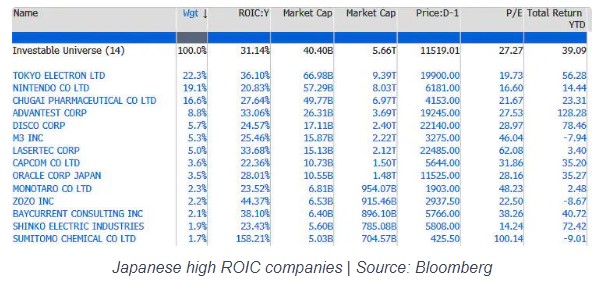

The list below shows 14 Japanese companies with a ROIC above 20% and a market value above $5bn. One observation is that this group of companies is quite small given the size of Japan’s equity market but it underscores Japan’s long tradition for maintaining corporate intra-holding relationships and employment more than effectively using capital. However, as we highlighted in our recent notes the Japanese corporate sector is changing and has become much more efficient in its use of capital. For many foreign investors there will not be many recognizable names except maybe for Nintendo which is a household name in many countries due to its iconic gaming consoles.

Advantest advances on AI rally

One of the companies on our list of high quality stocks in Japan is Advantest. The company is Japan’s leading manufacturer of automatic test equipment for the semiconductor industry, and manufacturer of measuring instruments used in designing, production, and maintenance of electronic systems such as fiber optics and wireless communications equipment.

In a country known for low growth and inflation since the late 1980s, Advantest is a rare growth story that has grown revenue from $1.61bn in FY13 (ending 31 March 2013) to $4.14bn in FY23 while expanding the EBITDA margin from 6% to 34%. The combination of 10% annualised revenue growth and rapidly expanding margins are the two key factors behind the impressive 27.3% annualised returns over the past 10 years and 29.5% annualised returns if dividends had been reinvested in the stock. The AI-hyped rally in US technology stocks has spread like ripples across the global semiconductor industry and Advantest shares are up 128% this year.

Explosive stock returns like this is not normal in the Japanese equity market and sell-side analysts have not been able to keep up with the 12-month price target sitting at only JPY 16,000 compared to the closing price to day at JPY 19,190. With an EV/EBITDA multiple of 19x Advantest is as expensive as it has ever been but still just in line with the global semiconductor industry.