By Peter Garnry, Head of Equity Strategy at Saxo

Equities were wobbling in August with all our theme baskets down except for the nuclear power theme basket highlighting the higher for longer narrative. However, recent economic data have been weaker than estimated. The US fiscal impulse could soon turnaround from being positive to negative lowering economic growth and forcing the Fed to cut the policy rate in early 2024. This would obviously be a negative environment for equities. Adding to our worries on equities are the elevated equity valuations on global equities reaching levels consistent with a negative outlook.

Will the economic cycle turn as US fiscal impulse goes negative?

Last year in July, the US fiscal deficit in percentage of nominal GDP stood at 3.7%, but as the Biden Administration launched a series of fiscal spending bills, including the groundbreaking US CHIPS Act, the fiscal deficit expanded to 8.4% of GDP. This constitutes an almost 5%-points increase in the fiscal deficit which create a significant fiscal impulse dynamic into the US economy. This impulse helped the US economy avoiding a recession this year as the fiscal impulse more than offset the historic rise in the Fed’s policy rate.

In July of this year, after a year of positive fiscal impulse, the fiscal deficit contracted a bit suggesting that maybe the fiscal cycle is turning. If this is the case, then over the coming year the economy will likely begin to slow down in a pace that will warrant the Fed to cut its policy rate to balance the economy. Depending on inflation dynamics and the Fed’s reaction time, the economy could slip into a recession in 2024 or at best find itself in a stagflation environment.

Equity valuations reflect “as good as it gets”

Given the likely turn in the US fiscal impulse the macro investor might favour defensive equities over cyclical equities and bonds over equities. The investor might be further confirmed in this opinion by the fact that global equities have seen their equity valuations bounce back to being almost one standard deviation expensive relative to the long-term historical average. The current equity valuation level on the MSCI World is consistent with higher probability of negative real rate returns over a 10-year period than positive real rate returns.

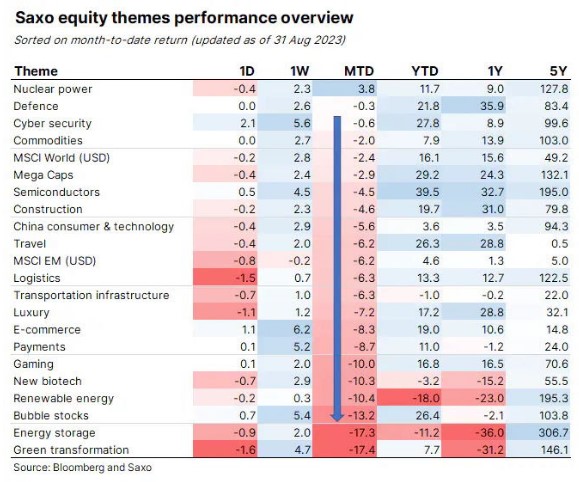

Nuclear power was best performing theme in August

Despite a good week in global equities August was a bad month for our equity theme baskets with especially a lot pain in our energy storage, renewable energy, and green transformation baskets. The big story in the green transformation trade was the DKK 16bn impairment announced by Orsted due to supply chain costs, higher interest rates, and lack of progress in additional US tax credits all related to its US offshore wind projects.

Not all theme baskets related to energy have done bad in August. Our commodities theme basket was only down 2% in August outperforming the MSCI World Index driven by gains across many commodities including strong gains in crude oil.

The best theme basket in August, and the only one gaining, was our nuclear power basket which increased 3.8% as prices on uranium continues to go higher with worries over the coup in Niger, home the seventh largest uranium mine in the world, adding to the pressure. Cameco, one of the largest global providers of uranium fuel, lifted their outlook in their FY23 Q2 results highlighting improving market fundamentals and increasing excitement from governments as nuclear power is increasingly seen a solution to decarbonize the global economy.

Adding to the nuclear power narrative, Sam Altman, co-founder of OpenAI, recently announced the intention to merge his small modular nuclear reactor company Oklo with a SPAC to go public under the ticker code ALCC. The fact that there is enough public investor interest in emerging nuclear power designs and technologies says a lot about how much the narrative around nuclear power has changed. We remain long-term positive on nuclear power.