By Armand SATCHIAN, Sustainable Investment Research Analyst, Crédit Mutuel Asset Management

Crédit Mutuel Asset Management is an asset management company of Groupe La Française, the holding company of the asset management branch of Crédit Mutuel Alliance Fédérale.

An optional « GAR », updated in 2026?

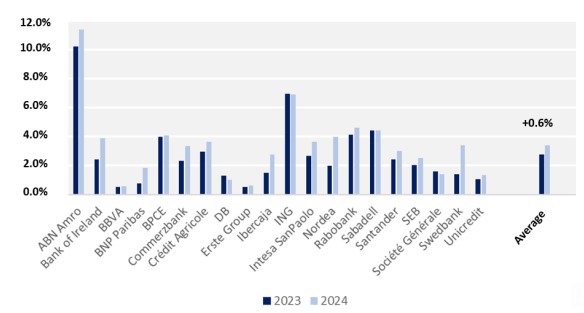

The Green Asset Ratio (GAR), which measures the proportion of a bank’s assets aligned with the European taxonomy, is a key indicator for assessing financial institutions’ involvement in the transition to a low-carbon economy (see Green Asset Ratio – Is the crash test really a complete failure? ). However, since the GAR’s introduction, several limitations have been pointed out such as, differing scopes between the numerator and the denominator, as well as major challenges in ensuring compliance with DNSH (Do No Significant Harm)[1] and MS (Minimum Safeguards)[2]. These shortcomings help explain the relatively low GAR levels reported in 2024 (average of 2.8 % across a sample of 20 banks). This trend has continued in 2025, with the average GAR still low (3.4 % for the same sample) highlighting the ongoing challenges raised by banks.

GAR evolution for a sample of 20 banks (2023 – 2024)

Source : Crédit Mutuel AM, 2023 and 2024 Publications (Annual & Pillar III reports) of mentionned banks Since the beginning of 2025, European institutions have responded to the concerns raised by banks, and these answers should be reflected in 2026 disclosures (for the 2025 financial year). In July 2025, the European Commission published a draft Delegated Act[3] as part of the simplification effort led by the Omnibus Package[4]. It includes major proposed changes to the GAR, such as:

Excluding from its denominator companies not covered by the Corporate Sustainability Reporting Directive (CSRD) Introducing a materiality criteria allowing financial institutions to exclude financial assets that represent less than 10% of loans or investments dedicated to specific activities[5] Simplifying reporting templates, resulting in an 89% reduction in required data points While some of these measures directly address banks’ concerns, others may, at least temporarily, reduce transparency in disclosures. For example, the European Commission announced that the publication of the detailed GAR templates would be optional until the end of 2027, provided that the institution declares that « no activity is claimed to be associated with economic activities that qualify as environmentally sustainable under articles 3 and 9 of Regulation (EU) 2020/852 »[6]. Similarly, a few weeks earlier, the European Banking Authority (EBA) announced in a consultation paper the suspension of disclosure obligations for templates 6 to 10 related to the GAR and of the Taxonomy Regulation in Pillar III reports (these ESG disclosures being published semi- annually).[7]

It is essential to stress that, given the Taxonomy’s pivotal role in the current legislative framework and the various requirements set by European supervisory and regulatory authorities (such as ESMA, the ECB, etc.), updates to Taxonomy regulations could have ripple effects.

Other « non taxonomic » indicators

While addressing some concerns, the GAR update will also narrow the indicator’s scope, due to the reduced coverage of the CSRD. Moreover, it opens the door to a temporary suspension of disclosure requirements, and will not immediately resolve other existing limitations of the European taxonomy such as the exclusion of certain activities (eg. agriculture) and the non-integration of social objectives. Therefore, the GAR remains, at best, a partial illustration of sustainable financing mobilized by banking institutions.

However, other disclosures from these institutions can add context – without guaranteeing exhaustiveness. For example, Template 2 of the Pillar III report[8] details exposure to the residential and commercial real estate sectors with a breakdown based on energy consumption and EPC labels (noting that many properties are still not covered by these labels). The Energy Financing Ratio also offers valuable insights into a bank's ability to support the transition by capturing both green and brown flows. While this indicator is not mandatory, it is gaining traction amongst banks, especially in the United States, where many institutions have submitted it for shareholder votes during their 2025 Annual General Meetings[9]. That said, caution is necessary due to the lack of standardization, which often leads to the use of varying methodologies[10].

On the social dimension, indicators are less prevalent. However, Template CR1 in the Pillar III reports of European banks highlights the proportion of SMEs in their portfolios. This data offers relevant insight into the role played by banks in promoting financial inclusion and supporting the local economy.

Finally, allocation reports on capital raised through labeled issuances, along with progress reports toward sustainable finance targets, can further enhance this picture. However, readers should be mindful of the lack of standardization in the definition of “sustainable finance” used in these initiatives and the possible inclusion of financial flows not reflected on the balance sheet (structuring of bonds, assets under management).

While the Green Asset Ratio is a useful indicator, it remains limited by its methodology and regulatory scope, which the upcoming 2026 update is unlikely to resolve. Understanding the full scope of banks’ sustainable activities requires more than just the GAR.