Tim Edwards, Managing Director, Index Investment Strategy at S&P Dow Jones Indices comments that January began brightly for the S&P 500 and its factor family, as the steadily increasing number of administered COVID vaccines provided an unambiguously positive statistic. However, VIX® began to sound the alarm as the month entered its final week, and a sharp sell-off in the final trading sessions sent the benchmark to a monthly loss. Most the S&P 500’s factor indices declined with it, but dividend-based strategies, and noncap-weighted value, were among the winners. More broadly, the top-level trend reversal in S&P 500 factor trends that began in the second half of 2020 continued in January: smaller stocks outperformed larger, value outperformed growth, and riskier stocks outperformed less-volatile names.”

Highlights

According to our January S&P 500 Factor Dashboard (attached), risk was also the story within US factor performances. Over the last three months, factor indices with a higher beta to the market have had much higher returns than would be supposed from their betas alone, while factors with a lower beta more than underperformed.

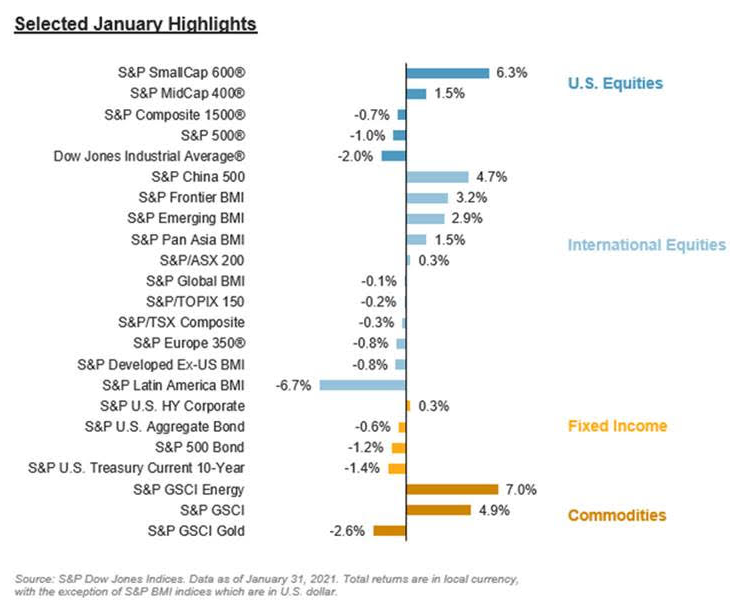

It wasn’t a bad month for everyone: American small caps skyrocketed, gaining 6%, and Chinese stocks lifted the S&P Pan Asia BMI to a gain on the month, helping the S&P Emerging BMI to finish with 3%.

The price of oil continued to rise, lifting the S&P GSCI and Energy equities with it. And although riskier segments generally outperformed, Latin American stocks failed to notice; the S&P Latin America 40 declined 7.6%.

US

A steep sell-off in the last week of January led to a mixed month of performance for U.S. equities, with the S&P 500® posting a loss of 1%.

The reversal that began in Q4 of 2020 continued, as smaller caps outperformed in January, with the S&P MidCap 400® and the S&P SmallCap 600® up 2% and 6%, respectively.

Volatility spiked, as the short squeeze frenzy mounted among retail investors, with the VIX® closing the month at 33.09.

Performance in international markets was also mixed, with the S&P Developed Ex-U.S. BMI down 1% and the S&P Emerging BMI up 3%.

Low Volatility High Dividend and Enhanced Value were the top performing factors.

Europe

The S&P Europe 350® erased its gains in the final trading session, leaving the continent’s benchmark with a small loss for January.

Energy led among sectors of the S&P Europe 350, while Momentum led among factors. Value and Financials were among this month’s underperformers.

After calmer waters for the majority of January, equity volatility raised its head on both sides of the Atlantic as implied volatility measures rose to their highest since November.