By Peter Garnry, Head of Equity Strategy, Saxo Bank

Equities have had a fantastic year delivering 21% return following already extraordinary gains in 2020. It seems almost impossible given the galloping inflation not seen since the early 1980s, but low nominal yields have created an environment of equities being the only game in town. The gains in equities have completely been due to technicalities such as low nominal yields, but have also been driven by a bonanza in earnings with earnings up 28% compared to 2019 showing the massive impact from public stimulus into the private sector. While looking back we are also looking ahead at what to expect in 2022 and how investors should tilt their equity portfolios towards themes that can thrive during inflation.

Negative real rates creates TINA

As investors are getting ready to close their books for the year it is always worthwhile reflecting on the year that has just passed. If we told you that S&P 500 would be up 28% and MSCI World up 21% for the year as the US core inflation hit almost 5%, the highest since the early 1980s, then you would not have believed it. The key to understand why equities are higher despite inflationary pressures are rooted in the bond market’s reaction to rising inflation.

The bond market sided with the Fed perceiving inflation to be transitory, but even as the Fed has terminated this language and said inflation is more deep rooted and persistent than initially thought, the bond market keep predicting inflation to remain low. This is based on the high debt-to-income levels in many parts of the world, ageing populations, and technology advancements all suppressing inflationary forces longer term. The stubbornly low nominal yields while realized and expected inflation are rising have caused a massive downward pressure on real yields, which sets in motion a sizeable reallocation into equities.

Why would you invest in bonds when your capital is being destroyed in real terms? You might as well swing for equities despite historically high prices and valuation because maybe you can at least defend capital against the corrosive inflation. In other words, TINA (there is no alternative) is still very much alive in financial markets as 2022 approaches, because as John Maynard Keynes and Warren Buffett both have observed but in different context, inflation is the enemy of the capitalistic economy and investors.

Profit bonanza driven by record stimulus

While low nominal yields have played their part in the equity rally this year through their impact on the cost of capital which is used for discounting future free cash flows, investors should not ignore the fact that earnings in the MSCI World Index are up 104% for the first three quarters of 2021 compared to the same period of 2020. For those who think that this is just the rebound effect should note that earnings in the first three quarters of 2021 are up 28% compared to the same period of 2019. In other words, the earnings power of companies coming out of the pandemic has been extraordinary and driven by the enormous loose monetary and fiscal stimulus operating on a combined level not seen since the post WWII years. The deficits across many of the world’s largest economies have created a corresponding surge in private sector surplus.

Interest rate sensitivity

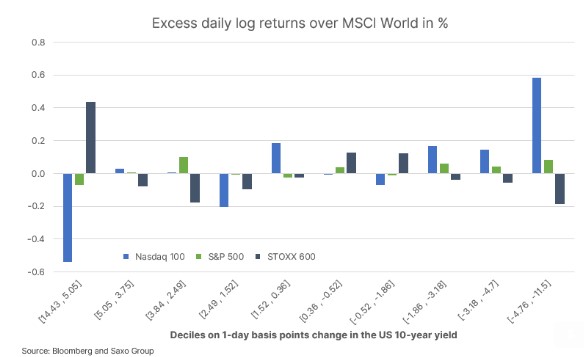

The irony of high profits and stellar equity returns in 2021, is that 2022 might go “wrong” for equities due to inflation outlook as a reaction in the bond market of 100 basis point in the long end of the US yield curve (10-year Treasuries) could push down equities regardless of earnings growth. We have recent estimated growth stocks such as Pinterest and Adobe to have interest rate sensitivity of 18% and 26% which means that is negative impact on their equity valuation from a 100 basis point move in the US 10-year yield holding all other things constant.

The overall US equity market probably has an equity duration around 15-18% which means that simply higher nominal yields could offset earnings growth next year. The chart below is from our recent equity research note Interest rate sensitivity is back in town haunting technology stocks showing how NASDAQ 100 and STOXX 600 are moving in opposite directions to large changes in the US 10-year yield. US technology stocks have a negative excess return compared global equities on days when long-term yields are increasing while European equities exhibit positive excess returns as they have a larger weight on financials, energy and mining.

We still think investors should continue to rebalance their equity portfolios towards being better at absorbing higher interest rates and inflation in 2022. This includes adding exposure to the commodity sector, financials, semiconductors, logistics, and financial trading firms which benefit from higher volatility and can also work as a hedge against tail losses in equity portfolios.

Green transformation, India, China, and urbanisation

Our green transformation basket is down 6% this year giving up some of its massive gains from 2020 when investors poured capital into this theme. Driven by a major breakthrough year for electric vehicles production next year the green transformation trade will come back with a vengeance. Vale is explicitly saying that it wants to become North America’s preferred supplier of the metals needed for the electric vehicle industry and Rio Tinto is also heavily investing in lithium carbonate projects including a big project in Serbia, which has the potential supply almost 10% of Europe’s annual need for its electric vehicle production in the future. The green transformation in terms of electric vehicles, solar, wind, energy storage, hydrogen production will continue due to put upward pressure on many key metals and long-term we believe the green transformation will add significantly to the long-term inflation rate.

India looks like the next China in terms of growth, infrastructure investments, market reforms, technology IPOs and subsequent returns for shareholders, and urbanisation. Indian equities have been one of the best equity markets over the past 20 years growing earnings 10% annualised and we believe this trend will continue over the next 10 years with extraordinary returns for investors. But India’s huge growth and urbanisation will happen simultaneously with the green transformation and also add to global inflation through commodity inflation.

China was on the defensive this year being oddly out of sync with the rest of the world. The housing crisis is causing a negative impact on the economy, credit markets, and consumer confidence. While the industry needs a solution it has to be balanced against the “common prosperity” narrative and we are already seeing signs that the government and central bank are beginning to mitigate the impact on the economy. Public stimulus will come back in 2022, but the looming question is where profitability goes from here as the technology crackdown and other reforms such as the new data privacy law are having an impact with analysts constantly lowering their estimates for growth. We do not have a firm view on where Chinese equities go next, except for our bullish view on consumer goods businesses as they are not intrinsically data-driven.