Food and energy will be at the center of our crisis years

By Peter Garnry, Head of Equity Strategy at Saxo Bank If central banks focus too much on core inflation a big mistake might be the outcome. Food and energy will be at the center of our crisis years with climate change and the green transformation being inflationary in the years to come. Investors should increasingly invest in the tangible world to offset these inflationary risks.

The energy crisis will drive everything

Around 30 central banks around the world have adopted inflation targeting using the headline inflation indices which in the US is the US Personal Consumption Expenditures Index (officially announced in January 2012). The official targeting is the headline inflation indices, but many central banks and economist are often putting more weight on the core inflation indices. These indices remove energy and food from the price index. This practice is likely what made central banks react to slowly to current inflation impulse; remember, at Jackson Hole one year ago Jerome Powell said: “We have much ground to cover to reach maximum employment, and time will tell whether we have reached 2% inflation on a sustainable basis”. At that point US CPI and core CPI stood at 5.4% y/y and 4.3% y/y respectively.

Core inflation indices remove the energy and food items because they are seen as volatile and mainly not driven by the trend change in overall prices, and the key assumption is also that they have temporary factors behind that will reverse later on. This argument was the same for our disrupted supply chains although in reality it has taken much longer than expected.

Food and energy will add to inflation going forward

Our team has written a lot about the physical world and lately we introduced indices of tangibles- vs intangibles-driven industry groups. We have shown many times how the world underinvested in the global energy and mining industry, and why this will haunt the world for years. Food and energy are also intertwined and connected which we have seen today with Yara reducing its ammonia production in Europe to just 35% of potential production due to elevated natural gas prices. Lower ammonia production will lead to less fertilizer for farmers and thus lower food production, which again can lead to higher food prices.

It should be clear by now, that ignoring food and energy could be a grave mistake by central banks. Climate change will make global food production more volatile and push up prices, and the green transformation will for years keep energy prices elevated. Our main thesis is that the coming decade will in many ways be a replay of the 1970s as politicians will intervene in the economy to mitigate the pain from higher prices, but these decisions will only keep the nominal economy growing fast and thus keeping inflation and the readjustments going for longer. The Fed’s core inflation measure is currently at 0.4% m/m measured over six months suggesting a core inflation rate annualized at around 5% which means that short-term interest rates must be set much higher to tame inflation. The headline inflation is currently twice as high as the core inflation.

Nominal wages will underpin inflation for a lot longer

Central banks should give substantial weight to the growth in nominal wages when monitoring inflation. If we look at nominal wage growth in the US we observe a three-staged acceleration in the US economy since 2009.

From 2009-2015 there was only 2% annualized wage growth as the economy was suffering from low demand in the subsequent years after the Great Financial Crisis. During the period 2015 to early 2020 we sax years of loose monetary policy and slowly healing economies which lifted US nominal wage growth to 2.9% annualized. The period from early 2020 until today is driven by the extraordinary monetary and fiscal stimulus that were put in place after the global Covid pandemic broke out. The combined stimulus was on par with the post-WWII years and were unleashed into a global economy that in hindsight was much closer to a hard physical supply limit than understood at the time. Subsequently demand has been running much stronger than trend growth and as a result nominal wages have accelerated to 5.2% annualized growth rate. Indeed, it seems we have a serious problem on our hands where inflation become unanchored from 2%.

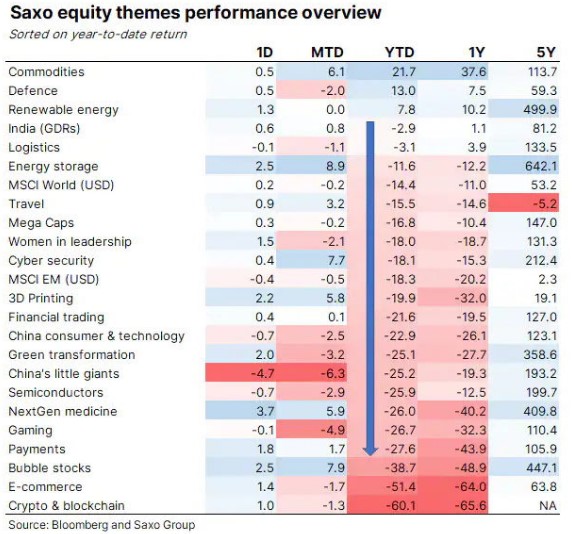

Invest in the tangible world

In an inflationary environment the tangible world must increase dramatically, so investors should invest in the tangible world to offset the inflation risk in order to preserve wealth in real terms. Our theme basket performance overview shows which tangible parts are doing well this year : commodities, defence, renewable energy, logistics, and energy storage.