By Ole S. Hansen,Head of Commodity Strategy at Saxo Bank

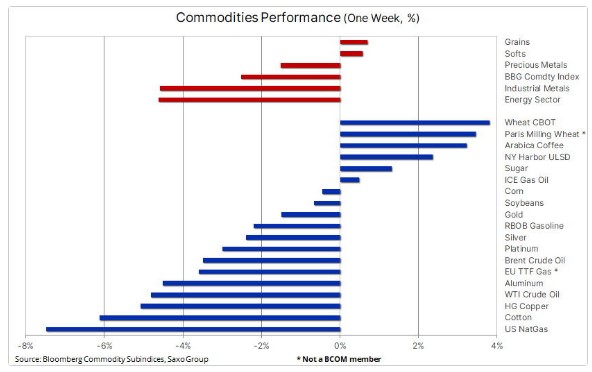

Commodities traded generally lower in a week where the big lines were drawn by developments in Washington and Moscow. At their latest FOMC meeting, the US Federal Reserve managed to surprise on the hawkish side of expectations after an expected 75-basis point rate hike was followed up the removal of expectations for a cut in 2023. Changes that were made despite a significant lowering of the GDP forecast for this year and next as well as a sharp rise in the unemployment rate forecast, a signal the Fed is willing to continue hiking rates even if the economy deteriorates in order to get ahead of inflation.

These developments helped send the dollar and US Treasury yields sharply higher and with other major central banks also hiking, the recession fear took hold and helped send growth-sensitive commodities like cotton and copper sharply lower. However, at the same time, other commodities like gold, wheat and diesel managed to find some support after President Putin escalated his flagging invasion of Ukraine, thereby adding a safe-haven bid to gold while increasing supply risks of key commodities such as wheat, crude oil and fuel products.

The Bloomberg Commodity Index traded lower by 2.5% on the week troubled by tighter monetary policy hurting the growth outlook, weakness in China’s economy and Europe’s energy crisis which has driven the region’s purchasing managers index to its lowest level since 2013. Losses being led by natural gas, cotton, crude oil and industrial metals.

Multiple uncertainties will continue to create a volatile environment for most commodities ahead of the year end. While the recession drums will continue to bang ever louder, the sector is unlikely to suffer a major setback before picking up speed again during 2023. The latest FOMC action has brought the market one step closer to peak hawkishness, potentially sometime during the final quarter of 2022, and once that happens, a subsequent peak in the dollar and Treasury yields may reduce some of the recent headwinds.

Our forecast for stable to potentially even higher prices led by pockets of strength in key commodities across all three sectors of energy, metals and agriculture is driven by sanctions, upstream cost inflation, adverse weather and low investment appetite, and with that in mind, we see the Bloomberg Commodity Index, which tracks a basket of 24 major commodities, holding onto most of its year-to-date gains around 15% for the remainder of the year.

Global container shipping rates in free fall

The deteriorating global economic outlook can be seen through the continued collapse in the cost of shipping 40-foot containers around the world, especially on the major routes from China to Europe as well as the US East and West Coasts. The Drewry Composite Container Freight Global Benchmark rate slumped 10% this past week to $4,472 per 40 feet box, and lowest since Dec 2020. Down 57% from the September 21 peak but still three times higher than the pre-pandemic average, suggesting further downside as the global economy continues to lose steam. As mentioned, all the major China to US and EU routes have slumped while the transatlantic route to New York is holding up, potentially due to the euro weakness supporting exports to the US.

Wheat sees largest gain since March on Ukraine and weather concerns

Chicago and Paris wheat futures, two of the best performing commodities markets this past week, reached a two-month high supported by risks of a deepening conflict in Ukraine putting the UN-supported grain export corridor at risk, and dry weather in crop areas of Argentina and the U.S. Plains. This despite an upbeat production update from the International Grains Council in which they lifted global production for the 2022/23 season by 8 million tons, mainly due to upgrades in Russia, Canada and Australia, an upward revision that would leave stocks higher at the end of the period by 10 million tons.

However, a reduction in already-weak exports of high-quality wheat from Ukraine may underpin prices into the winter months, not least considering the risk of triple-dip La Ninã raising concerns about production during the coming Southern Hemisphere growing season. Ukraine’s exports reached 883,000 tons in August, some 2.7 million tons below last year’s pace. That deficit may grow in September, normally the busiest month for Ukraine’s exports which reached 4.6 million tons last year. Keeping the route open, however, would see exports remain supported into what normally is the shoulder season of activity.

Gold succumbs to continued dollar and yield strength

Gold spent most of the week managing to find a geopolitically-related bid to shield it from the negative consequences of sharply higher US Treasury yields and dollar. In the end, however, the market buckled under the weight of deteriorating market sentiment driven by a 32-basis point jump in US ten-year yields to a 12-year high at 3.75% and a 2% rise in the Bloomberg Dollar Index to a record high (since 1997).

Gold and the other semi-investment metals like silver and platinum will likely to continue to remain under pressure until the market reach peak hawkishness, potentially not before 4% is reached in 10-year yields and the dollar squeezes out any remaining short positions. Whether the turning point will be reached before yearend remains to be seen. By continuing to raise interest rates while also raising expectations for lower growth and rising unemployment, the FOMC is signaling a recession is a price worth paying for getting inflation under control. We maintain a long held view the market, just like the FOMC, may end up being too optimistic in their belief inflation will return to the sub 3% level currently being priced in via the swap market.

Resistance has moved to $1690 while the break below $1654 on Friday could see the market target the 50% retracement of the 2018 to 2020 rally at $1618.

Copper and crude oil trade lower responding to growth worries

Growth and demand dependent commodities from copper and aluminum to crude oil all slumped with the focus fixed on the mentioned macro-economic developments with supportive supply issues, especially in crude oil, for now being pushed aside. Some signs of weakness, however, was seen in copper where inventories of copper monitored by the London Metal Exchange rose steeply for five straight days while the recent tightness in spot market showed signs of easing. The High-Grade copper futures traded in New York slumped by 4% on Friday to $3.33 per pound, a break that potentially could see the metal having another go at challenging key support around $3.14 per pound, the July low and 61.8% retracement of the 2020 to 2022 rally.

Crude oil meanwhile headed lower after spending most of the week confined to a relative tight range with the Powell versus Putin battle (demand versus supply) not having a clear winner until Friday when both Brent and WTI dropped as the FOMC driven slump in risk appetite and growth angst was dialed up a notch as the dollar and yields continued to surge higher. A difficult and potentially volatile quarter awaits with multiple and contradictory uncertainties having their say in the direction. While the risk to growth is being priced in, the market has left it to another day to worry about the supply-reducing impact of an EU embargo on Russian oil and fuel as well as a part reversal of the US selling 180 million barrels from its Strategic Reserves.