By Peter Garnry, Head of Equity Strategy at Saxo

Powell was clear yesterday saying that it is premature to even think about pausing rate hikes as inflation goes to surprise to the upside relative to the Fed's model forecasts. Despite much tighter financial conditions, the US economy is still going strong with a labour market that is still significantly more tight than the pre-pandemic level suggesting wage pressures will continue to cause headwinds for companies and keep inflation higher for longer. Equity valuations are around the long-term average since 1995 suggesting more downside risks to equities as interest rates will likely increase, margins will continue to decline, and revenue expectations may cool.

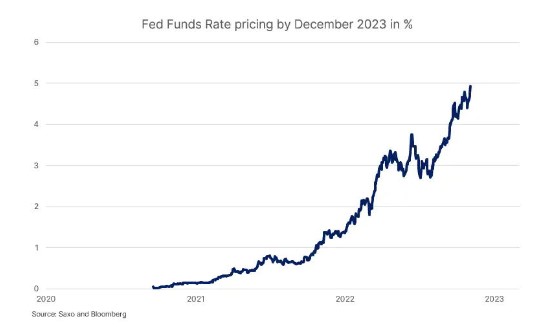

Equities rallied initially on the FOMC press release revealing a 75 basis points hike to 3.75-4% target range and the need for ongoing hikes until rates are sufficiently restrictive, but during the press conference Fed Chair Powell steered the narrative in a completely different direction. Powell said that the Fed still had some ways to go on rates and that the ultimate rate level was going to be higher than previously, expecting touching on a pattern that the Fed’s models have continuously been wrong. Powell basically said that he does not trust the current forecasts and that it is very premature to think about pausing rate hikes. The reaction has been a 25 basis points move higher in the expected Fed Funds Rate in December 2023 (see the chart below), suggesting the market is revising up its terminal rate projection. If the error in inflation forecasts continue with the pattern Powell suggests then this rate will likely continue higher to reflect the ‘higher inflation for longer’ narrative.

In addition to these statements on rates Powell said that the window of ‘soft landing’ in the economy is narrowing, suggesting the Fed sees that it is increasingly getting more difficult to set the economy up for soft landing while taming inflation. ECB President Lagarde is also out saying today that a mild recession is not enough to tame inflation to desired levels, suggesting two natural trajectories in the economy and central bank policies. Either central banks let inflation run higher for longer pausing rates at levels creating a soft landing but anchoring inflation at higher levels for longer, or they keep hiking until the economy goes into a deeper recession. Both trajectories are bad for equities but the latter has more negative dynamics than the first.

What has been remarkable is the extent to which the US economy has been able to absorb tighter financial conditions. Despite a regular interest rate shock, Powell’s preferred measure on the US labour market is still indicating that the labour market is red hot and very tight suggesting wage pressures will continue for a prolonged period keeping inflation higher for longer. The measure Powell has been speaking about is the total job openings in the US economy relative to number of unemployed workers. This measure is still 56% higher than the pre-pandemic level which in itself was indicating the tightest US labour market since at least 2002.

The triangle of discount rate, growth and margins

Equities have three dominant drivers of valuation with the discount rate being the biggest influencer of equity declines over the past year. Margins are clearly rolling over in recent earnings seasons as wage pressures and commodity prices are squeezing companies’ ability to pass on all of the costs. That means that the only opposite force to lift equities has been revenue growth expectations which are directly linked to the probability of a recession. The recent rally in equities has been linked to the ‘soft landing’ narrative as economic data are suggesting the economy is growing at trend growth despite tighter financial conditions.

But with Powell’s statement about the window is narrowing for a soft landing and higher terminal rate the equity market will soon be under pressure from both higher discount rate, lower revenue expectations, and margins rolling over. Our medium term outlook of the S&P 500 hitting the drawdown cycle low at the 3,200 level is still our base case scenario.

Equity valuations sit on the average since 1996

On a monthly basis we update our valuation model on global equities consisting of seven different valuation metrics in order to gauge the overall valuation level and what it potentially means for future returns. As of October, the MSCI World was valued just around the average since 1995 after peaking out in February 2021 at 1.67 standard deviations above the average. The current equity valuation level adds to downside risks in equities as the current level in the US 10-year yield is now above the long-term average since 1995 and will likely continue higher given Powell’s statements yesterday. With an above average interest rates and inflation environment coupled with increasing risks of lower economic growth we expect equity valuations to compress even further.